From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSteel Market Overview: Asia’s Steel Production Shows Signs of Recovery Amidst Ongoing Challenges

China’s steel industry is currently navigating a cautious landscape, with a reported 3.9% decrease in steel output from January to May, as detailed in the article “China reduced steel output by 3.9% y/y in January–May.” Despite this decline, a slight rebound was observed in May, aligning with seasonal peaks in consumption, highlighted in both “China’s crude steel output down 3.9 percent in January-May 2026, slight rebound in May“ and “CISA mills’ daily crude steel output up 3.8% in early June 2026, stocks also up.” This indicates that while production has slowed, demand may pick up during peak construction seasons, suggesting a complex balancing act for buyers.

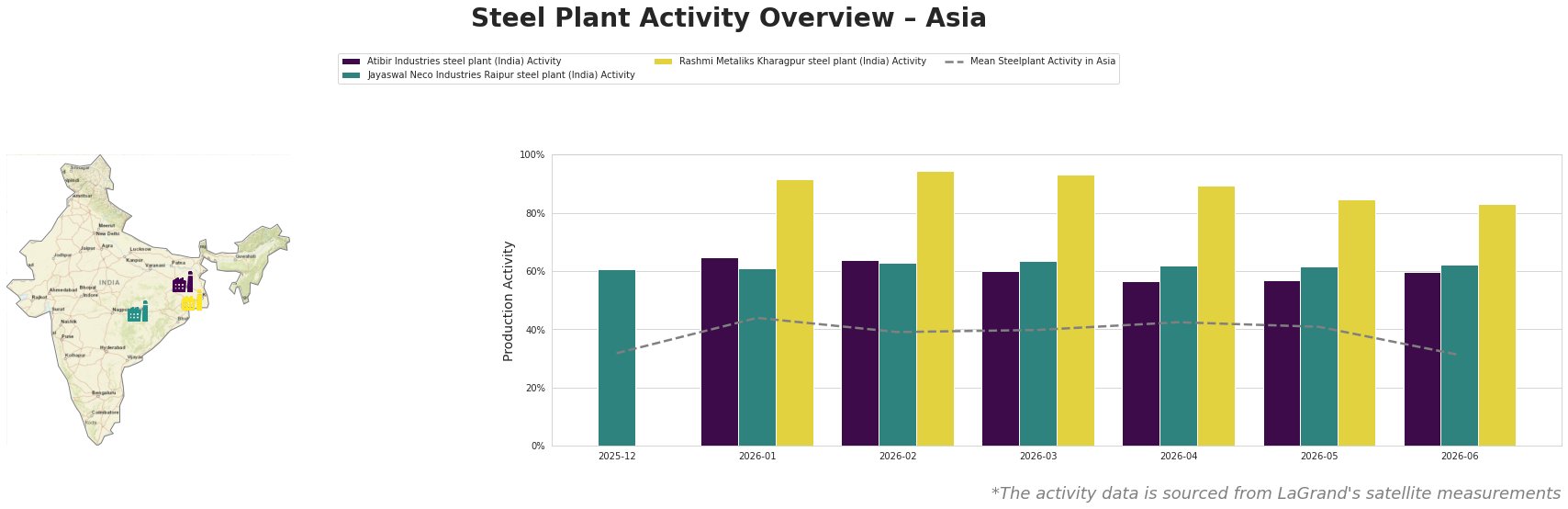

Atibir Industries’ activity peaked at 65% in January but fell to 57% in May, then rebounded slightly to 60% in June. This aligns with the anticipated seasonal fluctuations noted in “CISA mills’ daily crude steel output up 3.8% in early June 2026, stocks also up.” Jayaswal Neco Industries exhibited stable activity, fluctuating between 62% and 64%, suggesting resilience despite the broader market context. In contrast, Rashmi Metaliks experienced drops from 92% in January to 85% in May, reflecting changing demand patterns as indicated by the overall reduction in steel output.

The reduction in China’s property investments, detailed in “Investment in Chinese property fell by 16.2 per cent y/y in January–May,” pressured overall steel demand, as construction activities are a key consumer of steel. The disproportionate decline in construction activity, along with falling steel consumption in the sector, may further impact the procurement strategies for buyers, highlighting potential supply issues amid increased inventory levels in June.

Given the current neutral sentiment, steel buyers should consider procuring ahead of peak demand seasons but remain vigilant as inventory levels and property market conditions could signal further disruptions. Immediate actions should focus on the following:

- Monitor Inventory Levels: With rising stocks reported, particularly noted in “CISA mills’ daily crude steel output up 3.8% in early June 2026, stocks also up,” assess timing for procurement based on inventory cycles.

- Adjust Procurement Strategies: Based on the production fluctuations among observed plants, particularly Rashmi Metaliks, review order sizes and timelines in alignment with published activity trends and anticipated seasonal consumption peaks.

- Evaluate Plant Performance: Remain informed about individual plant performance metrics as seen with Atibir Industries and Rashmi Metaliks, ensuring that sourcing aligns with capacity and production stability during uncertain market conditions.

A close watch on plant-specific and macroeconomic indicators, especially regarding China’s real estate sector, will be essential for guiding strategic procurement decisions in the coming months.