From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNeutral Steel Market Outlook for Europe: Observations from Recent Plant Activities

Recent satellite data indicates a fluctuating landscape in Europe’s steel industry. Notably, the sentiment remains Neutral amid pressing regulatory changes and market pressures. Key articles such as “99 Prozent Elektroquote für deutsche Unternehmensflotten” and “German government approves building modernisation law” highlight the ongoing legislative shifts that intertwine with operational dynamics. Specifically, increased activity in aforementioned steel plants doesn’t show a direct link to the legislative changes, which adds complexity to the current market scenario.

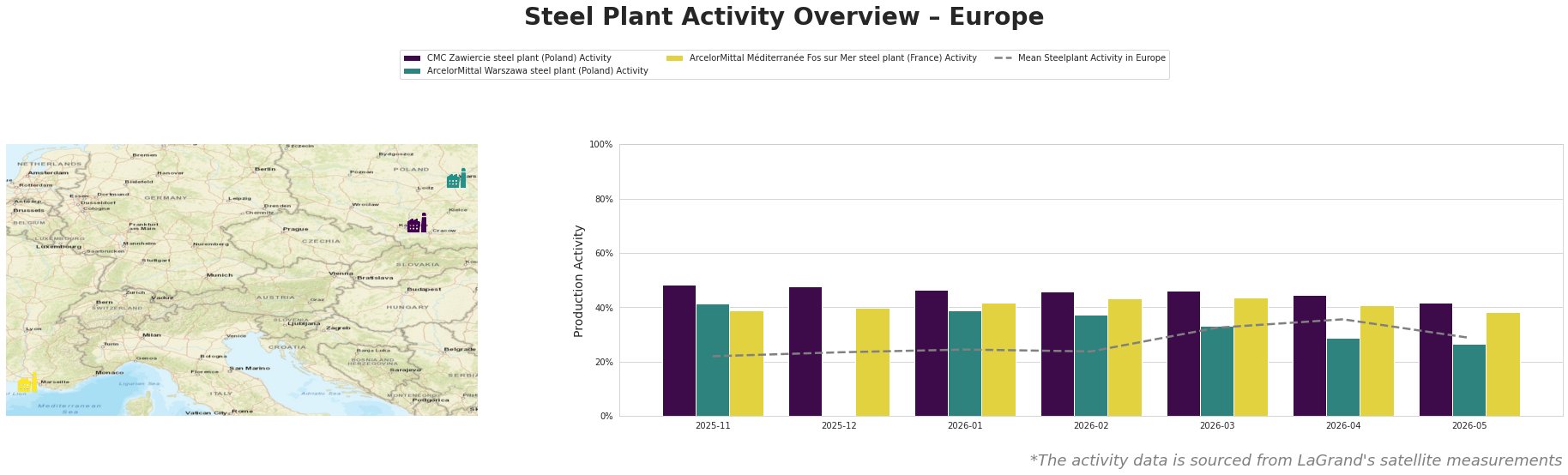

The CMC Zawiercie steel plant in Poland exhibited notable activity, peaking at 48.0% from November to December 2025, but has seen a gradual decline to 42.0% by May 2026. This trend, while substantial, appears disconnected from legislative changes posed by “99 Prozent Elektroquote für deutsche Unternehmensflotten”, which primarily affects the automotive sector.

ArcelorMittal Warszawa has also faced downturns, dropping from 41.0% in November to just 26.0% in May. These reductions align with broader climate discussions implied in “Energiewende: Klimaziele sind nicht das Problem,” suggesting that market pressures may stem from rising energy costs rather than operational inefficiencies in the plant itself.

Conversely, ArcelorMittal Méditerranée shows resilience with minor activity fluctuations within a stable range of 39.0% to 43.0% across the same timeframe. While some stability is expressed, “Klimaziele verfehlt – na und?” invites scrutiny on whether such operational stability may affect future sustainability initiatives.

Potential procurement actions for buyers include focusing on Polish suppliers like CMC Zawiercie, where lower fluctuations are observed versus their counterparts, and monitoring policy impacts particularly linked to the newly approved building modernisation law, as outlined in “German government approves building modernisation law.” Immediate supply chain disruptions are possible as the industry adjusts to evolving energy transition laws, underscoring the necessity for adaptable procurement strategies.

In summary, while the overall steel market illustrates stability in activity levels, ongoing political developments could significantly alter supply dynamics and pricing mechanisms in the short term. Buyers should remain vigilant and adjust their strategies accordingly.