From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineRussian Steel Market Sentiment Declines Following EU Sanctions on Metal Products

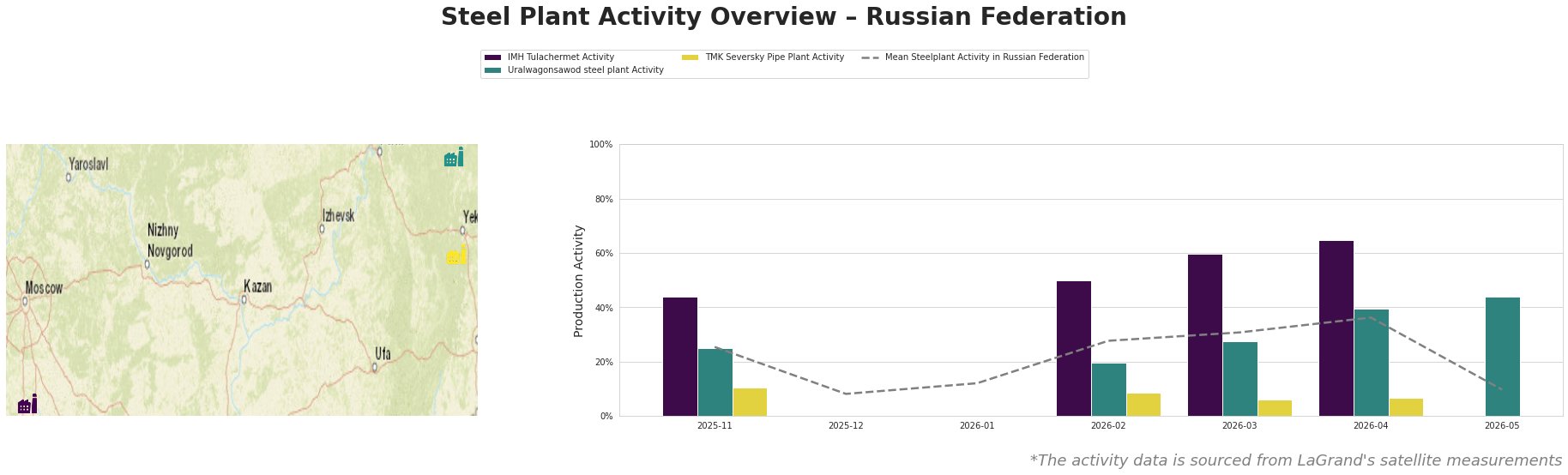

The steel market sentiment in the Russian Federation has turned negative, primarily triggered by escalating sanctions from the EU. The recent articles titled “EU widens Russia sanctions to scrap, metal goods” and “EU’s 20th sanctions package further tightens restrictions on Russian steel-linked trade” elucidate how strict new trade barriers are adversely affecting steel production activities. Notably, satellite data reveals significant declines in the operational rates of key steel plants correlating with these regulatory updates.

The IMH Tulachermet plant in Tula showed a peak activity of 65% in April 2026, but plummeted to 0% by May, suggesting a sharp decline likely influenced by the EU’s 20th sanctions package further tightens restrictions on Russian steel-linked trade. In contrast, the TMK Seversky Pipe Plant has exhibited poor activity levels, dropping to 6% in March. This plant’s activity has shown considerable volatility, likely tied to export restrictions detailed in both mentioned articles.

Uralwagonsawod steel plant’s activity dropped marginally despite earlier consistency, showing a correlation with the sanctions but lacking explicit satellite activity data around those dates. Importantly, no direct link can be established for Uralwagonsawod’s performance decline.

Evaluated Market Implications:

The newly imposed EU sanctions present significant supply chain risks for Russian steel buyers. The cessation of activities at IMH Tulachermet and TMK Seversky Pipe Plant raises concerns about procurement continuity. Buyers should actively monitor alternative sourcing options, especially regarding semi-finished and finished rolled products.

Steel buyers in the Russian market should prioritize:

- Diversifying Suppliers: Considering the unpredictable activity in major plants, establishing relationships with alternative regional producers may mitigate supply risks.

- Stockpiling: Given the evident instability in production levels, securing excess inventory of critical steel products may be prudent until market conditions stabilize.

- Contractual Flexibility: Procurement teams should negotiate for clauses that accommodate supply disruptions or changes in lead times, emphasizing the need for adaptability in current procurement strategies.

These actions, supported by observable site activity changes and strict new regulations, will be vital in navigating this challenging market landscape effectively.