From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Outlook for Europe’s Steel Market Driven by Increased Activity and Higher Raw Material Prices

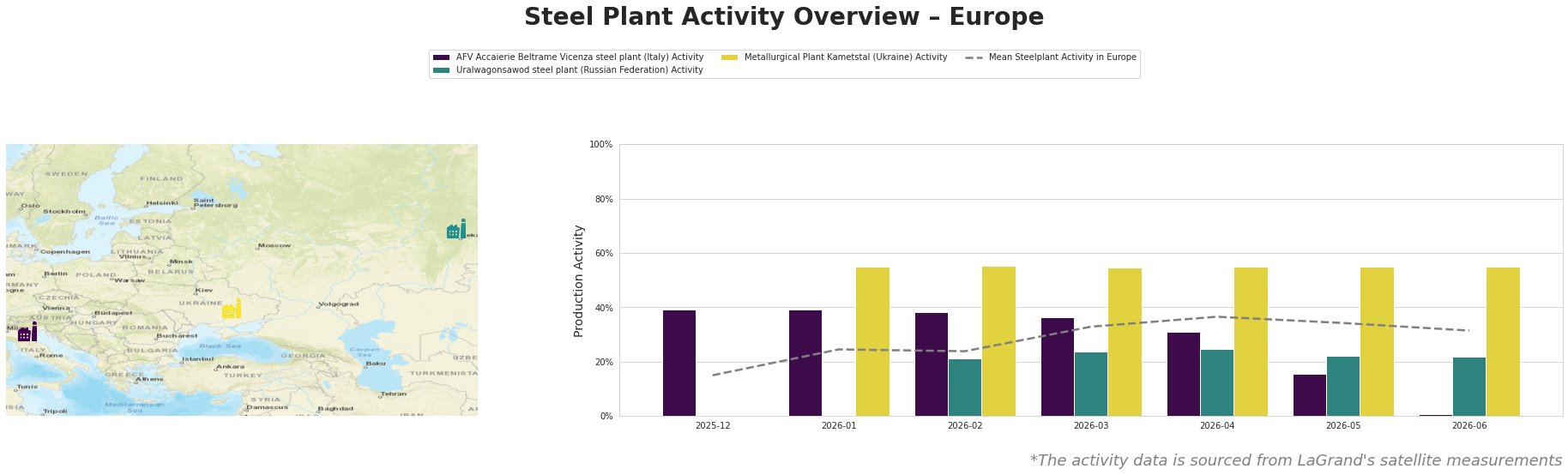

Steel producers across Europe are experiencing a positive trend in activity levels, coinciding with rising forecasts for iron ore and coking coal prices. Recent developments outlined in Fitch raises its iron ore price forecast for 2026 to $100 per tonne demonstrate the market’s resilience despite global economic uncertainties, contributing to an uptick in production levels among key steel plants. The activity at the Metallurgical Plant Kametstal in Ukraine, which has maintained steady output, is particularly noteworthy as it aligns with stable demand from steelmakers indicated in Fitch’s analysis.

The AFV Accaierie Beltrame Vicenza steel plant (Italy) has seen a dramatic decline in activity, plunging from 39% in December 2025 to just 1% by June 2026. This 38 percentage point drop does not seem to connect directly to any specific news, indicating possible internal operational challenges. In contrast, the Metallurgical Plant Kametstal remains stable at 55%, aligning with rising global demands as outlined in Fitch’s report.

Meanwhile, Uralwagonsawod in the Russian Federation shows modest fluctuations, where recent activity increased to 22% in May, contrasting with the low activity observed in Vicenza but still below market expectations. The recent coking coal trends noted in Australian coking coal exports climb up in May 2026 on strong Asian offtake signify a robust demand that could support Uralwagonsawod’s future performance as well.

Given the upward trends in raw material prices and the stability of high-intermediate production levels at Kametstal, steel procurement professionals should consider locking in supply contracts sooner rather than later to hedge against anticipated price increases and potential supply disruptions due to rising logistical and geopolitical strains. Specifically, while the downturn at the Vicenza plant presents a current challenge, its eventual recovery could align positively with the broader market trends noted in Fitch’s projections.