From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Outlook for Iran’s Steel Market Amid Geopolitical Tensions

Recent developments in Iran’s steel sector reflect a continuous positive market sentiment, bolstered by strategic geopolitical factors and evolving industrial activity. The Iran’s ship seizures not a violation: White House and Iran fires on container ships in Hormuz: Update articles elucidate escalating maritime tensions, yet the ongoing US ceasefire extension presents a stabilizing force that may facilitate operational continuity in the steel industry. This reflects in recent satellite-observed activity across several key steel plants, showcasing varying activity levels linked more to internal dynamics rather than international maritime disruptions.

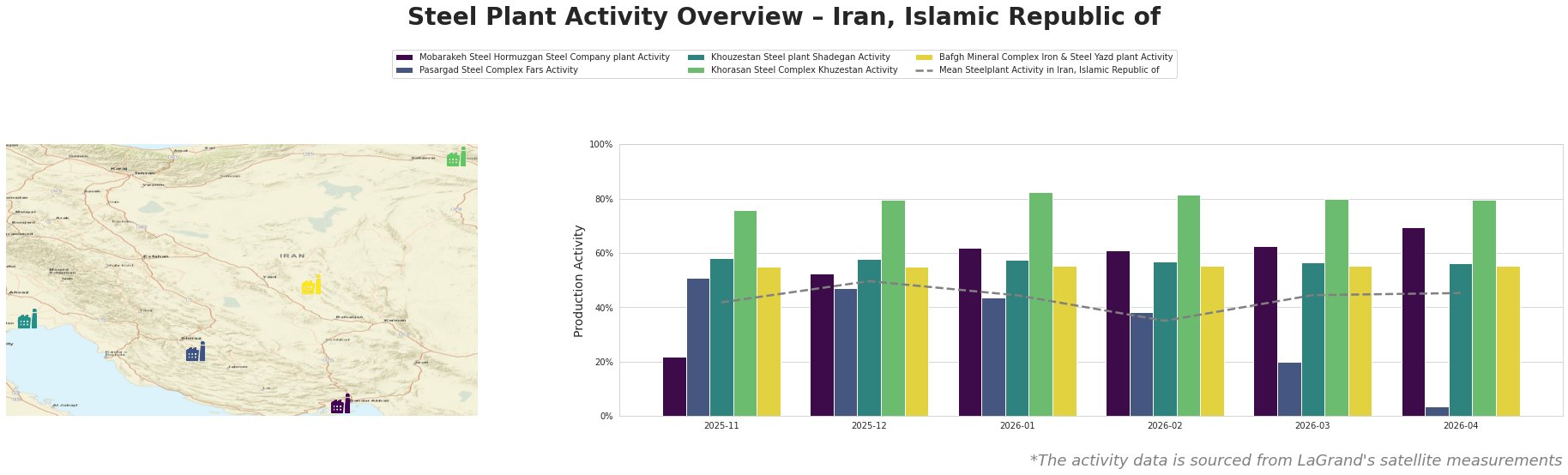

Mobarakeh Steel, pivotal for Iran’s steel production, has shown significant recovery, climbing to 70.0% activity in April from a prior low of 22.0% in November, likely indicating a shift towards proactive production strategies amid geopolitical concerns. The Stocks Supported by Iran Ceasefire Extension and Strong Earnings news suggests that the global market confidence may be influencing production levels positively.

Conversely, Pasargad Steel Complex experienced a drastic dip to 4.0% in April from 51.0% in November 2025, indicating severe disruptions which cannot be directly tied to the recent maritime incidents or ceasefire discussions. This stark decline presents a red flag for procurement professionals sourcing from this plant.

Khouzestan and Khorasan complexes maintained relative stability around 56.0% to 80.0% activity, with Khorasan peaking at 82.0%, suggesting consistent output and resilience against external pressures. This stability could be advantageous for buyers seeking reliable supply channels, especially amidst fluctuating activities in other plants.

Given the increasing geopolitical tensions surrounding maritime routes near Iran, it is prudent for steel buyers to consider stockpiling and diversifying their sourcing strategies, particularly favoring plants like Mobarakeh and Khouzestan where production is neither declining significantly nor tied to immediate risk factors from international incidents. The potential procurement approach should emphasize reliability in these regions while remaining aware of the volatility indicated by Pasargad’s activity levels.

In summary, leveraging information from both geopolitical developments and observed plant performance equips steel buyers with actionable insights to navigate the rapidly evolving landscape of Iran’s steel market effectively.