From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market Insights: UK Quota Cuts and Activity Trends Indicate a Neutral Outlook

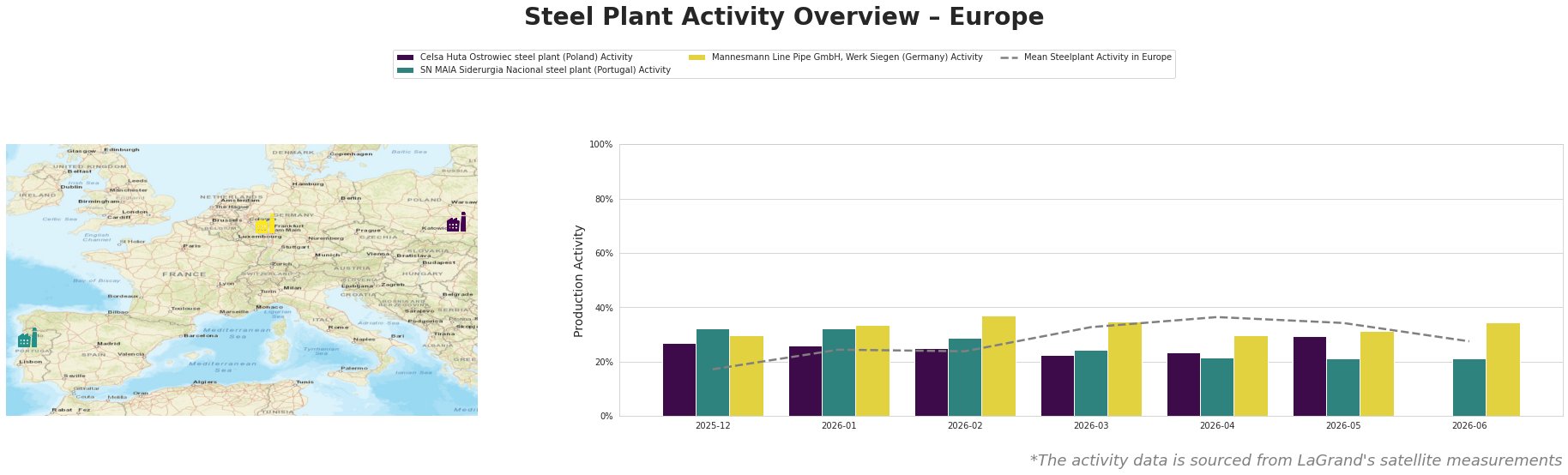

The European steel market is experiencing a period of adjustment following the UK’s announcement of a 60% reduction in steel import quotas to protect local production. This measure aims to counteract challenges defined in the OECD report about projected global steel overcapacity. Correspondingly, satellite data reveals varied activity levels across selected steel plants, reflecting the implications of these regulatory changes and market dynamics.

Recent satellite observations indicate a downturn in activity across certain steel plants. The activity level at the Celsa Huta Ostrowiec steel plant declined from 27% in December 2025 to 21% in June 2026, reflecting a gradual reduction despite prior increases. This drop could be indirectly influenced by market shifts following both the UK to cut steel import quotas by 60% to protect domestic steel industry and The UK has announced the details of the transition period for steel safeguard measures. However, direct correlations between specific quota measures and plant-level performance remain elusive.

The SN MAIA Siderurgia Nacional steel plant shows a stable yet low activity level, dropping from 32% to 21% in the same period, indicating a substantial decrease. The lack of connection to the named articles suggests that wider regional economic factors may be at play rather than UK-specific regulations translating directly to Portuguese operations.

In contrast, the Mannesmann Line Pipe GmbH, Werk Siegen maintained a stable operation around 35%, reflecting a robust position amid fluctuating input costs driven by tariff changes. This stability may partly be attributed to a consistent demand for pipes, which is less sensitive to the impending import restrictions highlighted in UK to cut steel import quotas by 60% to protect domestic steel industry.

The neutral market sentiment suggests potential supply disruptions, especially for materials traditionally imported from the UK. Steel buyers may want to reassess procurement strategies focusing on local suppliers or establishing contracts ahead of the quota implementation on July 1, 2026. Additionally, ongoing developments regarding The UK may consider easing new protective measures on steel – media reports should be monitored closely for potential shifts that could influence supply chain dynamics further.

In summary, while the UK’s protective measures may bolster domestic steel production in the short term, potential complications from tariff impositions may lead to increased costs and availability concerns, necessitating agile procurement strategies from industry players across Europe.