From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNegative Outlook for European Steel Market Amid Sanction-Driven Activity Declines

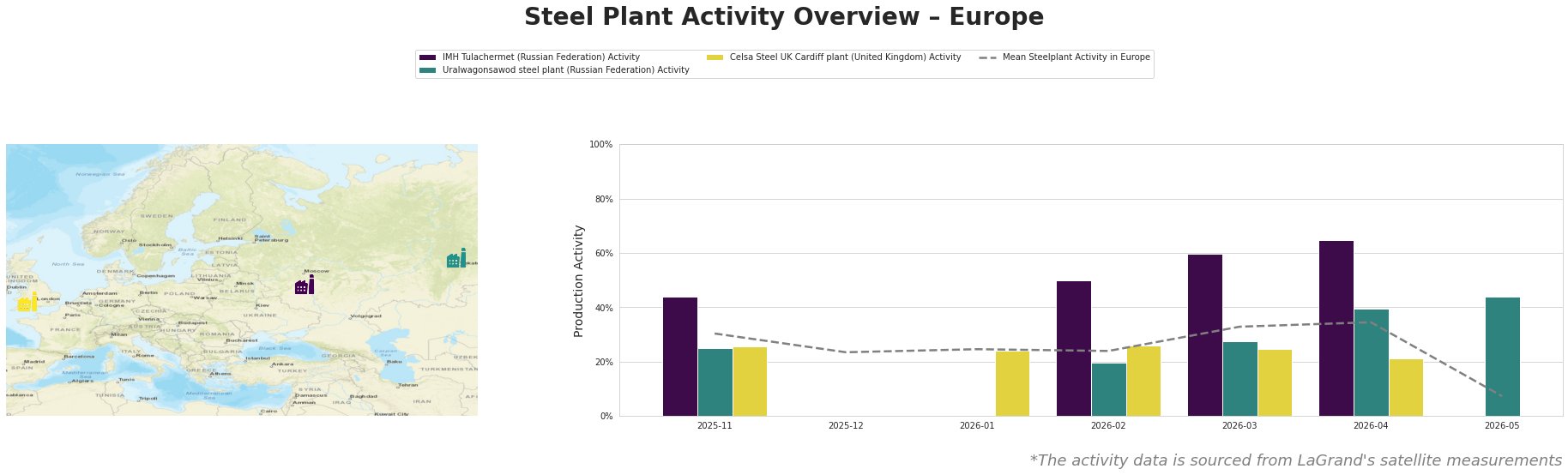

The European steel market is currently facing a negative sentiment due to recent sanctions placed on Russia and Belarus, as highlighted in the articles “EU widens Russia sanctions to scrap, metal goods“ and “EU’s 20th sanctions package further tightens restrictions on Russian steel-linked trade.” Satellite data reflecting a significant decrease in activity levels at various steel plants corroborates this trend. Notably, activity at the IMH Tulachermet plant dropped to 65% in April 2026, peaking at 60% in March after reaching a low of 23% in December 2025.

IMH Tulachermet, located in Tula, has seen its activity level plummet, having dropped from a high of 65% in April to an expected decrease to just 7% by May 2026. This decline aligns with the sanctions reported in “EU widens Russia sanctions to scrap, metal goods,” which restrict markets crucial to this plant’s operations. The facility, operating primarily on integrated processes with key products like rebar and wire rod, is particularly vulnerable to the new restrictions placed on the import and export of its metal products.

Conversely, Uralwagonsawod’s activity also fell from 40% in April to 44% in May despite the sanctions. However, no specific link between its observed activity levels and the recent sanctions can be established. Data indicates consistently low activity, suggesting a more severe and ongoing issue rather than a direct consequence of recent sanctions.

At Celsa Steel’s Cardiff plant, activity declined from 26% in March to 21% in April and remains unmonitored for May. Although it predominantly operates an electric arc furnace to produce semi-finished and finished rolled products aimed at construction and machinery, its performance similarly reflects the overall drop in market confidence driven by the sanctions outlined in “EU’s 20th sanctions package further tightens restrictions on Russian steel-linked trade.”

Given the evident supply disruptions nearing the steel plants due to substantial sanctions on metal products from Russia, it is advised for steel buyers to secure contracts while exploring alternative suppliers outside the affected regions. Immediate procurement actions should be taken to mitigate risks, especially from facilities like IMH Tulachermet, where production may not only see shortages but considerable delays tied to the sanctions framework. These proactive measures will be crucial to maintaining supply chains and meeting demand in the uncertain landscape ahead.