From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Outlook for Europe’s Steel Market Amidst Demand Stability and Strategic Quotas

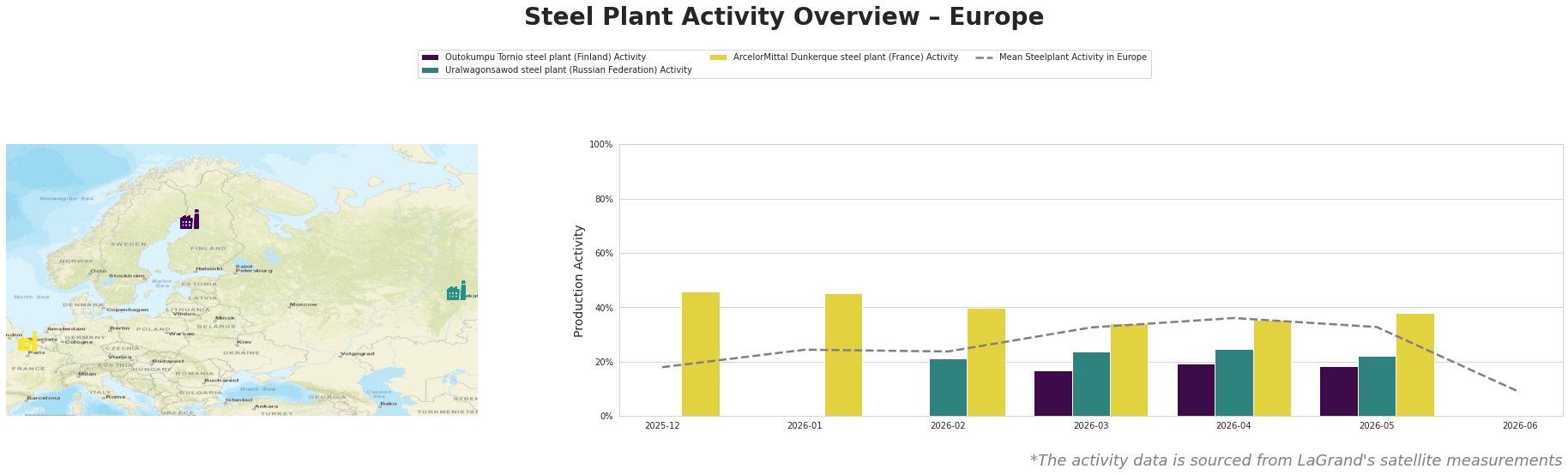

The steel market in Europe is experiencing a positive sentiment as evidenced by recent developments. Notably, the article “EU HRC market shows modest domestic demand, while import trade is thin amid quota uncertainty” indicates that despite modest domestic demand and stable business activity, pricing remains competitive, particularly in northern Europe where HRC offers are around €700/mt ex-works. Satellite data correlating to plant activity illustrates some stability, with plants such as Outokumpu and ArcelorMittal Dunkerque maintaining decent operational levels, although the latter has seen a recent uptick in activity amidst positive market projections.

The Outokumpu Tornio plant, which operates two Electric Arc Furnaces (EAF) with a capacity for 1.2 million tonnes of crude steel, has remained stable at 19% activity in May, reflecting consistent demand for its products in sectors like automotive and energy. However, there were notable declines in January and December, where activity was at 0%, with no direct news connection established during those months. This stability may be related to the positive outlook indicated in the EUROMETAL meeting, where stakeholders discussed the necessity of a green transition that could positively influence future demand and activity.

Conversely, the ArcelorMittal Dunkerque plant, with a significantly larger capacity, fluctuated between 34% and 38% activity in May despite pressure from the Carbon Border Adjustment Mechanism (CBAM) affecting pricing dynamics. The concerns about increased import costs due to these adjustments, highlighted in the article “European heavy plate round-up: Italian plate prices down further, re-rollers squeezed by CBAM,” suggest that Dunkerque could see further demand if prices stabilize.

The Uralwagonsawod, which has not been adequately tracked in recent reports and has remained below 25% activity, does not presently tie into the broader market discussions, making it difficult to predict potential disruptions independently.

Potential Supply Implications: Given the complexities around evolving regulations and potential port quota distributions—especially under “European flat steel imports market subdued, eyes on safeguard outcome”—there may be supply disruptions if mills cannot adapt to the incoming quotas. Therefore, buyers in sectors dependent on HRC and heavy plates should proactively assess inventory levels and be prepared for potential shortages as they align procurement cycles with market fluctuations.

Recommended Actions: Steel buyers should closely monitor the impact of the upcoming quotas effective July 1 and consider placing orders for HRC from established suppliers where pricing remains competitive, particularly from Turkish and Algerian sources, before any further adjustments proliferate. Additionally, fostering relationships with plants that showcase stable activity levels like Outokumpu and ArcelorMittal could mitigate risks associated with potential regulatory shifts and market volatility.