From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Steel Market Outlook in Asia: Activity Trends Driven by Recent Developments

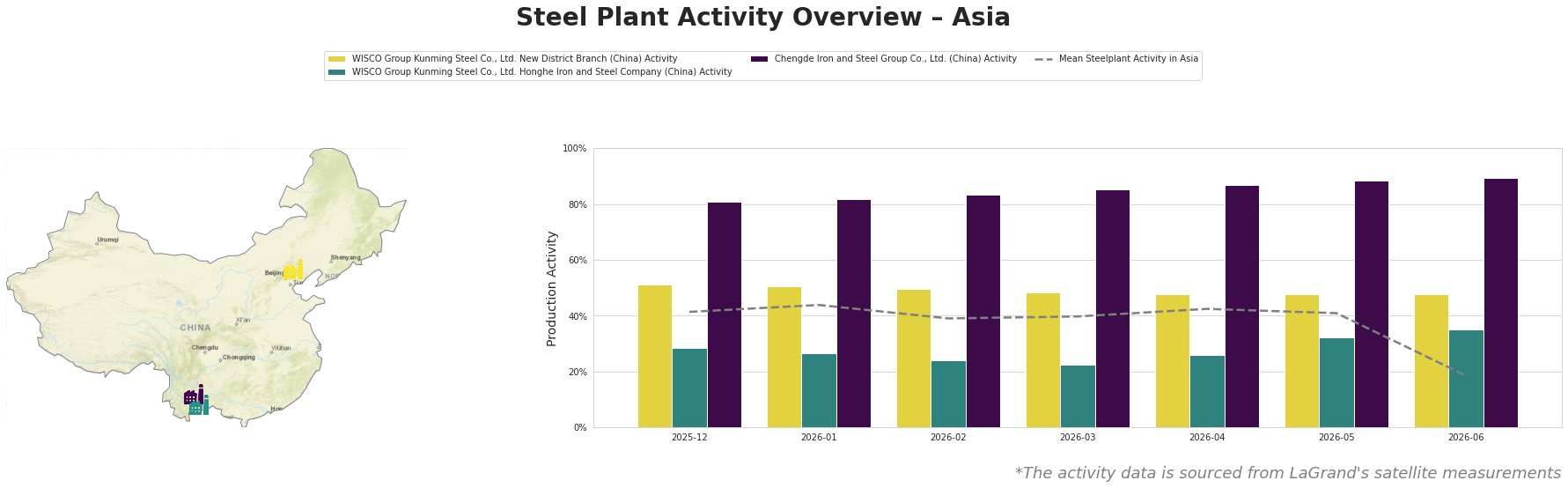

Recent activities in Asia’s steel market reflect a positive sentiment, particularly influenced by pivotal changes in China. Notably, China’s rolled steel exports fell by 8.1% y/y a five-month period and China’s steel exports down 8.1% in Jan-May, but up 8.9% in May 2026 from Apr highlight shifting dynamics as plant activities adapt. These developments correlate with observable shifts in satellite data, indicating a responsive market.

The activity levels at Chengde Iron and Steel Group peaked significantly in April at 87.0%, reflecting sustained demand in sectors like infrastructure amidst weak property sector performance. Conversely, the recent downturn to 19.0% mean activity in June contrasts with April’s highs, suggesting seasonal adjustments or localized challenges. This is not aligned with the observed increase in May exports from China’s market.

WISCO Group Kunming Steel Co., Ltd. New District observed stable activity around 51.0% but saw minor fluctuations. The slight decrease in February to 49.0% may link to the government’s new export licenses negatively impacting production dynamics, as aligned with China’s rolled steel exports fell by 8.1% y/y a five-month period.

WISCO Group Kunming Steel Co., Ltd. Honghe Iron and Steel Company displayed a gradual increase in activity, peaking at 35.0% in June. This increase contrasts with China’s overall export challenges, potentially indicating efforts at increased local or domestic market engagement.

Evaluated Market Implications: The decrease in China’s export figures signals possible supply disruptions in the international market but could lead to further stabilization in domestic pricing. Buyers should proactively adjust procurement strategies, particularly considering the fluctuation in activity levels post-May. Firms should evaluate contracts, especially for hot-rolled and cold-rolled products, aligning such strategies with observed peak production months (April-May) and projected demand shifts. These adjustments could position stakeholders favorably against emerging supply fluctuations and competitive pricing adjustments in Asia’s reinforced market backdrop.