From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Surge: Strong Activity Levels and Positive Outlook

Recent data analysis and news updates indicate a very positive sentiment in the European steel market as observed through increased activity levels at major steel plants. Notably, the article Union pauses strikes at Australia’s Ichthys LNG: Update highlights ongoing negotiations enhancing operational confidence, although primarily focused on LNG, reflects a broader trend affecting global energy-intensive industries, including steel production. Satellite data aligns with this sentiment, showing resilience and growth in steel plant activities.

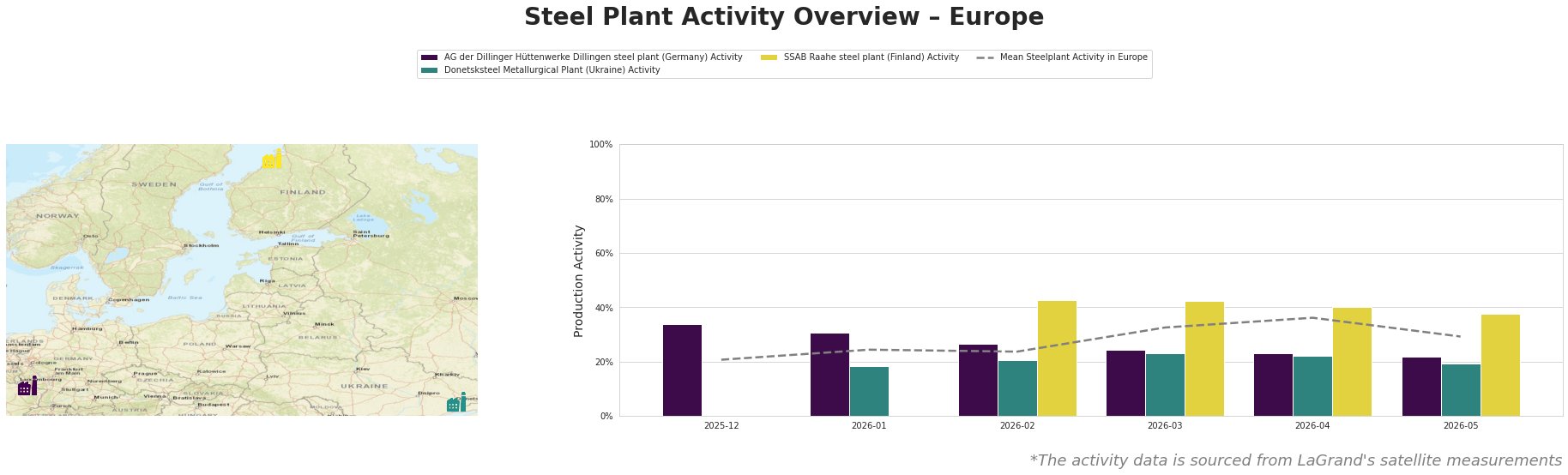

The AG der Dillinger Hüttenwerke Dillingen steel plant in Germany operated at 34% activity at the end of December 2025, but has had a steady decline to 22% by May 2026. The decrease does not appear to have a direct connection to any identified news events. In contrast, SSAB Raahe showed fluctuating activity peaking at 43% in February but experienced a decline to 38% in May 2026. The Donetsksteel Metallurgical Plant remained largely inactive, with activity dropping from 20% to 19% through early 2026, which may be attributed to ongoing local conflicts rather than recent news.

The overall mean activity increased from 21% at the end of 2025 to a high of 36% in April 2026, signaling a recovery trend across the industry that may encourage procurement professionals to consider strategic buying as confidence rises.

The strongest signal for buyers comes from the potential increased demand reflected in the Q&A: Australia’s Santos plans growth in PNG, Alaska, which underscores a global energy initiative influencing supply chains, including steel, fueled by a parallel demand for fossil fuels and their by-products.

Given the notable disparities in activity levels, procurement teams should consider elevating orders at the SSAB Raahe plant while monitoring Dillinger’s declining output closely. Furthermore, strategic supply agreements could mitigate risks associated with the Donetsksteel plant’s instability. Diversification of procurement sources across these plants could ensure more stable supply chains moving forward.