From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNegative Sentiment Prevails in Asia’s Steel Market Amid Geopolitical Turmoil

Recent developments in Asia’s steel market indicate a negative sentiment driven by geopolitical tensions and significant supply disruptions. Notably, the articles titled “Urea derivatives offered substantially higher: Update” and “Southeast Asia faces methanol supply crunch: Update” highlight how rising energy costs and diminished methanol imports are adversely impacting production capabilities. Satellite observations reveal a critical decline in activity across major steel plants, correlating with these issues, though direct linkages to specific plants from these articles are limited.

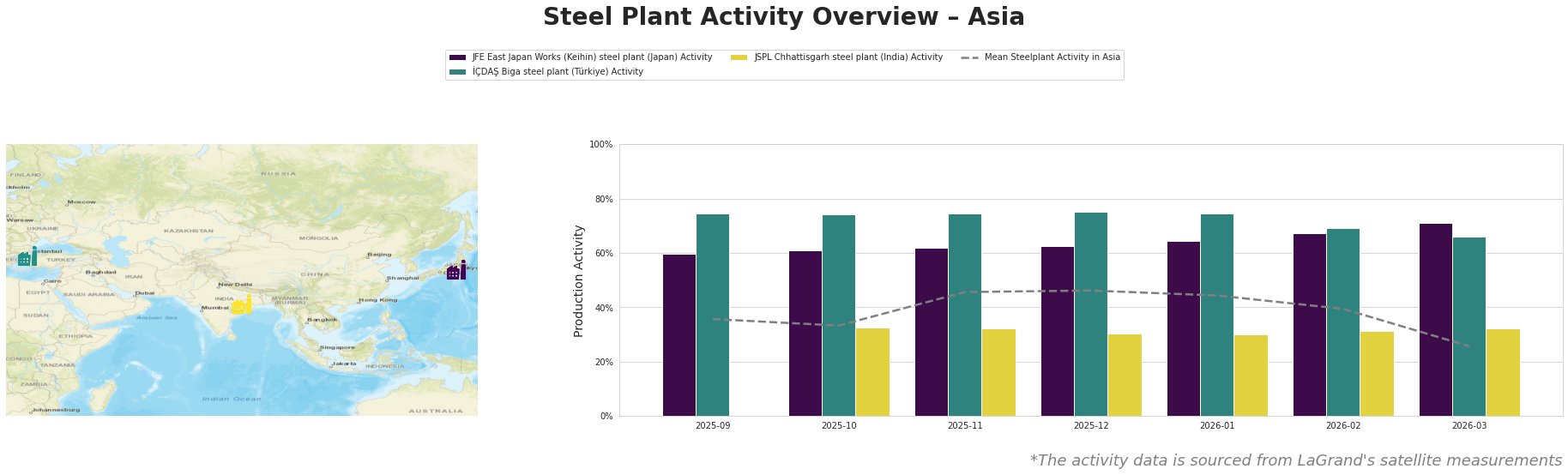

The mean steel plant activity in Asia observed a substantial decline to 26% by March 2026, falling from a previous high of 46% in November 2025. The JFE East Japan Works (Keihin) maintained a relative peak activity of 71% as late as March 2026, which will likely be impacted by the ongoing issues outlined in “Japan’s Mitsubishi Chemical slows ethylene production” as naphtha supply concerns affect broader industrial output and potential steel feedstocks. Meanwhile, İÇDAŞ Biga saw a drop to 66%, stable but worrying in light of the regional pressures from low methanol supply impacting construction steel demand.

JSPL Chhattisgarh’s activity remained the lowest at 32%, which, while stable compared to the previous month, illustrates ongoing challenges. The plant’s direct links to methanol supply shortages are less defined, indicating external pressures may have stifled production choices.

Given the rising prices for key inputs highlighted in “Urea derivatives offered substantially higher: Update”, procurement teams should closely monitor raw materials to strategize purchases—specifically focusing on regions likely to see volatility due to geopolitical factors. The expected potential for decreased supply from disrupted plants necessitates immediate action to secure inventory levels, particularly for steel producers relying on materials from Southeast Asia.

Steel procurement professionals are advised to:

– Prioritize contracts and orders for March and April 2026, anticipating higher prices.

– Assess alternative supply routes outside of impacted regions to mitigate risk.

– Maintain flexibility in production schedules to adapt to the evolving supply landscape, especially in light of cited disruptions.