From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Outlook for the European Steel Market Amid Regulatory Developments and Plant Activity

Recent developments in the European steel market have been fueled by significant regulatory discussions and varying activity levels across key plants. The articles ETS: delayed responses, a cautious approach and key demand and ETS: Delayed response, cautious approach, and basic requirements detail Luxembourg’s reservations over the European Emissions Trading System (ETS) reforms aimed at maintaining industrial competitiveness, which may drive steel demand. This cautious yet supportive stance from Luxembourg harmonizes with observed activity levels at selected steel plants.

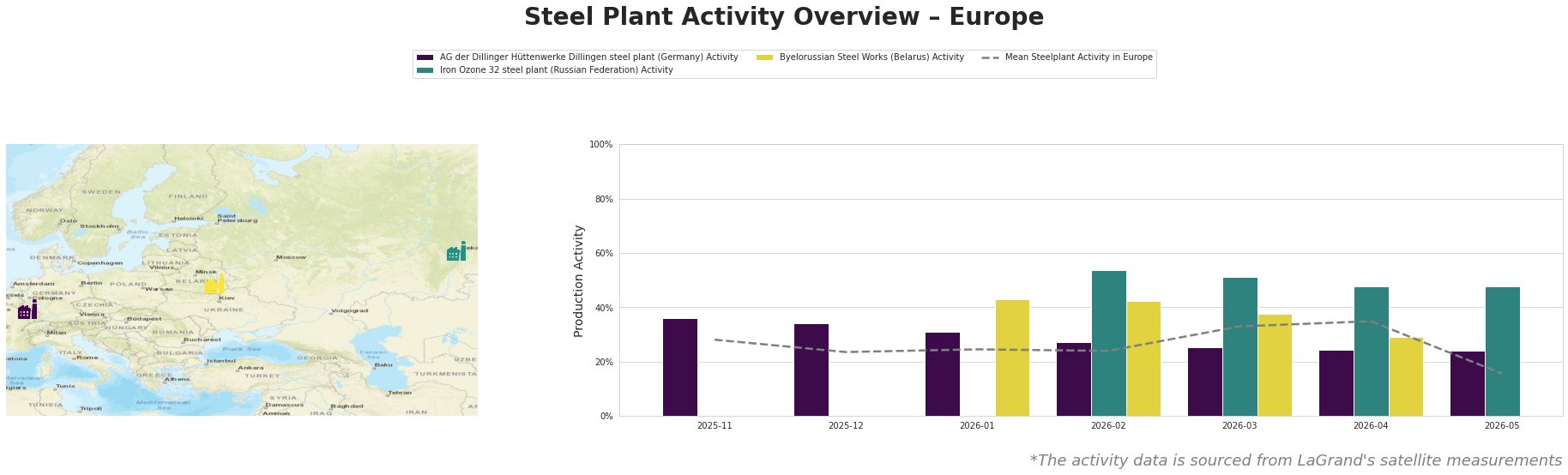

Measured Activity Overview

AG der Dillinger Hüttenwerke in Germany shows variability with a peak of 36% in November 2025, followed by relative stability before a notable decline to 24% in May 2026. This fluctuation suggests a direct influence from ongoing discussions regarding the ETS regarding competitiveness, as emphasized in the articles.

The Iron Ozone 32 plant demonstrated significant activity increases with peaks of 54% in January 2026, later stabilizing at 48% by April 2026, likely motivated by responsive market demands amid regulatory changes. This is further evidenced by Luxembourg’s efforts to address energy costs and industrial support as outlined in the previous articles.

Byelorussian Steel Works reflected a related decline, falling to 29% activity by late April 2026, which may indicate challenges linked to its operational environment and international competitiveness amidst the backdrop of the ETS discussion.

Evaluated Market Implications

The variability in plant activity, particularly concerning AG der Dillinger Hüttenwerke and Iron Ozone 32, suggests potential supply disruptions in steel sourcing, particularly if regulatory changes create prolonged production uncertainties, especially given the backdrop of Luxembourg’s cautious approach outlined in ETS: delayed responses, a cautious approach and key demand. Steel buyers should closely monitor these developments, as notable reductions across the mean activity could signify constrained supply chains, particularly in Germany and Russia.

To mitigate potential disruptions, procurement professionals are advised to consider preemptive contracts or increased inventory for semi-finished and finished products from the active plants, particularly those with higher recent activity levels like Iron Ozone 32, while remaining vigilant to monitor shifts in regulatory context as Luxembourg finalizes its ETS insights. Specifically, focusing on maintaining supplier relationships aligned with sustainable practices could further enhance market positioning in the evolving European landscape.