From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Upsurge in European Steel Market: Key Operational Resumptions at ArcelorMittal Boosts Activity Levels

ArcelorMittal’s plans to reignite operations, as detailed in “ArcelorMittal to resume operations in Gijon next week“ and “ArcelorMittal resumes production at blast furnace B in Gijón,” signal a restoration of activity levels across Europe’s steel industry. This resurgence coincides with rising trade volumes and is corroborated by satellite data indicating increasing operations at key plants, highlighting a positive market sentiment driven by renewed demand.

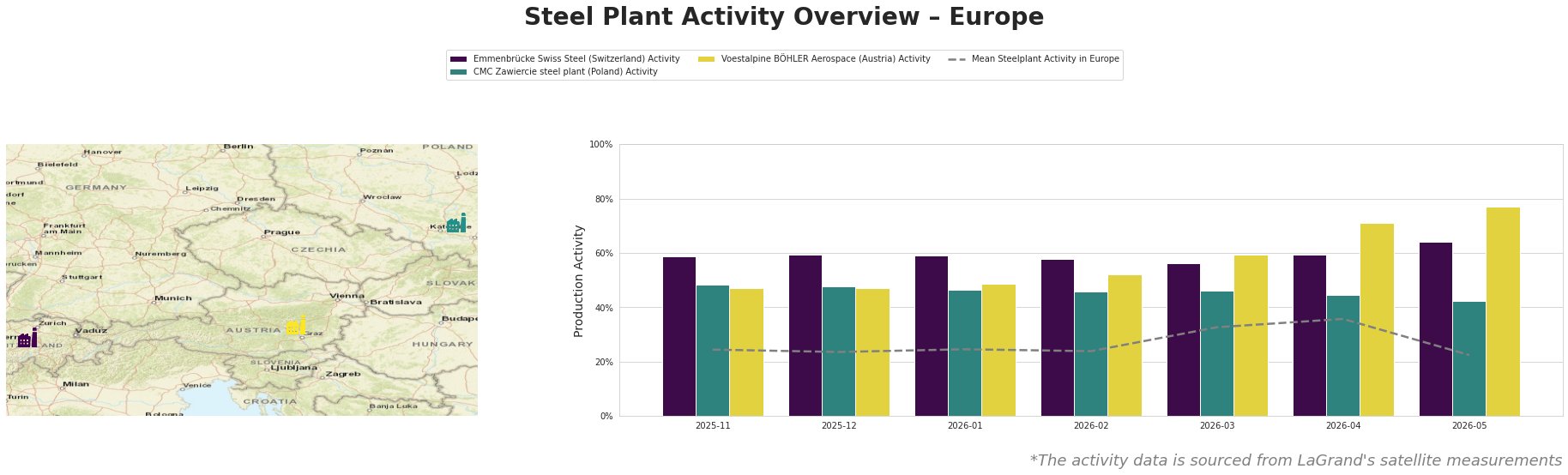

In observing the activity levels across various plants, Emmenbrücke Swiss Steel maintained a strong performance with a peak activity of 64% in May 2026. This is significant, especially given the overall average European steel activity is trending downward at 22% for the same period. The increase is notable against “Review of global steel production and production capacities conducted by MEPs,” which emphasizes ongoing modernization efforts beneficial to productivity.

CMC Zawiercie, with a crude steel capacity of 1.7 million tons, showed a decrease to 42.0% activity by May 2026. This dip aligns with the broader context of a temporary decline in steel demand stemming from global supply pressures, yet the company continues to serve diverse industries including automotive and construction, signaling a potential rebound as market stability improves.

Voestalpine BÖHLER Aerospace reported the highest activity level at 77.0% as of May 2026, benefiting from consistent demand in specialized aerospace sectors. This peak further reinforces optimism presented in “ArcelorMittal Spain head questions whether higher EU steel tariffs will be enough…” indicating that heightened tariffs may bolster domestic production in adjacent sectors.

Strategically, the potential for supply disruptions is limited due to the operational resumptions, especially at ArcelorMittal’s facilities in Gijón and Fos-sur-Mer, as noted in the articles. Given this context, steel buyers are advised to focus on contracts covering this increased capacity and demand. Additionally, considering rising production capabilities, procurement should be prioritized during this uptick in activity, particularly from those facilities benefiting from modernization efforts that include electric arc furnace technology.

The operational resumes are further bolstered by consistent electrical steel production initiatives, such as those at new electrical steel lines in northern France, enhancing the supply chain robustness amidst potential fluctuations in international trade dynamics. Consequently, steel buyers should remain vigilant about procurement strategies that align with both domestic capacity and the evolving trade landscape.