From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market in Europe Faces Downturn Amid New Import Quotas and Decreasing Activity Levels

Europe is grappling with a negative market sentiment in the steel sector, driven by recent announcements and declining plant activity. The articles “EU announces new steel import quota volumes and implementation changes“ and “British industry risks losing markets due to changes in the EU“ highlight the EU’s efforts to address the challenges posed by global overcapacity, while satellite data indicates a worrying trend in steel plant activity levels.

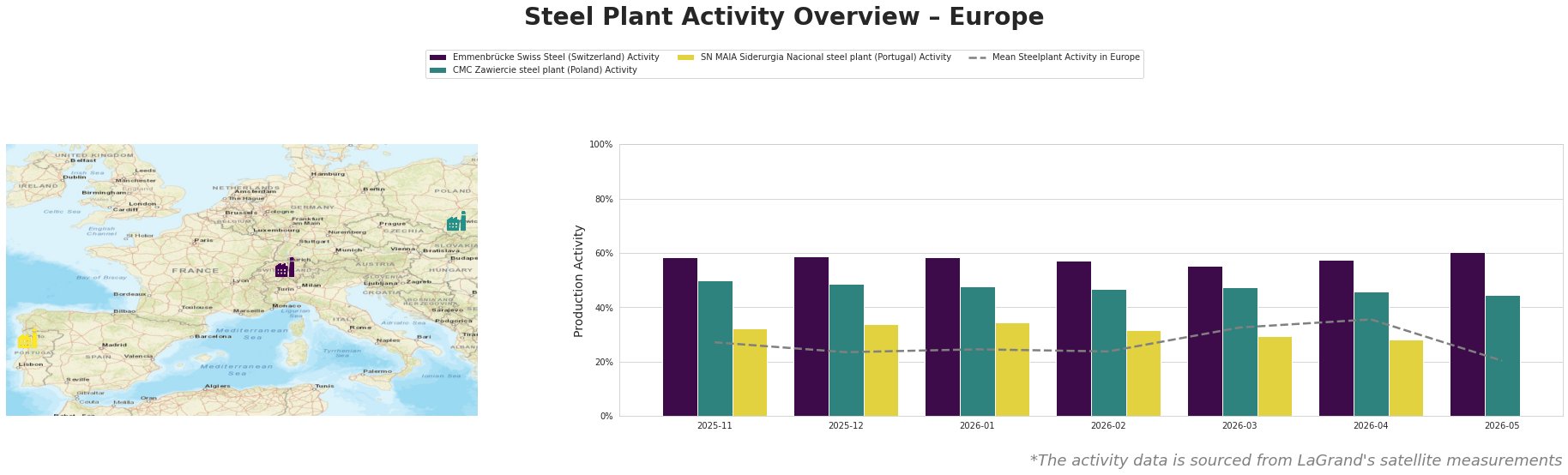

The general trend across the region shows a significant drop in activity, particularly notable in May 2026, when the mean activity plummeted to 20%, marking a 44% decrease from April. Emmenbrücke Swiss Steel exhibited the highest activity at 60% in May, while the CMC Zawiercie steel plant and SN MAIA recorded lower activity at 45% and an unspecified value, respectively. This decline aligns with the EU’s newly announced steel import quota, which may disrupt supply and adversely affect local production.

The CMC Zawiercie steel plant, primarily engaged in the production of steel for the automotive and infrastructure sectors, has seen a reduction to 45% activity as of May 2026, reflecting a broader trend of declining domestic demand and possibly linking to market uncertainties due to the upcoming import quotas discussed in “EU announces new steel import quotas and changes in their application.” This regulation seeks to curb excess imports while aiming to support domestic production amidst increased tariffs.

Emmenbrücke Swiss Steel also experienced a stable yet notably high activity level at 60% in the same month, reflecting a relatively better position compared to peers, although future projections remain uncertain due to changing trade dynamics.

Given these observations, steel buyers should prepare for potential supply disruptions, especially concerning CMC Zawiercie and SN MAIA, where activity levels are notably low and may impact their ability to meet demand. Furthermore, procurement strategies should pivot towards securing commitments with local producers, particularly from Emmenbrücke, as the EU’s quota regulations alter the market landscape.

To navigate these challenging market conditions, analysts should closely monitor changes in plant activity and remain proactive in seeking alternative sourcing options that align with evolving regulatory measures.