From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Report: Rising Activity amid New Regulations and Tariff Changes

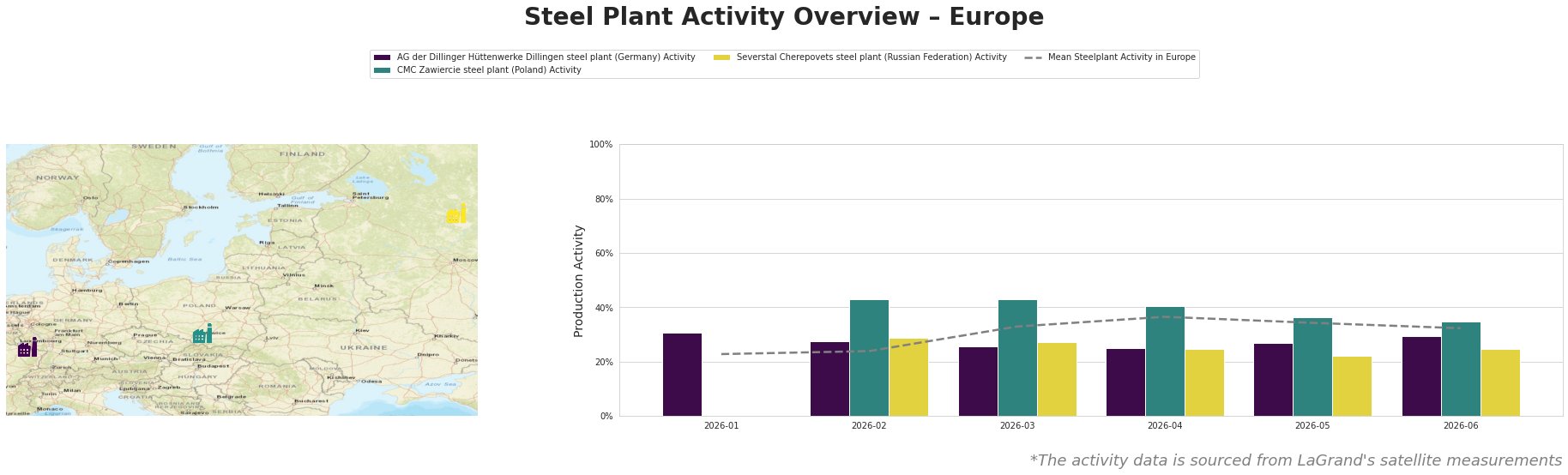

The European steel market is witnessing a very positive shift, fueled by recent regulatory changes and an uptick in plant activity levels. Key developments include The EU’s requirement regarding the smelting and casting of steel will come into force in October, which anticipates heightened scrutiny on steel imports, and EU’s new steel regulation published in the official journal, including “Melt and Pour” requirement and 50% tariff, aimed at controlling global steel overcapacity. These legislative updates correspond with increased satellite-observed activity at several major European steel plants, confirming a recovery in production levels.

The AG der Dillinger Hüttenwerke plant in Germany shows a stable upward trend, particularly with a notable activity level of 31% in January, peaking at 37% in April before correcting slightly to 29% in June. The CMC Zawiercie steel plant saw significant variability, achieving its highest activity at 43% in February and March, reflecting its operational agility in the face of demand. Although rising from 40% in April to 36% in May, it stabilized at 35% in June. Severstal Cherepovets remains the least active plant, showing consistent levels between 22% and 29%, indicating less responsiveness to regulatory changes, particularly those in the EU market.

The implications of the newly introduced “Melt and Pour” requirement can be seen reflected in the AG der Dillinger Hüttenwerke’s operational adjustments, likely aiming for compliance with enhanced transparency ahead of the regulation’s enforcement in October. Similarly, the high activity levels at CMC Zawiercie suggest a proactive approach to align production capabilities with market demands and newly imposed tariff regimes.

In light of these developments, procurement professionals should consider the following recommendations:

– Leverage increasing output from compliant European plants like Dillinger and Zawiercie to meet immediate supply needs as non-compliant imports face stiffer tariffs.

– Monitor the stakeholder discussions post-October 2026 for further adjustments and compliance issues with the EU’s smelting and casting rule that might affect supply chains.

– Given the regulatory landscape, buyers might find better pricing and availability from high-activity plants ahead of anticipated market adjustments driven by new tariffs.

This strategic focus could result in optimized procurement and greater resilience in supply chain management in the forthcoming months.