From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineDeclining Activity Levels and Regulatory Pressures: The Current Steel Market Dynamics in Asia

Recent insights into the Asian steel market reveal a concerning decline in activity levels across several key steel plants, driven partly by the looming impacts of the EU’s Carbon Border Adjustment Mechanism (CBAM). As highlighted in “Irepas: CBAM to favour verified mills by 2027,”, mills with verified emissions data may secure a competitive edge. However, instability from excessive cost pressures and weakened demand, as noted in “Irepas: CBAM will give preference to proven plants by 2027,”, is amplifying market fears.

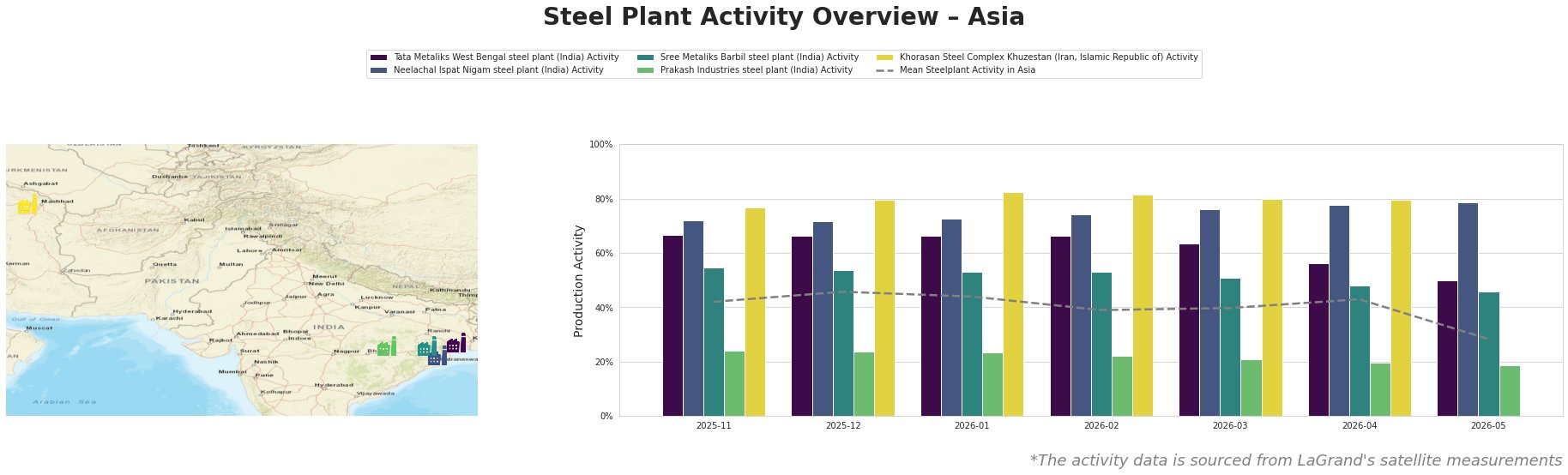

Measured Activity Overview

Activity at the Tata Metaliks plant decreased from 67% in late November 2025 to 50% by May 2026, indicating a decline that closely aligns with overall market trends and regulatory pressures referenced in “Carbon Chain: Default emission values can double or triple CBAM costs.” Similar drops were observed in Prakash Industries, falling from 24% to 19%, signaling tight margins and waning consumer demand. This decline affirms the negative sentiment pervading the sector.

The Neelachal Ispat Nigam saw a slight increase, but this is largely insignificant against a backdrop of uncertainty tied to the CBAM’s imminent implementation. Despite overall stability in some plants like Khorasan, other activities remain adversely affected by the geopolitical and logistical challenges detailed at the Irepas meetings.

Evaluated Market Implications

As observed, significant supply disruptions are anticipated, especially for plants like Prakash Industries and Tata Metaliks, due to constrained activity and rising operating costs influenced by energy prices and compliance burdens. Steel buyers should take immediate actions to secure short-term contracts with verified suppliers, particularly those positioned to adapt to the upcoming CBAM directives.

The insights from “Irepas: CBAM will give preference to proven plants by 2027” indicate that consumers should prioritize establishing relationships with mills that can demonstrate verified emissions data. As the landscape evolves with tighter regulatory frameworks, this proactive approach may mitigate the impacts of further disruptions and sustain procurement reliability amidst prevailing negative market sentiment.