From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineIndia Steel Market Report: Activity Trends Neutral Amid Fertilizer Sector Developments

Recent trends in India’s steel market show a Neutral sentiment as satellite-observed activities indicate fluctuations but no decisive trends, directly influenced by external factors rather than steel demand. Articles such as “India plans joint buying of fertilizers, raw materials“ and “India’s IPL issues tender to buy 1.6mn t of DAP/TSP“ highlight how joint procurement initiatives are being established due to supply chain challenges, indirectly influencing steel production dynamics.

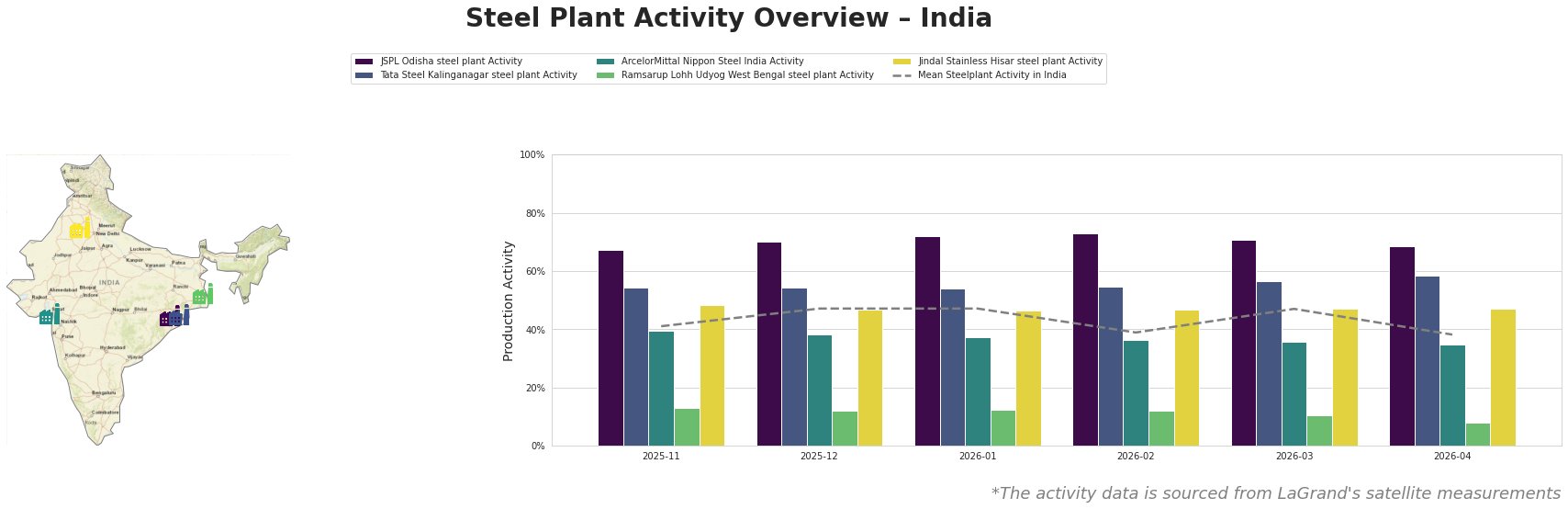

Activity levels across the observed plants demonstrate notable variability—particularly the JSPL Odisha plant, which peaked at 73.0% in February, while Ramsarup Lohh Udyog showed minimal activity, dropping to 8.0% in April. Notably, despite these fluctuations, there is no explicit connection to steel market disruption risks from the fertilizer sector straightforwardly establishing a direct or themed link.

The JSPL Odisha steel plant, primarily using integrated BOF and DRI processes with a production capacity of 6,000 MT of crude steel, reported a recent activity drop to 69.0%, likely influenced by broader procurement strategies amidst fertilizer sector changes highlighted in “India plans joint buying of fertilizers, raw materials.”

In contrast, Tata Steel Kalinganagar, maintaining stable activity with minor variances between 54.0% to 58.0%, reflects a steadier operational output in light of rising demands in domestic sectors like automotive, a market perhaps undeterred by fertilizer procurement shifts.

ArcelorMittal Nippon Steel India witnessed declines, centered around 35.0% in April from 40.0% previously, potentially signaling tighter supply chains indirectly linked to the aforementioned developments in joint procurement of raw materials, restricting operational adaptability.

Overall, given the prevailing conditions, steel buyers are advised to secure procurement ahead of any anticipated supply constraints. Merging orders through joint acquisitions could promote cost efficiencies as collective purchasing approaches in fertilizer may indicate underlying trends worth monitoring, while readiness for rapid shifts in demand signals based on regional developments is crucial.

Actionable procurement recommendations include securing contracts with JSPL and Tata Steel to capitalize on their comparatively higher activity rates, while closely monitoring developments within the fertilizer supply domain that may affect overall steel production stability.