From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineUkraine Steel Market Report: Sharp Declines Amid Increased Quota Pressures

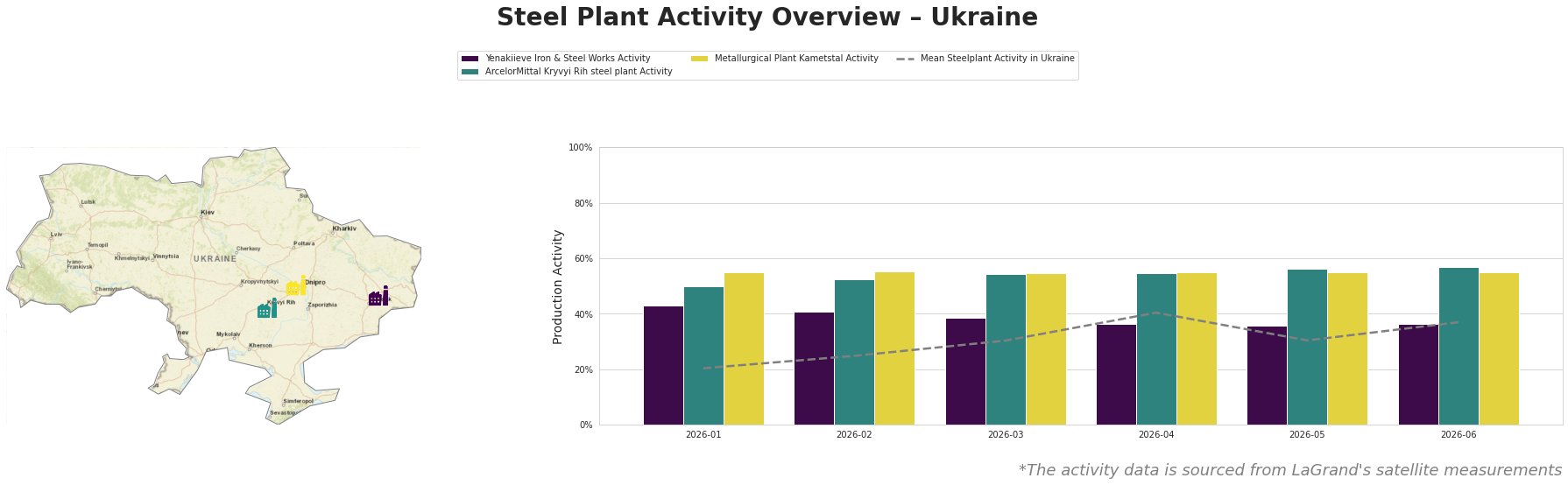

Recent developments in Ukraine’s steel market indicate a very negative outlook as activity levels at major steel plants decline sharply. The British Chamber of Commerce and Industry (BCC) warns about impending steel import quotas set to take effect on July 1, 2026, which could impose substantial challenges on suppliers dependent on external markets. This aligns with satellite-observed reductions in steel production at key facilities in Ukraine, as evidenced by the monthly activity reports.

Activity at Yenakiieve Iron & Steel Works demonstrates considerable stability at 36% in June 2026 but remains below the historical averages, partially linked to the uncertainty in British import quotas as detailed in the “Tariff quota negotiations are politicizing European steel imports“ article. This stagnation indicates potential challenges in meeting domestic demand amidst tightening international trade conditions.

ArcelorMittal Kryvyi Rih, exhibiting a gradual increase to 57% in June, indicates a lag compared to pre-established benchmarks, possibly instigated by concerns from British steel fabricators calling for the new steel measures to be revised. Such discrepancies suggest that upcoming governmental regulatory changes may disrupt existing supply chains, pressuring production capabilities.

The Metallurgical Plant Kametstal has maintained stable activity levels at 55%, likely reflecting ongoing challenges as raised in “Measures to protect the UK steel industry continue to provoke a negative reaction from the industry, despite the updates“, emphasizing the difficulty in sourcing required materials.

The significant discrepancies in activity levels at these plants signal possible supply disruptions for steel procurement in the short to medium term.

Given the current market landscape, it is advisable for steel buyers to consider increasing procurement ahead of anticipated supply tightening and price increases, particularly for critical segments such as rebar and wire rods, which are forecasted to face shortages. Additionally, continuous monitoring of import quota negotiations will be crucial to mitigating risks associated with supply chain disruptions, especially in light of impending tariff implementations.