From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Faces Downturn Amid Weak Demand and High Inventory Levels

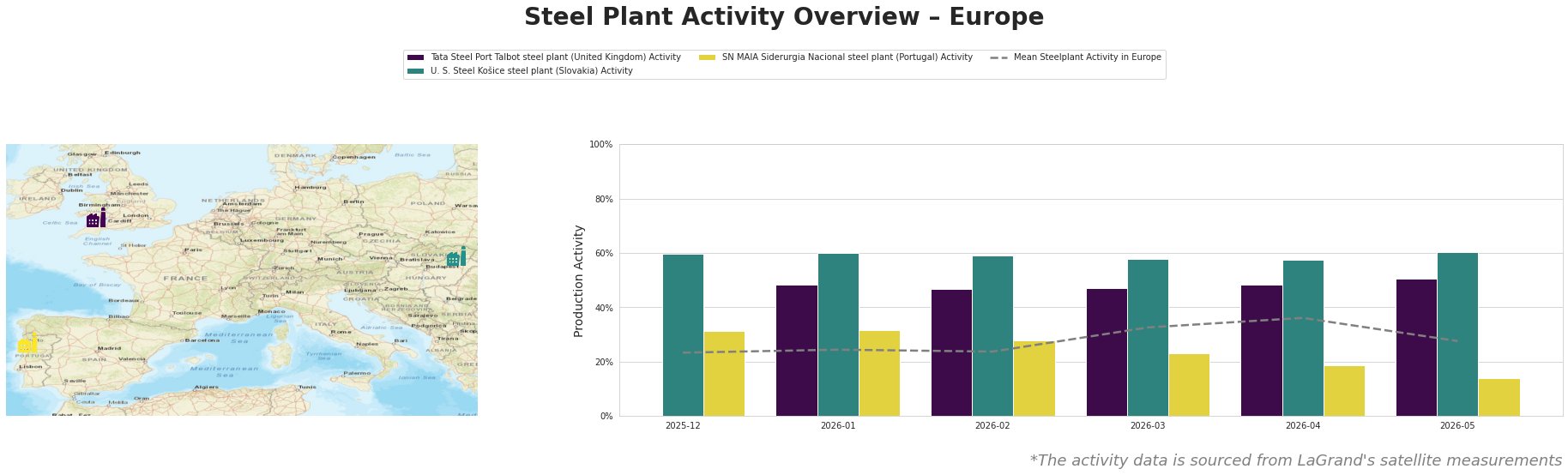

The European steel market is experiencing significant challenges due to weakened demand and elevated inventory levels. According to the article Muted activity caps European HRC prices; no near-term recovery seen, recent trading in the hot-rolled coil (HRC) market has been subdued, resulting in stable prices and dismal market sentiment. This sentiment is reflected in the satellite-observed activity levels of steel plants, notably with the European mean steelplant activity dropping to 28% in May 2026.

The Tata Steel Port Talbot plant in the UK displays a recent activity of 50% in May 2026, a slight improvement from the previous month, which may relate to ongoing efforts to stabilize operations amidst overall market struggles. Conversely, the U. S. Steel Košice plant maintains higher activity at 60%, reflecting its position in a challenging environment. However, the SN MAIA Siderurgia Nacional has plummeted to 14%, marking a declining trend amid weak demand and lower sales correlated with the broader market issues outlined in Local European steel heavy plate prices stable in Italy on weak demand; wider deal range heard in Germany.

The European longs market cools down amid holidays, production stoppages, and weak demand; safeguard measures also in focus article indicates that the market is reeling from production stoppages and weak demand, directly impacting plant operations and highlighting risks of supply disruptions. The declining activity at the SN MAIA plant aligns with these broader concerns, making it essential for buyers to monitor specific plants closely for potential sourcing volatility.

Given these developments, steel buyers are advised to:

- Prioritize procurement from the U. S. Steel Košice plant as it remains stable in activity and could symbolize a reliable supply source amidst a cooling market.

- Negotiate prices with suppliers taking into account high inventory levels and potential overstock situations, particularly in the HRC segment, as underscored by the Protectionism, the costs of combating demand in coil pricing in the EU article.

- Consider alternative suppliers or fallback options, especially from the Turkish market mentioned in the recent articles, to mitigate risks associated with the weak dynamics in local European steel production.

The negative outlook, reinforced by recent activity data and market sentiment, underscores a cautious approach for procurement in the current landscape.