From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope’s Steel Market Sentiment Holds Steady Amid Import Quota Revisions and Activity Changes

In Europe, the steel market remains neutral as notable developments occur surrounding import quotas in the UK. Articles like “British steel fabricators are calling for the new steel measures to be revised“ and “UK confirms reduction of import quotas by 51%“ shed light on new government policies that could disrupt supply chains and affect competition. These changes coincide with observable trends in plant activity reported through satellite data, though no direct correlation was identified between specific plants and the new import measures.

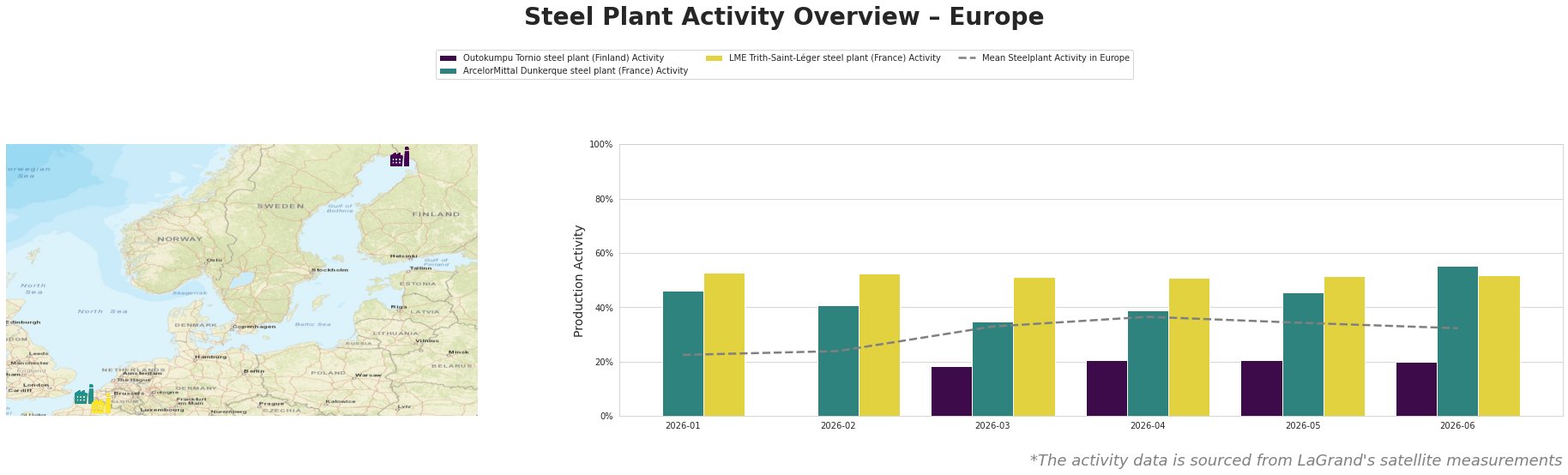

In reviewing the activity levels, Outokumpu Tornio steel plant has shown a gradual decline, falling from 21.0% in April to 20.0% in June, hovering significantly below the mean level. This drop does not align directly with the news on adjustments to UK tariffs.

Conversely, ArcelorMittal Dunkerque has maintained robust activity, peaking at 55.0% in June, correlating with its resilience amid pressures such as increased costs from new tariffs discussed in “UK eases new steel import quota cuts to 51% instead of 60%“. Notably, it outperforms the mean, indicating a stable demand in its operational domain.

LME Trith-Saint-Léger has maintained consistent activity at around 52.0%, remaining stable despite ongoing uncertainty in surrounding markets, with no specific link to activity fluctuations and the recent tariff alterations.

The implications of the UK’s protective measures, as highlighted in the article “UK adjusts EU import quotas after agreement is reached,” signal potential supply disruptions, notably for products that are critical domestically but not sufficiently produced. Steel buyers should consider immediate procurement actions to mitigate risks of shortages, particularly for specialty products impacted by diminished local production capabilities.

Additionally, buyers should closely monitor developments regarding the transition to low-carbon steel procurement emphasized in articles like “Measures to protect the UK steel industry continue to provoke a negative reaction from the industry, despite the updates.” Keeping an agile procurement strategy may serve as a buffer against rising costs associated with increased tariffs on imported steel and unstable supply chains.

In conclusion, while the market sentiment remains neutral, the observed activity levels hint at the potential for increased volatility in supply, necessitating proactive engagement by steel buyers to anticipate shifts in availability and pricing.