From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope’s Steel Market: Neutral Outlook Amid Fluctuating Plant Activity and CBAM Controversies

Recent developments in Europe illustrate a complex landscape for the steel industry, particularly surrounding the Carbon Border Adjustment Mechanism (CBAM). In the article MEPs urge Commission to ‘reassess’ CBAM for Ukraine, we see calls for the EU to reconsider CBAM’s impacts on Ukrainian steel exports, aligning with a significant drop in Ukrainian production levels due to the ongoing war. Meanwhile, the recent article The European Parliament has begun discussing a CBAM deferral for Ukraine reiterates this sentiment and reflects the unresolved status of Ukraine’s steel sector under CBAM regulations, generating uncertainty in market conditions.

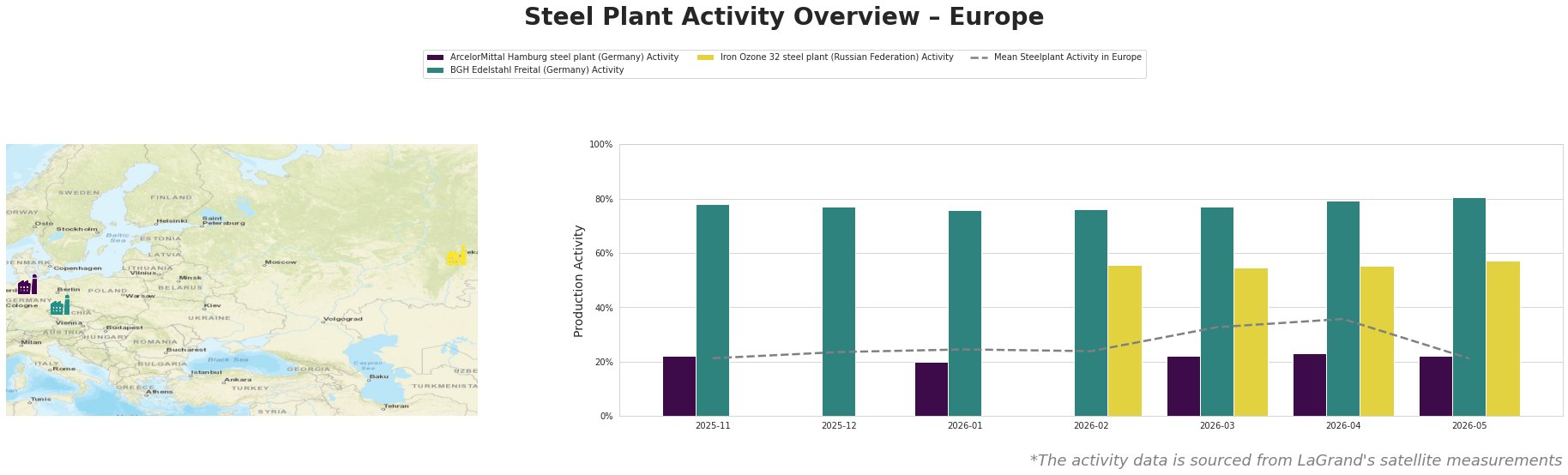

Measured Activity Overview

Activity levels across Europe show considerable variability. The mean activity dipped from a peak of 36% in April 2026 to 21% in May 2026, mirroring broader uncertainties regarding steel demand likely spurred by geopolitical events as noted in Business associations have called on the EC to adopt a special CBAM approach for Ukraine. The BGH Edelstahl Freital consistently maintained higher activity levels, peaking at 81% in May 2026, indicative of stable operations despite the market volatility.

Plant Analysis

ArcelorMittal Hamburg: The plant’s recent activity is closely tied to fluctuations in market sentiment; it recorded a low of 20% in January 2026, contrasting with a brief recovery in April. This decline coincides with rising concerns over global steel demand and regulatory adjustments outlined in the above news articles, although a direct alignment with CBAM initiatives remains unconfirmed.

BGH Edelstahl Freital: Exhibiting higher activity levels throughout the observed period, this plant reached an impressive 81% in May 2026, reflecting strong demand for stainless and tool steels. Its operation resilience may buffer it against fluctuations attributed to CBAM discussions affecting larger market players.

Iron Ozone 32: The Russian plant displayed more volatility, with activity dropping from 56% in February to stabilizing around 57% in May. This aligns with ongoing geopolitical tensions that directly affect supply chains, but it lacks specific links to the aforementioned news articles.

Evaluated Market Implications

The ongoing discussions regarding CBAM, particularly its implications for Ukraine, signal potential supply disruptions, especially if Ukrainian steel production continues to decline. Given that MEPs urge Commission to ‘reassess’ CBAM for Ukraine suggests urgent need for policy clarity, steel buyers should prepare for possible shortages or increased prices linked to Ukrainian exports.

Steel procurement professionals should consider diversifying suppliers, particularly exploring options outside affected regions, as highlighted by the activity insights of BGH Edelstahl Freital. Strategic procurement actions, such as increased stockpiling from suppliers with stable output like BGH Edelstahl, can serve as a risk mitigation strategy against anticipated market fluctuations.

In summary, buyers must remain vigilant, monitor geopolitical developments closely, and be ready to adjust procurement strategies to navigate a neutral but uncertain market landscape effectively.