From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNegative Outlook for Iran’s Steel Market Amidst Crisis, Tensions, and Activity Declines

Iran’s steel market faces significant challenges as political tensions and operational disruptions undermine production capacities. Recent reports such as “Trump’s shift in tone fails to revive Hormuz traffic“ and “Iran’s ‘Tehran toll’ booth forces some tankers to pay millions to leave Strait of Hormuz“ indicate a critical decrease in maritime activity, directly impacting steel supply levels. Satellite data corroborates this decline, showcasing an unsettling downturn in plant operations.

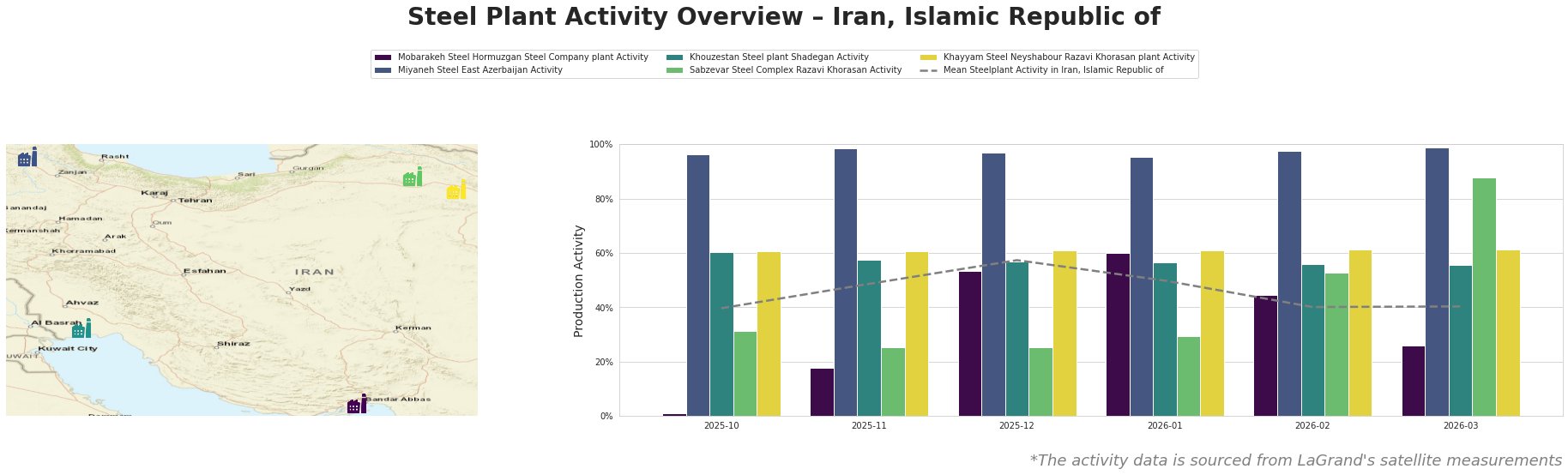

The Mobarakeh Steel Hormuzgan facility, a key player in Iran’s production landscape with a crude steel capacity of 1,500, experienced a striking drop from 60.0% in January to just 26.0% by March 2026, aligning with disruptions highlighted in “Iran says Hormuz strait only closed to ‘enemies’”. The diminished maritime traffic has likely constrained essential raw material flows to the plant, manifesting in its operational capacity.

Conversely, the Miyaneh Steel plant has maintained relatively high activity levels, peaking at 99.0% in March. This performance stands out and suggests that, despite regional tensions, some areas could still be securing necessary resources. However, without external factors mitigating the overall negative trend, the sustainability of this operation remains concerning.

For Khouzestan Steel, activity levels remained stagnant around the 56% mark, indicating a potential plateau likely due to service delays and supply chain disruptions caused by adjacent geopolitical developments.

The Sabzevar Steel Complex notably recorded increased activity in March at 88.0%, suggesting adaptability to existing challenges and a potential for enhanced procurement measures from local markets.

In light of these trends, potential supply disruptions are clearly linked to the decreasing activity levels, particularly at Mobarakeh Steel. Steel buyers should voraciously assess supply sources and consider diversifying procurement strategies to mitigate impending shortages. Specific recommendations include:

- Negotiate with local suppliers to secure raw materials, especially focusing on plants with stabilizing or increasing activity levels, such as Miyaneh and Sabzevar.

- Monitor developments surrounding the Strait of Hormuz, as maritime traffic and geopolitics deeply influence steel logistics.

- Prepare for increased pricing pressures, particularly if the current instability continues, potentially driving supply shortages in steel offerings.

In summary, Iran’s steel market is facing substantial operational challenges amidst rising geopolitical tensions and strained supply chains.