From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineChina’s Steel Market Insights: Production Decline with Signs of Rebound in Early June 2026

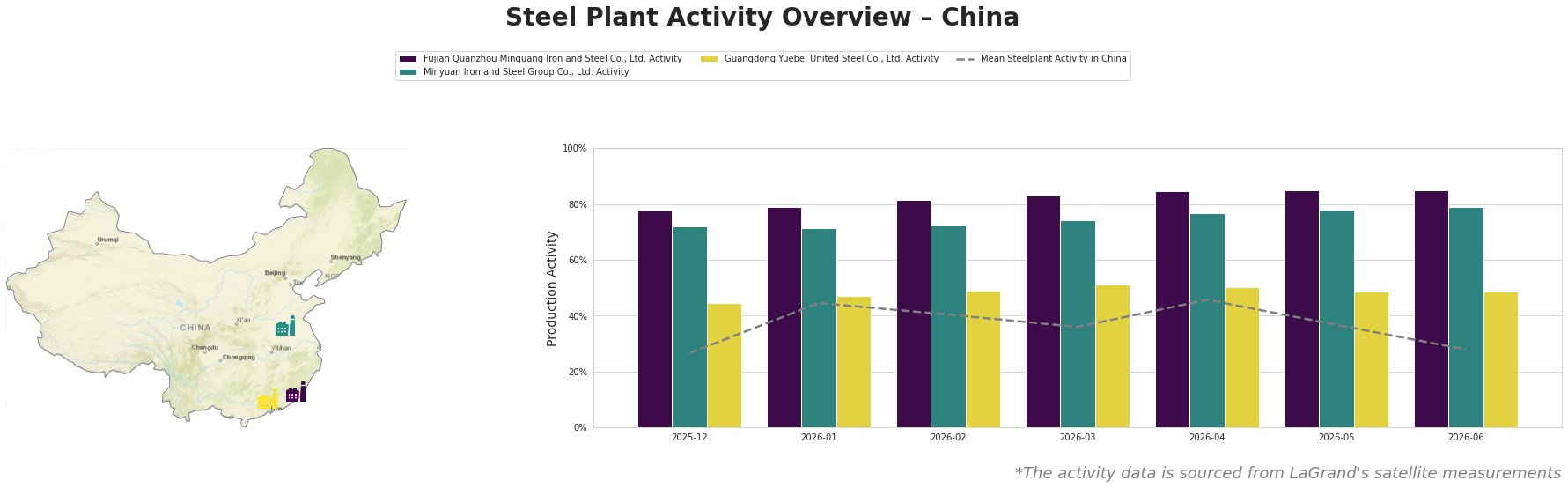

China’s steel industry faces challenges, marked by a 3.9% year-on-year decline in steel output from January to May, as detailed in “China reduced steel output by 3.9% y/y in January–May“ and “China’s crude steel output down 3.9 percent in January-May 2026, slight rebound in May.” Despite the overall downturn, May saw an uptick in crude steel output, correlating with peak seasonal demand, while subsequent satellite observations indicate mixed plant activity levels.

Fujian Quanzhou Minguang Iron and Steel Co., Ltd. maintained robust activity levels, hitting 85% in late May despite a 3.8% increase in daily crude steel output reported by CISA, indicating a consistent output approach amid market fluctuations. Contrarily, Guangdong Yuebei United Steel Co., Ltd. experienced lower activities at 49% in May, with no clear connection to specific news articles indicating significant changes in this region.

Minyuan Iron and Steel Group Co., Ltd. reflects sluggish demand trends evidenced by a 4.3% decline to late May activity. This downturn correlates with overall market weakness, notably impacting the building sector and housing prices, as noted in “NBS: New house prices in first-tier cities of China up 0.2% in May 2026 from April.”

As steel prices showed slight decreases, with an average rebar price down by 0.2% from early June (according to the MOC), a surge in crude steel output of 3.8% early June might indicate a temporary recovery. However, rising steel inventories—up 6.6% compared to late May—signal weak demand, further supported by the rainy season affecting construction activity.

Supply disruptions may arise from continued weak demand in regions served by Guangdong Yuebei, while Fujian’s stable production mitigates immediate threats to availability in that sector. Steel buyers should consider prioritizing procurement from Fujian’s Minguang plant, given its current capacity and sustained activity levels, ensuring supply resilience. Analysts should closely monitor ongoing pricing trends, as rising costs in coal (e.g., coking coal up 3.6%) might affect future steel pricing strategies.

Thus, while production and market sentiment remain neutral, the potential for regional procurement strategies to pivot based on real-time plant activity is critical in navigating current market dynamics.