From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNegative Sentiment in Ukraine’s Steel Market: Supply Challenges Loom Ahead

Ukraine’s steel market faces significant challenges as highlighted by the UK confirms reduction of import quotas by 51% and Tariff quota negotiations are politicizing European steel imports. Recent activity data indicates a downward trend in steel plant operations amid these restrictive measures impacting both Ukrainian exports and local demand stability.

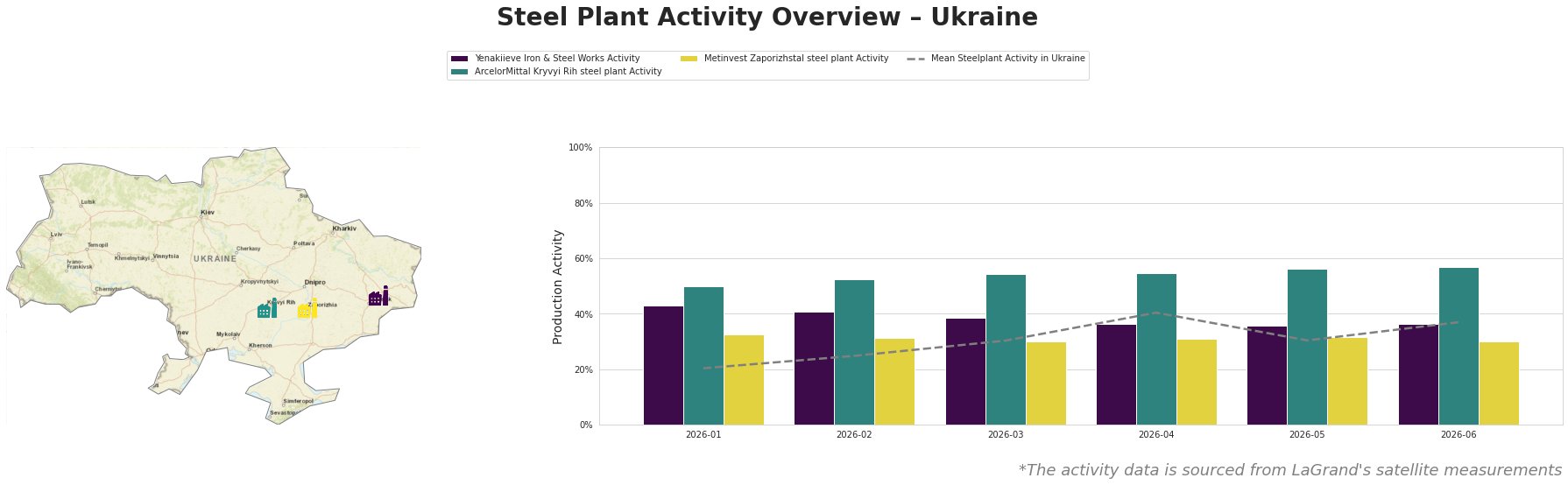

Recent satellite observations show that ArcelorMittal Kryvyi Rih (AMKR) recorded a notable increase in activity, peaking at 57% in June, the highest across the three plants. However, this increase may not be sustainable due to external pressures from the new UK and EU import tariffs, which compel steel mills in Ukraine to navigate a tougher competitive landscape. Conversely, both Yenakiieve Iron & Steel Works and Metinvest Zaporizhstal exhibited stable but low activity levels, maintaining around 36-32% and 30% respectively, suggesting limited upward mobility in operations.

Yenakiieve Iron & Steel Works, located in Donetsk, is primarily involved in the production of semi-finished and finished rolled products with a historically integrated process. Its activity declined to 36% in June, but remains stable despite the broader market challenges. Notably, this decline does not seem directly linked to the recent news articles.

ArcelorMittal Kryvyi Rih, the largest facility, managed to slightly increase activity to 57% in June, yet faces pressing challenges as highlighted in the British steel fabricators are calling for the new steel measures to be revised article, which raises concerns over market stability and competitiveness due to increased import costs and potential supply shortages.

Metinvest Zaporizhstal also remains stagnant at 30%, focusing on finished rolled products. With limited production flexibility and a reliance on deployment to competitive markets affected by tariff changes, the plant’s stability is under scrutiny.

Market implications suggest potential disruptions in supply as UK and EU tariffs could limit available raw materials, exacerbating the challenges faced by local mills that rely on exports. Steel procurement professionals are advised to prioritize early sourcing and potentially consider diversifying supply channels outside of heavily tariffed ranges.

Given the unfolding dynamics captured by these news articles and recent activity levels, steel buyers should be prepared for price volatility and possibly diminished availability of certain products, notably as the new import quotas take effect in the coming months.