From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineUkraine Steel Market Analysis: Strong Activity Signals Growth Amid EU Import Quota Changes

Recent developments in the Ukrainian steel market are influenced by the EU unveils tighter steel import quotas, new allocation structure and EU introduces stricter steel import quotas and new distribution structure articles. These changes reflect a shift in import regulation, affecting Ukrainian steel exports as plants adjust their activities amidst tightening European market conditions.

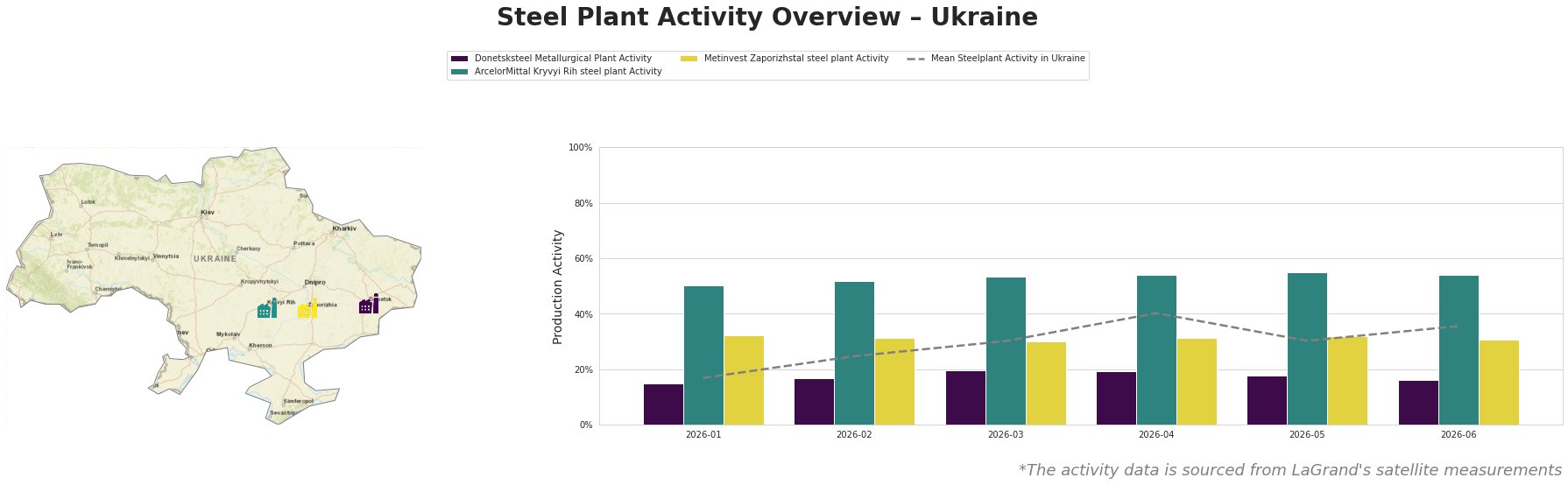

Across observed months, the mean steel plant activity in Ukraine peaked at 40.0% in April, reflecting a general recovery trend. However, by June, activity slightly decreased to 36.0%, closely following the article’s announcement of stricter import quotas.

The Donetsksteel Metallurgical Plant’s activity consistently remained below the average, with a maximum of 20.0% in March but falling back to 16.0% by June. This trend indicates challenges in ramping up production, possibly linked to the regulatory changes cited in the aforementioned news articles, although no explicit connection can be established directly.

In contrast, ArcelorMittal Kryvyi Rih demonstrated a robust performance, peaking at 55.0% in May, indicating its resilience and adaptability in the current market landscape. The recent shifts in EU quota policies that favor countries with existing FTAs may particularly benefit this plant under its established trade relationships, potentially enhancing its competitive edge in the EU market.

Metinvest Zaporizhstal showcased relatively stable activity levels, maintaining productivity around the 30% mark. The slight decrease from 32.0% to 31.0% in June suggests it has reached an operational plateau, possibly tied to broader market conditions impacted by EU export regulations, although no direct evidence ties these two factors explicitly.

Given the evidence from the news articles and observed steel plant activities, the following actionable insights emerge for steel procurement professionals:

-

Focus on ArcelorMittal Kryvyi Rih: Given its higher performance metrics and potential adaptability to the changing regulatory environment, prioritize procurement from this plant to ensure stable supply amidst tightening EU market conditions.

-

Monitor Donetsksteel’s Capabilities: As this plant falls significantly below the mean activity, closely monitor its operations for potential disruptions. Buyers should consider diversifying sources to mitigate risks associated with low activity levels.

-

Strategic Sleep Planning: With new EU import quotas likely affecting overall supply dynamics, steel buyers should proactively adjust their procurement strategies, potentially increasing orders from reliable sources before the pending quota impacts materialize.

By aligning procurement strategies with the ongoing market activities and regulatory changes, stakeholders can navigate the complexities ahead effectively.