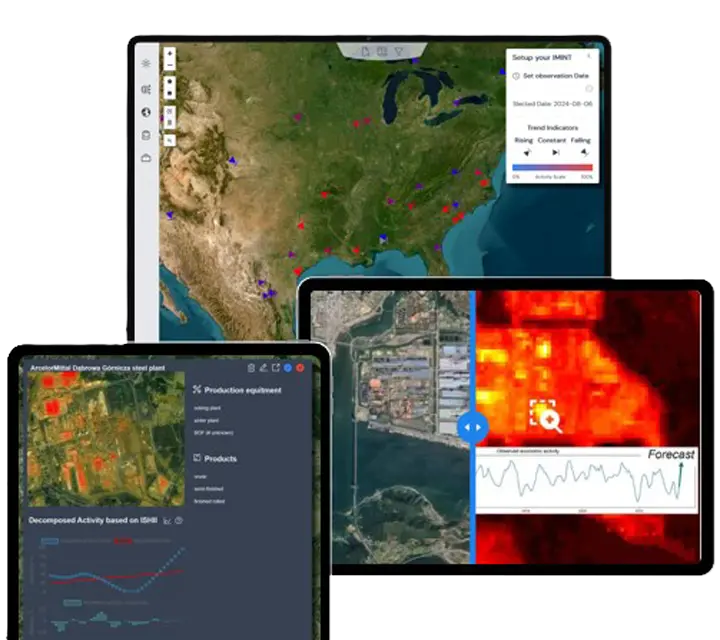

Satellite-Based Energy Monitoring

Gain valuable insights for your business and manage your energy networks and production more efficiently and sustainably.

District Heating Networks

Regular reports to safeguard security of supply to your customers when it counts most. Detect heat loss, target maintenance, reduce costs, and save energy.

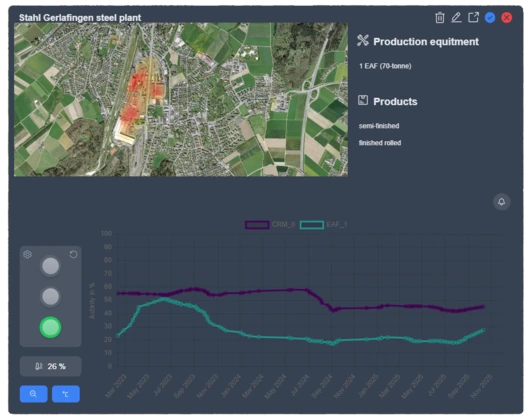

Steel Production

Web-based business intelligence to lower your cost of procurement, reduce your financial risks and gain geopolitical insights.

Future Products

Expand your energy and infrastructure monitoring capabilities from orbit. Detecting solar panel availability, rooftop installations, and defect cell locations.

From Orbit to Insight

We translate thermal radiation signals from space into actionable management summaries, combining multi-source data fusion and AI-powered anomaly detection.

Trusted by Industry Leaders

"As LaGrand's lead customer, we helped refine the novel technology into a powerful procurement tool for insights on purchasing decisions."

"Winning the RUAG Innovation Award marked LaGrand's very first milestone, proof that satellite-based industry intelligence can create impact."

Zehnder Group

Custom steel procurement intelligence reducing price volatility risks.

RUAG Award

LaGrand awarded the RUAG Innovation Prize validating satellite defect detection.

Patented Technology

Protected by international patent WO2026037483 for Cloud Reconstruction in remote sensing.