From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineAsia Steel Market Analysis: Positive Sentiment Amid EU Quota Shifts and Plant Activity Trends

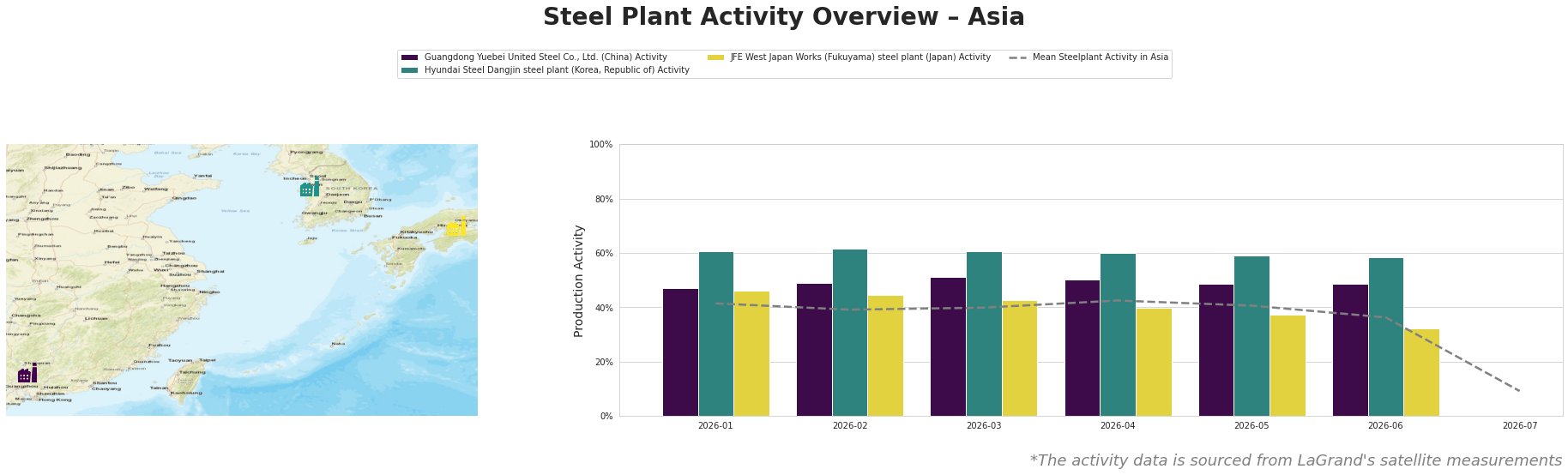

Recent developments in the steel market across Asia reflect a positive sentiment, influenced by notable changes in EU steel import quotas. The articles “EU cuts Türkiye’s steel quotas, except CR, tinplate“ and “EU steel import quotas exhausted for Turkey, South Korea, China and others as Q2 2026 ends“ shed light on the revised quantities impacting Türkiye and other nations, fostering shifts in plant activities in the region. The satellite data reveals a decline in activity at key production facilities, which aligns strategically with the evolving market landscape.

In the analysis, significant activity drops are reported across all observed plants in July 2026, particularly evident at the Hyundai Steel Dangjin steel plant and JFE West Japan Works. The recent “EU steel import quotas exceeded in several categories just three days into new period“ highlights the increased demand and urgency in fulfilling orders, potentially leading to temporary supply disruptions for areas dependent on these manufacturers.

The Guangdong Yuebei United Steel Co., Ltd. in China reported a stable activity level of 49% in June, maintaining comparatively better performance relative to the mean. This stability may indicate resilience amid quota reductions impacting Turkish and other regional competitors, suggesting a price support mechanism exists for Chinese products. However, the overall decline in activity could signal tightening supply and demand irregularities, necessitating proactive procurement strategies.

Hyundai Steel Dangjin steel plant showcased a drop in activity to 58% in June from 61% earlier in the year, coinciding with the heightened import quota strategies involving South Korea. The plant primarily focuses on automotive and infrastructure applications, indicating potential vulnerability should quotas influence raw material costs adversely.

The JFE West Japan Works has seen a notable drop to 32%, aligned with larger trends reported in the recent quota articles, indicating a potential slowdown in production likely due to scarce foreign demand and adjustments to inbound material procurement linked to the EU’s regulatory shifts.

In light of these insights, steel buyers in Asia should consider the following recommendations:

– Mitigate Supply Risks: Given the diminishing activity levels at Hyundai and JFE plants, it is advisable to secure procurement commitments ahead of anticipated delays due to heightened quota activity and regional competition.

– Focus on Chinese Supply Options: Take advantage of stable performance from Guangdong Yuebei. Strategically prioritize orders to buffer against potential disruptions caused by observed drops in South Korean and Japanese outputs.

– Monitor EU Imports Closely: Regularly evaluate import quota usage by competing nations to inform pricing and production strategies, particularly as Turkey faces heightened scrutiny under the new quota system.

These strategies should be informed by ongoing market observations, ensuring adaptability to rapidly changing dynamics within the Asian steel market.