From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineSpain’s Steel Market Faces Declining Activity Amidst Uncertain Protective Measures

Spain’s steel industry currently faces a negative sentiment driven by decreasing activity levels and doubts regarding the effectiveness of EU protections. Reports such as “EU protective measures against steel imports may be ineffective – ArcelorMittal Spain“ and “ArcelorMittal Spain head questions whether higher EU steel tariffs will be enough, Gijón blast furnace restarted“ highlight recent challenges, particularly the rise in steel imports and the impact of high electricity costs. Although the resumption of operations at ArcelorMittal’s Blast Furnace B in Gijón, as noted in “ArcelorMittal resumes production at blast furnace B in Gijón,” may offer temporary relief, it coincides with a broader downward trend in activity levels.

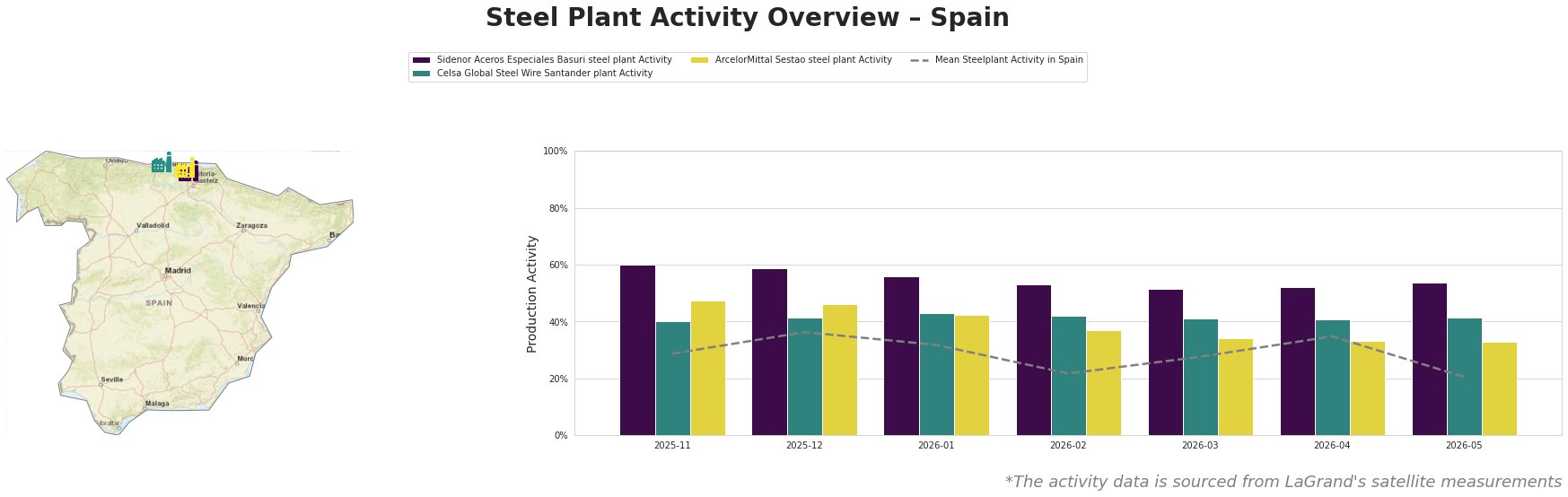

The mean activity across Spain’s steel plants recently fluctuated with a notable decline to 21% in May 2026, underscoring significant challenges. Sidenor Aceros Especiales Basuri experienced stable activity around 60% to 54%, while ArcelorMittal Sestao’s production dropped significantly from 47% in November to 33% in May. This aligns with concerns from Philippe Meyran about industry conditions in the “EU protective measures against steel imports may be ineffective – ArcelorMittal Spain” article, highlighting a slow industry downturn amid rising imports and high costs for switch to electric arc furnaces.

For Celsa Global, activity remained relatively steady, oscillating between 40% and 43%. However, declines in overall production hint at systemic weaknesses rather than isolated struggles.

The strategic reopening of Blast Furnace B in Gijón is unlikely to offset broader market declines, as Meyran emphasizes a lack of regulatory stability and escalating costs, casting doubt on the forthcoming tariff decisions’ impact on improving conditions (as stated in “ArcelorMittal Spain head questions whether higher EU steel tariffs will be enough, Gijón blast furnace restarted”).

Purchasing professionals should be vigilant about the following potential supply interruptions:

– ArcelorMittal Sestao: Recent production drops may continue as tariffs loom, leading to limited availability.

– Investigate Sidenor associations as a potential alternative supplier, given its relatively steady performance.

To adapt to the shifting market landscape, buyers are advised to:

– Secure additional sourcing from Sidenor: Given its consistent output levels in the face of broader declines.

– Monitor developments surrounding EU tariffs closely: Procurement strategies may need to adapt based on shifts in import duties affecting pricing and availability.

This comprehensive approach can aid in mitigating risks associated with an increasingly uncertain market.