From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Overview: Steady Recovery Amidst Capacity Restarts

Recent developments in the European steel industry reflect a neutral market sentiment, primarily influenced by operational changes within key steel plants. Noteworthy articles such as “ArcelorMittal to restart Gijon BF B next week“ and “ArcelorMittal resumes production at blast furnace B in Gijón“ detail the planned resumption of operations at Gijón, while the “Review of global steel production and production capacities conducted by MEPs“ highlights broader production trends amidst potential regulatory impacts on trade.

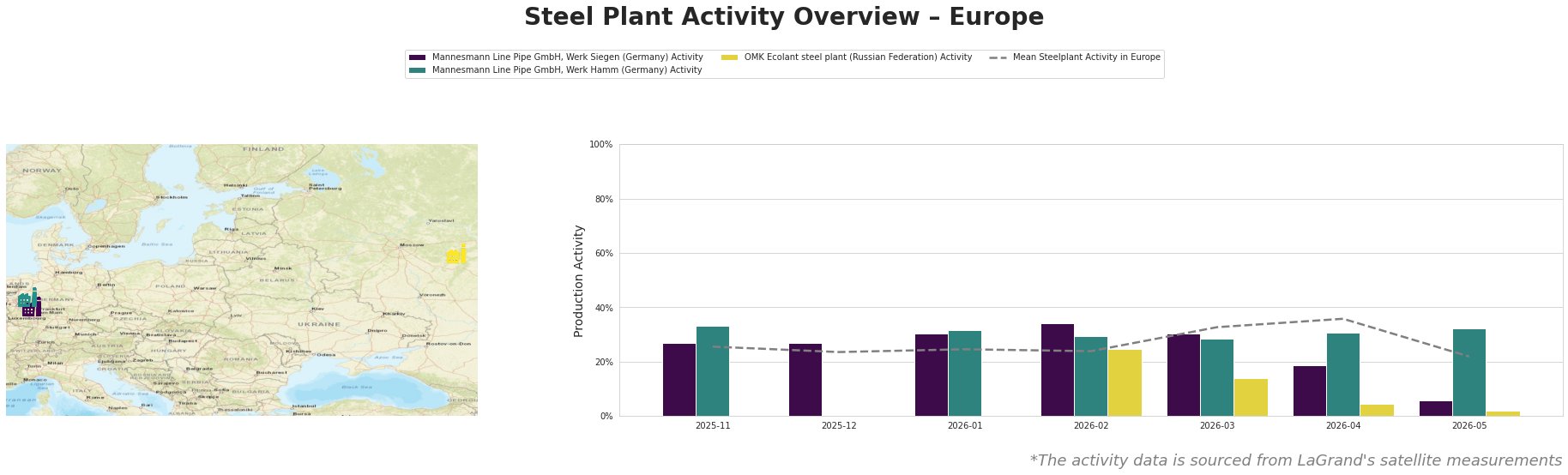

Satellite observations indicate a varied activity landscape across selected steel facilities in Europe:

The mean activity level across facilities reached a peak of 36.0% in April 2026, followed by a decline to 22.0% in May 2026. This fluctuation is particularly notable in the activities of Mannesmann’s Siegen plant, which saw a significant drop from 19.0% to 6.0%, coinciding with the uncertainty expressed in “EU protective measures against steel imports may be ineffective – ArcelorMittal Spain” regarding tariffs. Conversely, Mannesmann’s Hamm plant maintained higher levels of activity, potentially linked to ongoing trade and production strategies.

Mannesmann Line Pipe GmbH, Werk Siegen

The Siegen facility primarily utilizes EAF technology for pipe production. Its activity levels waned sharply in May, aligning with industry-wide concerns raised about EU trade measures and increased import tariffs, although no direct connection to specific production changes at this site was established.

Mannesmann Line Pipe GmbH, Werk Hamm

Similar to Siegen, Hamm operates primarily with EAF technology. Recent operational data indicates steady activity despite broader market fluctuations. With a maintained level of 32.0%, Hamm’s resilience amidst external challenges reflects its strategic positioning within the market.

OMK Ecolant Steel Plant

Operational in the Russian Federation, OMK Ecolant features a DRI-EAF production process with a significant capacity of 1,800 tons. Its activity levels fell to 2.0% in May, suggesting substantial disruptions. However, no direct links to the previously mentioned news articles were evident, indicating that challenges may stem from broader market dynamics, including sanctions or logistic issues that require further attention.

Evaluating the market implications, the expected restart of blast furnace B at Gijón could alleviate some supply constraints and potentially stabilize the market with increased capacity at a strategic moment when demand is projected to rise due to new EU protective measures.

Steel buyers should prepare for fluctuating availability from Mannesmann’s Siegen plant, given its recent activity drop, while also capitalizing on steady production from Hamm. It is advisable to closely monitor the Gijón operations, particularly post-restart, to gauge its full impact on market conditions. In light of increasing Brazilian slab imports to the EU, steel procurement strategies may also benefit from reviewing global sourcing options to mitigate localized supply disruptions.