From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope’s Steel Market: Navigating New Quotas Amidst Neutral Sentiment

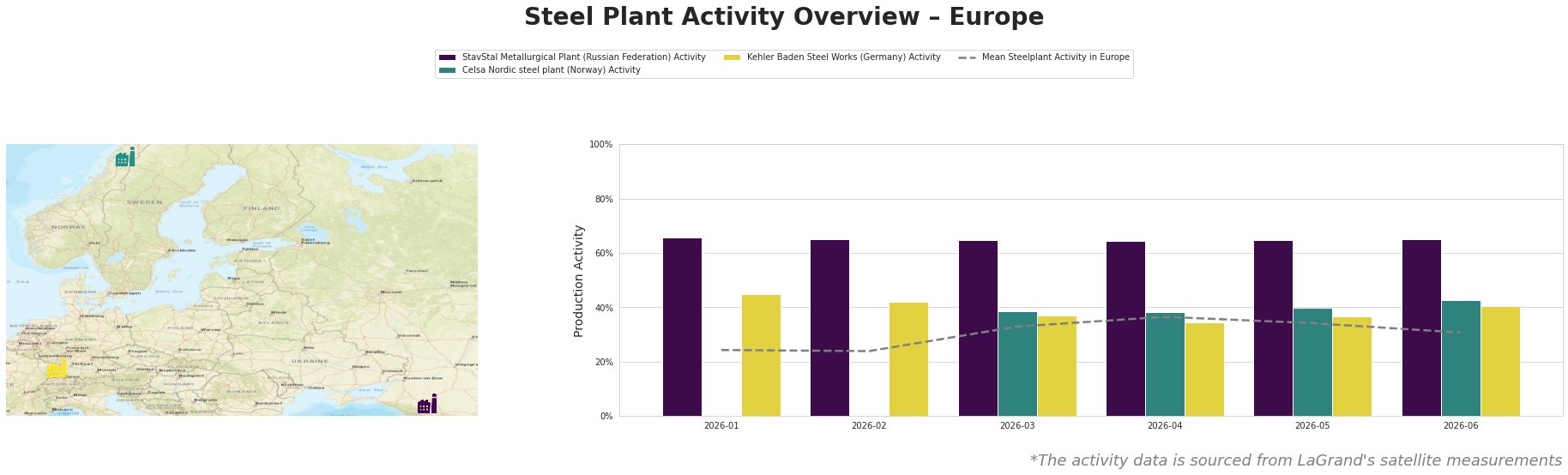

In Europe, steel market stability is being disrupted by new protective measures, particularly affecting the UK and EU. As reported in “In Britain, warnings are being issued about the threat to business posed by new steel import quotas“, the British Chamber of Commerce has highlighted significant financial implications for SMEs due to impending restrictions on import quotas and tariffs starting July 1, 2026. These changes are mirrored in the EU’s approach, elaborated by “Tariff quota negotiations are politicizing European steel imports,” indicating a chilling effect on procurement trends. Recent satellite observations reveal a continued impact on activity levels at key steel plants, albeit showing moderate fluctuations.

The StavStal Metallurgical Plant has maintained high activity levels (66%) but has not shown growth from earlier months, reflecting a stable yet unchanging output. This stability does not correlate directly to the ongoing market fears surrounding new trade negotiations, particularly those in “Tariff quota negotiations are politicizing European steel imports.” The Celsa Nordic Steel Plant shows an activity rise to 43% in June, yet overall it has fluctuated around a lack of clear demand drivers given recent tariff uncertainties. Conversely, the Kehler Baden Steel Works saw a decrease from 42% in February to 37% in March, indicating a declining trend, perhaps connected to external pressures as noted in the wider market discussions.

The observed reductions in mean activity levels overall, from 37% in April to 31% in June, align with the anxiety about the strict import quotas being enacted. The “UK has published details of new protective measures concerning steel” suggests that such measures may further exacerbate supply chain uncertainties and contribute to rising manufacturing costs across specific segments.

With significant cuts to tariff-free import quotas, as highlighted in “UK eases new steel import quota cuts to 51% instead of 60%“, steel buyers should prepare for potential shortfalls. Immediate procurement efforts should focus on securing contracts before the July deadline to mitigate cost increases associated with new tariffs, particularly for products facing quotas that are not sufficiently available domestically.

In conclusion, procurement personnel should prioritize establishing flexible sourcing strategies, especially given the expected competitive pressures stemming from import restrictions. Emphasis on building relationships with suppliers in regions less impacted by quota cuts can enhance resilience against future disruptions stemming from these legislative shifts.