From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market Report: Neutral Sentiment Amid Rising Import Duties and Output Challenges

Recent developments in Europe’s steel market are shaped predominantly by Ukraine’s ongoing situation and the EU’s trade measures. Articles such as “Ukraine has extended anti-dumping measures on imports of seamless pipes from China“ and “Domestic prices for hot-rolled steel and pipes rose by 9–10% in May“ illustrate critical trade dynamics, where domestic pricing dynamics continue to be influenced by geopolitical factors and protective measures.

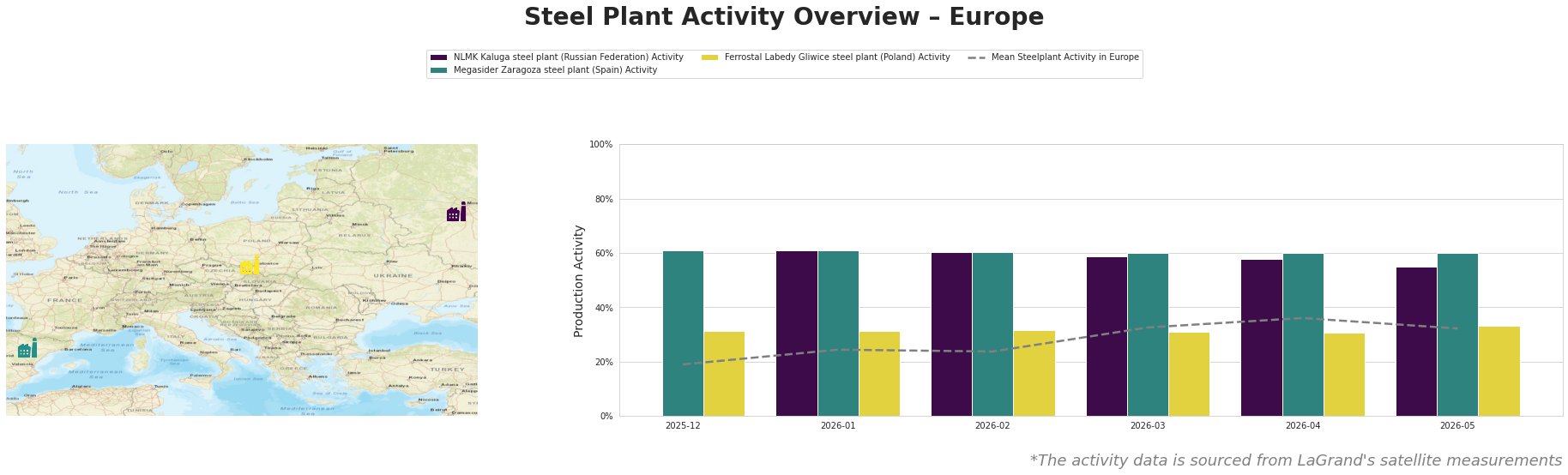

While activity levels remain neutral, satellite data indicates that NLMK Kaluga’s output dropped to 55% activity in May, aligning with the context set by Luca Zanotti’s recent articles, particularly “The EU steel quota will hit Ukrainian steelmakers affected by the war hard – Interpipe CEO,” which emphasizes the ongoing struggles of the Ukrainian steel industry that has declined by 80% since the onset of the war.

The NLMK Kaluga plant predominantly utilizes Electric Arc Furnace (EAF) technology and serves a market for semi-finished and finished rolled steel products. Its recent drop in activity from 58% to 55% in May reflects broader market pressures alongside Ukraine’s critical steel sector decline and protective measures indicated in “Ukraine should be exempted from steel quotas under the EU’s new trade measure – Luca Zanotti.”

The Megasider Zaragoza plant maintained a stable 60% activity level, indicating resilience within Spain’s steel sector. Given that this facility focuses on finished rolled products primarily for building and infrastructure, Spanish steel buyers could continue procurement without expectation of immediate disruption—though vigilance is advised given fluctuating regional dynamics.

On the other hand, Ferrostal Labedy in Gliwice slightly increased to 33% activity levels, which might suggest responsiveness to regional demand despite the general market sentiment. However, no direct news correlations are established with this uptick.

In summary, potential supply disruptions are likely, especially surrounding the Ukrainian steel supply chain due to expected increases in import tariffs, as highlighted in “The euroquote on steel will hit hard the Ukrainian metallurgists affected by the war.”

Recommendations for steel buyers:

– Investigate alternative sourcing from stable European plants, notably Megasider Zaragoza, given its steady output.

– Monitor pricing trends closely, especially post-July 1, when EU duties on steel imports rise to 50%, potentially creating supply gaps.

– Prepare for longer lead times or price increases for products linked to Ukraine-produced steel, particularly if trade barriers remain in place.