From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Market Sentiment Drives Steel Activity in Europe Amid Climate Policy Developments

Recent events in Europe highlight a rising steel market sentiment following notable government developments and shifts in plant activities. Significant heatwaves in 2025, as outlined in “Europa erwärmt sich schneller als alle anderen Kontinente,” coupled with ongoing discussions on emissions trading reforms in “ETS: delayed responses, a cautious approach and key demand“ and “ETS: Delayed response, cautious approach, and basic requirements,” reflect both environmental challenges and an urgent call for industrial adaptation.

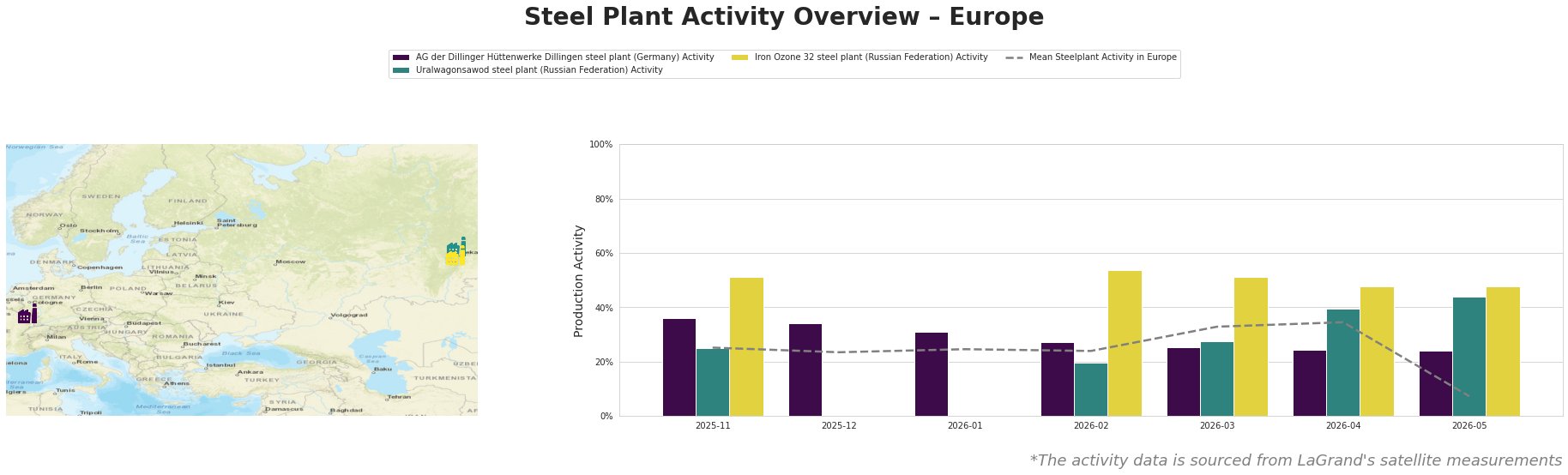

Table: Recent Monthly Activity Trends of Selected Steel Plants

The overall steel plant activity in Europe peaked at 35.0% in April 2026, indicating a recovery phase, although the subsequent month saw a sharp decline to 7.0%. Notably, the AG der Dillinger Hüttenwerke’s activity has shown a downward trend, reaching 24.0% in April, which indicates potential operational challenges exacerbated by climate factors as reported in recent news. Meanwhile, the Uralwagonsawod steel plant achieved a high activity rate of 44.0% in May, despite the simultaneous overall decline in Europe, reflecting strategic operational resilience. The Iron Ozone 32 plant, consistently maintaining activity levels around 48.0%, exhibits stable performance amidst fluctuating mean activity.

The lack of direct connections between the reported activity at AG der Dillinger Hüttenwerke and external developments indicates that operational adjustments might be necessary to counterbalance the risks posed by stringent carbon regulations discussed in the articles on the ETS.

Given the slower emissions trading reform pace emphasized in the recent Luxembourg government discussions, steel procurement professionals should consider diversifying their suppliers away from the AG der Dillinger Hüttenwerke to mitigate the risk of further operational disruptions. Alternatively, deeper engagement with Uralwagonsawod or Iron Ozone 32 may yield more stable sourcing channels as their outputs are reportedly more resilient to current environmental challenges and policy uncertainties.

To summarize, steel buyers in Europe should:

– Monitor AG der Dillinger Hüttenwerke for potential supply disruptions.

– Seek alternative sources such as Uralwagonsawod and Iron Ozone 32, whose activity levels indicate greater stability.

– Stay informed on the developments in ETS reforms for clearer insights into future cost structures and competitiveness in the European steel market.