From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNeutral Steel Market Sentiment in Europe Amid Rising Trade Barriers and Declining Activity

Recent developments in the European steel market highlight a Neutral sentiment as trade barriers increase, particularly affecting Ukrainian steel producers. Articles such as “The euroquote on steel will hit hard the Ukrainian metallurgists affected by the war, – CEO ‘Interpipe’” and “Ukraine needs to be exempted from steel quotas as part of a new EU trade event, Luca Zanotti“ emphasize the detrimental impact of new EU tariffs and quotas on Ukraine, which has seen a production decline of 80% due to ongoing conflict with Russia. This backdrop aligns with observed activity reductions in European steel plants.

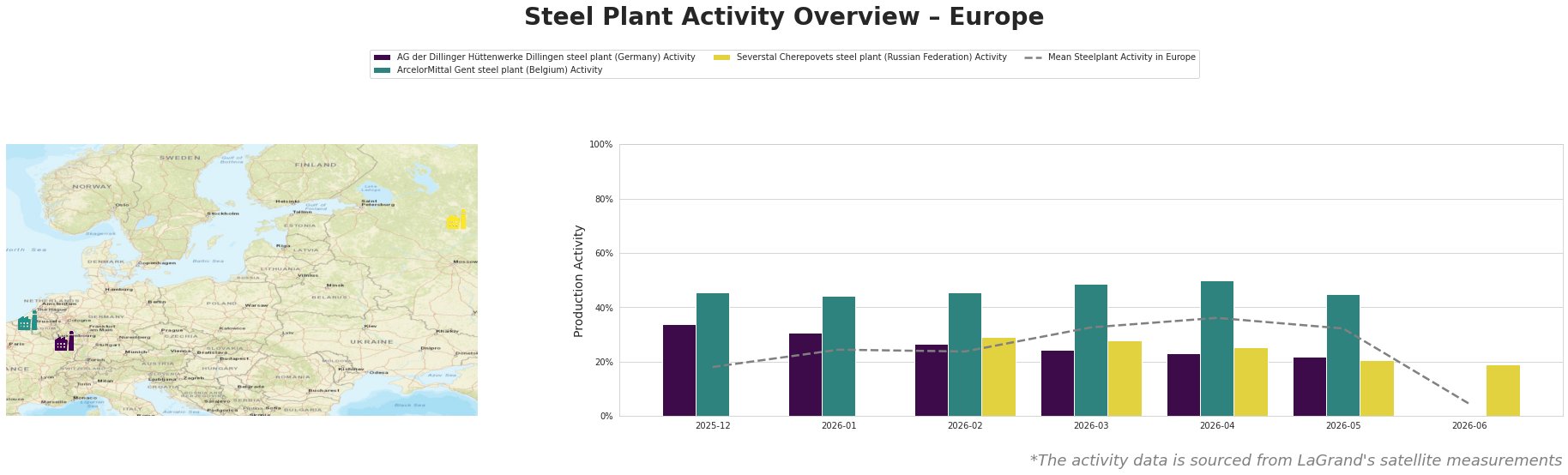

Activity levels across the observed steel plants indicate significant fluctuations. The AG der Dillinger Hüttenwerke Dillingen steel plant’s activity fell from 34% to 22% between December 2025 and May 2026, while ArcelorMittal Gent peaked at 50% in April 2026 before declining to 45% in May. The Severstal Cherepovets plant also experienced a steep drop to 20% in May and further down to 19% in June, likely tied to broader market uncertainties. While the mean activity level across all plants sharply declined to 4% in June 2026, this seems indirectly linked to the aforementioned trade barriers and tariffs highlighted in the news articles, though exact correlations for specific plants remain unconfirmed.

The AG der Dillinger Hüttenwerke Dillingen plant, situated in Saarland, has notably witnessed production shrink from a higher activity level of 34% in December to 22% by May 2026. This decline may reflect shifts in procurement strategies in response to EU trade policies but lacks explicit connection to reported news, as direct cause-effect dynamics have not been firmly established.

In contrast, the ArcelorMittal Gent steel plant in Vlaanderen maintained higher operational capacity with activities declining from 50% to 45% recently, potentially indicating resilience against market volatility. Nonetheless, the news concerning increased tariffs, as noted in “The UK has announced new tariffs on steel imports for the transition period,” underlines mounting pressure within the EU steel supply chain, hinting at adjustments needed in procurement practices.

The Severstal Cherepovets plant, primarily dependent on the Russian market, experienced a dramatic drop from 28% to 20% during the same period, raising concerns regarding potential supply disruptions. This situation, coupled with weakening production capacity due to geopolitical tensions, highlights a critical need for strategic sourcing decisions.

Given these market dynamics, steel procurement professionals are advised to:

- Monitor Supply Sources: Stay updated on developments affecting Ukrainian steel production as new tariffs may disrupt traditional supply routes, as indicated by the Interpipe CEO’s warnings.

- Adjust Procurement Strategies: Consider securing alternative suppliers and adjust inventory strategies in light of the potential supply shortages particularly from affected regions.

- Analyze Market Movements: Pay special attention to operational fluctuations among European steel plants, especially in light of recent tariffs and the overall production environment.

These considerations aim to enhance resilience against the currently neutral yet potentially volatile European steel market.