From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNegative Trends in Europe’s Steel Market: Urgent Implications for Buyers

Recent developments in Europe, particularly around UK-India trade relations and steel import quotas, present a challenging outlook for the steel sector. Articles such as “Tariff quota negotiations are politicizing European steel imports“ and “British businesses are calling on the government to ease protective measures on steel“ highlight escalating tensions that have led to significant drops in operational activity, as observed through satellite data.

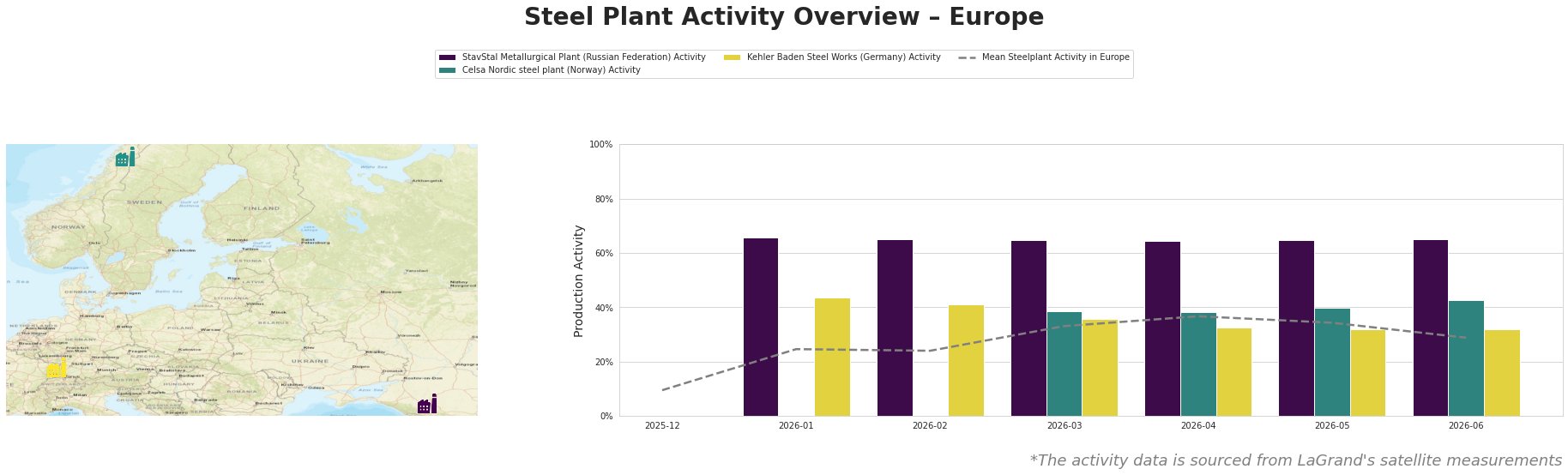

In response to impending import restrictions effective July 1, 2026, plants across Europe are experiencing a downturn. For instance, the average steel plant activity decreased from 34% in May to 29% in June, aligning with warnings from the British Chambers of Commerce regarding the financial impacts of tariff increases and quota reductions. Directly connected, the StavStal Metallurgical Plant in Russia exhibited static activity levels of 65% throughout the observed months, indicating it may not yet be reflecting the broader market downturn, while Kehler Baden Steel Works in Germany reported a consistent 32%, possibly struggling to meet domestic demand as quotas tighten.

At the Celsa Nordic steel plant in Norway, activity increased slightly to 43% in June from 40% in May, signalling minor resilience amid heightened political uncertainties mentioned in the pending negotiations about tariff quotas. Nevertheless, the BCC’s concerns, referenced in “BCC warns UK steel import restrictions could create ‘cliff-edge’ for manufacturers,” emphasize that these shifts may still be insufficient given the restrictions’ scale.

Current dynamics suggest potential supply disruptions, especially for plants in the UK. Steel buyers should proactively consider alternative sourcing strategies from regions less affected by quota reductions and tariffs, leveraging the relatively stable StavStal plant, which maintains its operational capacity. Additionally, timely engagement with suppliers regarding inventory strategies ahead of July’s tariffs is crucial to mitigate financial impacts, particularly for SMEs in construction and manufacturing that might face increased costs.

Given the interdependencies outlined, steel procurement strategies must adapt swiftly to avoid operational disruptions, following specific recommendations from industry leaders to advocate for adjustments in upcoming policy measures.