From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineGermany’s Steel Industry Faces Downward Pressure Amid Rising Trade Tensions

Germany’s steel market sentiment has turned negative due to recent external pressures, particularly from potential new tariffs as highlighted in “Donald Trump: Neue Zolldrohung gegen EU im Fokus“ and “Neue US-Zölle: Bis zu 30 Milliarden Euro – so hoch wäre der Schaden für die deutsche Autoindustrie.” Analysts warn that these tariffs may significantly increase production costs for automotive-related steel products, which could directly impact demand across the sector.

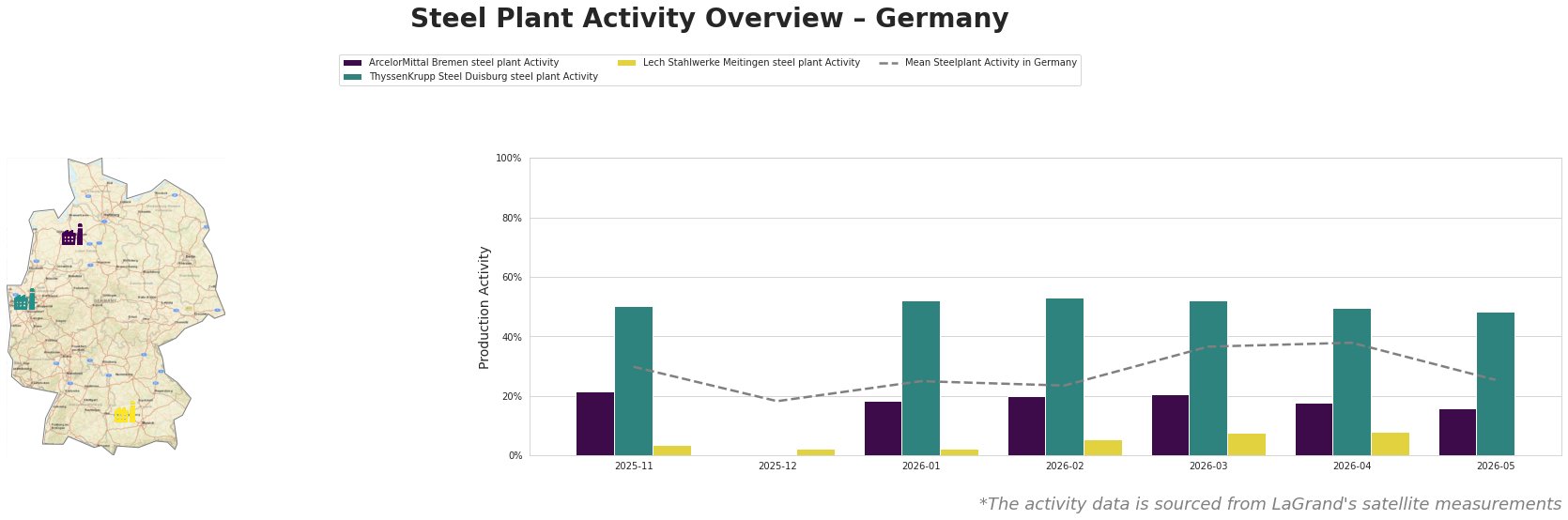

The activity levels across Germany’s steel plants have seen marked declines, particularly in May 2026. The mean activity dropped to 25% from 38% in April, showing a worrying downward trend. The ArcelorMittal Bremen plant decreased from 18% in April to 16% in May, while ThyssenKrupp in Duisburg experienced a reduction from 50% to 48% in the same period. The Lech Stahlwerke Meitingen plant has recorded persistently low activity, which correlates with heightened uncertainties regarding automotive steel demand due to impending U.S. tariffs as mentioned in the articles.

The ArcelorMittal Bremen steel plant, with a crude steel production capacity of 3,800 tonnes, has seen its activity decline by 2% to 16% in May from April levels. This plant produces finished rolled products primarily for the automotive sector, which may be adversely affected by the new U.S. tariffs discussed in “Neue US-Zölle: Bis zu 30 Milliarden Euro – so hoch wäre der Schaden für die deutsche Autoindustrie.” This plant’s reduced activity may indicate a pulled-back production in anticipation of declining orders from the automotive industry.

ThyssenKrupp Steel Duisburg, capable of producing 13,000 tonnes of crude steel, observed a slight decrease to 48% activity in May. This plant provides a range of products including hot strip and coated products crucial for various sectors, including automotive. The ongoing trade tensions and fears of recession—signaled in both “Neue US-Zölle: Bis zu 30 Milliarden Euro – so hoch wäre der Schaden für die deutsche Autoindustrie” and “Donald Trump: Neue Zolldrohung gegen EU im Fokus”—forewarn of possible swings in order demands that could further hinder production.

Lech Stahlwerke Meitingen, a smaller electric arc furnace plant, registered very low activity levels, maintaining just 8% in April and dropping to a null percentage in May, indicating stagnant operations possibly linked to reduced demand from its automotive and construction end-users amidst the prevailing economic uncertainties.

Market implications drawn from these trends indicate potential supply disruptions, particularly for automotive-grade steel as plants like ArcelorMittal Bremen brace for reduced orders due to the projected increase in tariffs. For procurement professionals, immediate recommendations include:

-

Reassess Long-term Contracts: Engage suppliers to review long-term contracts with flexibility in delivery volumes and pricing structures to mitigate future supply volatility.

-

Diversify Supply Sources: Consider alternative steel suppliers in less affected regions to buffer against localized production losses.

-

Monitor Political Developments: Keep a close eye on trade negotiations and tariff announcements impacting the EU and Germany, allowing timely adjustments to procurement strategies in response to emerging risks.

Targeted scrutiny of these specific plants and their roles in the broader supply chain will be essential for navigating the current downturn while aligning with actionable procurement strategies.