From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNeutral Outlook for Ukraine’s Steel Market: Analyzing Recent Activity in Light of UK Trade Measures

Recent developments in the Ukrainian steel market are influenced by external regulatory changes in the UK concerning steel imports. Notably, the UK has published details of new protective measures concerning steel, which will affect duty-free import quotas. This regulatory environment coincides with observed changes in the operational activity of major Ukrainian steel plants.

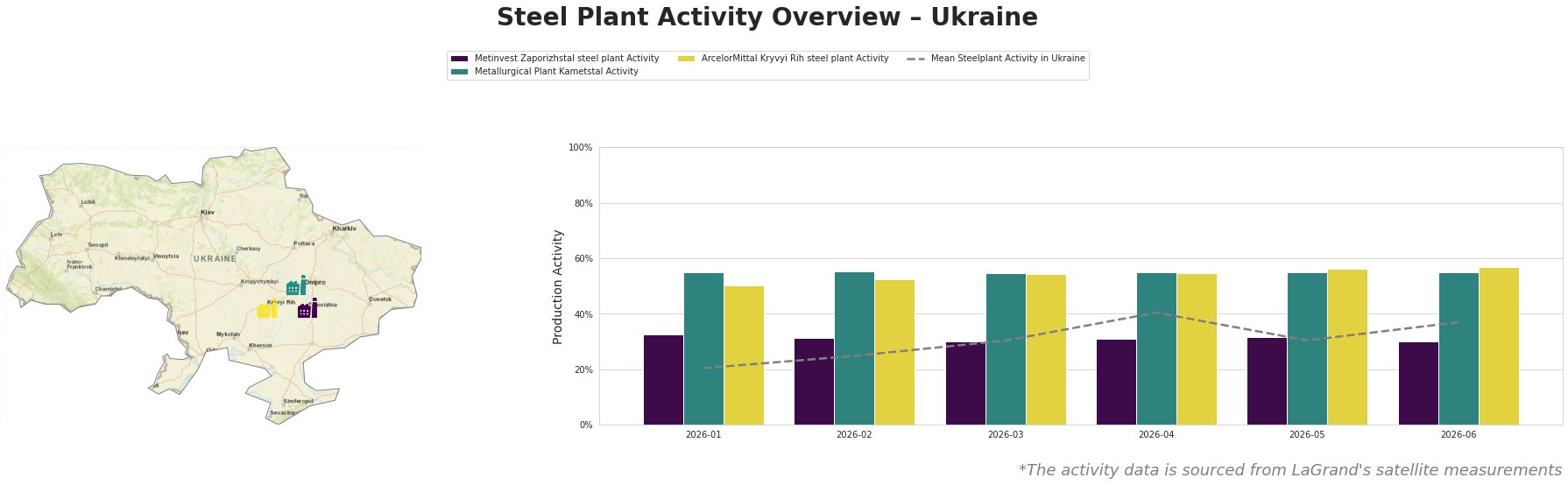

In June, satellite data showed that Metinvest Zaporizhstal, Metallurgical Plant Kametstal, and ArcelorMittal Kryvyi Rih experienced fluctuations in activity. Metinvest Zaporizhstal’s activity saw a significant drop to 30% in June from a 32% peak in May, while ArcelorMittal’s activity slightly increased to 57%, showing resilience amidst industry challenges.

The Metinvest Zaporizhstal plant operates primarily through integrated blast furnace technology, producing finished rolled goods such as hot-rolled coils and sheets. Despite its strong production capacity of 4,100 tonnes of crude steel, its activity declined in June. This drop may reflect ongoing uncertainties tied to import tariffs imposed by the UK, which will remain attractive for Ukrainian steel exports, as confirmed in the article UK confirms reduction of import quotas by 51%.

Metallurgical Plant Kametstal maintained stable performance at 55%, indicating steady production of semi-finished and finished rolled products primarily for the energy and transport sectors. It’s worth noting that some market versatility may cushion Kametstal from shocks stemming from UK tariffs, although no direct relationships between Kametstal’s sustained activity levels and the noted UK news articles were observed.

ArcelorMittal Kryvyi Rih, with its robust production capability of 8,000 tonnes of crude steel, saw activity rise to 57% in June. This growth can potentially be attributed to its diversified product lines, which include critical inputs for construction and infrastructure. The relatively higher activity level amidst UK import restrictions underscores the plant’s resilience against market disruptions, although no explicit linkage to the recent UK measures was established.

In terms of market implications, ongoing import restrictions could potentially shift supply dynamics, particularly impacting pricing strategies. Steel buyers should consider leveraging existing tariffs favorable to Ukrainian products against rising costs from other markets. Procurement strategies should prioritize securing contracts with Ukrainian facilities, especially with UK adjusts EU import quotas after agreement is reached, which emphasizes Ukraine’s preferential trading status.

Therefore, procurement professionals are advised to:

– Secure agreements with Ukrainian suppliers before potential price hikes driven by shifts in the UK market.

– Monitor plant activity levels closely to identify potential disruptions and align procurement strategies accordingly.

– Remain informed about ongoing changes in international trade policies affecting steel imports, particularly from the UK, to safeguard against unforeseen market shifts.