From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market Report: Negative Outlook for Asia Amidst Rising Costs and Low Demand

Steel activity across Asia is experiencing significant challenges, driven primarily by increased input costs and weak demand for finished products. Recent reports highlight key issues impacting the market, such as “Prices for coking coal rose in June,” indicating pressure on production costs due to supply restrictions in China, and the China Iron and Steel Association’s finding that “CISA mills’ daily crude steel output up 0.8% in mid-June 2026, stocks also up,” suggesting inventory levels are climbing while consumption remains stagnant.

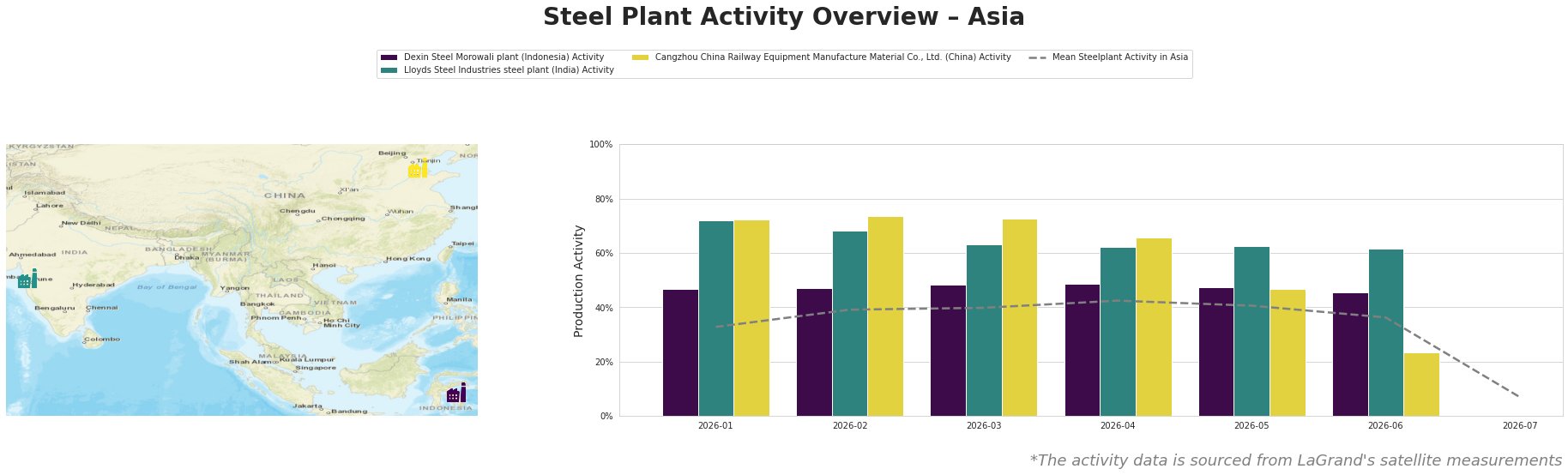

Recent Monthly Activity Trends

Dexin Steel’s activity decreased slightly to 45% in June from 48% in May, showing some resilience amidst pricing pressures. Conversely, the Cangzhou plant saw a dramatic drop to 23%, down from 47%, likely correlating with reported increases in inventories and weak demand as per the CISA report.

Plant Insights and Activity Dynamics

Dexin Steel Morowali in Indonesia focuses on integrated steel production and has exhibited stable activity with a June output of 45%, reflecting a minor decrease from the previous month. This stability is noteworthy compared to the rising coking coal prices documented in “Prices for coking coal rose in June,” creating a challenging backdrop for maintaining production levels. However, local demand dynamics appear to support ongoing activity.

Lloyds Steel Industries in India maintained a steady activity level of 62% in June, consistent with previous months. The plant’s consistent demand from sectors like energy products contrasts with the broader halt in market momentum as highlighted in multiple reports, including the CISA inventory statistics.

Cangzhou China Railway Equipment experienced a severe drop to 23% in June, down from 47% in May. The significant decline connects back to the CISA’s report indicating increasing steel inventories, highlighting a mismatch between production and consumption—a critical situation given the geopolitical tensions affecting supply as noted in “CSC: China production cuts and geopolitical tensions tighten global steel supply.”

Market Implications and Recommendations

In light of rising costs for raw materials such as coking coal and increasing inventory levels, several supply disruptions loom for the Asian steel market, particularly in regions heavily influenced by geopolitical factors, such as Taiwan and mainland China. Steel buyers should prepare for potential escalations in procurement costs and supply limitations.

Recommendations:

1. Monitor Coking Coal Prices: Engage in forward contracting for coking coal to hedge against further price increases, especially given its critical role in cost structures as demonstrated in recent activity shifts.

-

Adjust Procurement Strategies: Given the rising inventory and stagnant demand, buyers should consider tailoring their procurement volumes to align with shifting demand patterns, focusing on immediate needs rather than long-term stockpiling.

-

Diversify Supply Sources: Suppliers potentially affected by the geopolitical landscape should be diversified to mitigate risks of production cuts or stoppages tied to external conflicts.

-

Focus on Long-term Contracts: Establish partnerships with suppliers for secure long-term contracts, reducing exposure to price volatility demonstrated in recent market fluctuations.

Gathering insights from both plant activity patterns and broader economic factors will be essential for navigating this negative market sentiment effectively.