From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineAsia Steel Market Report: Coping with Overcapacity and Declining Demand in 2026

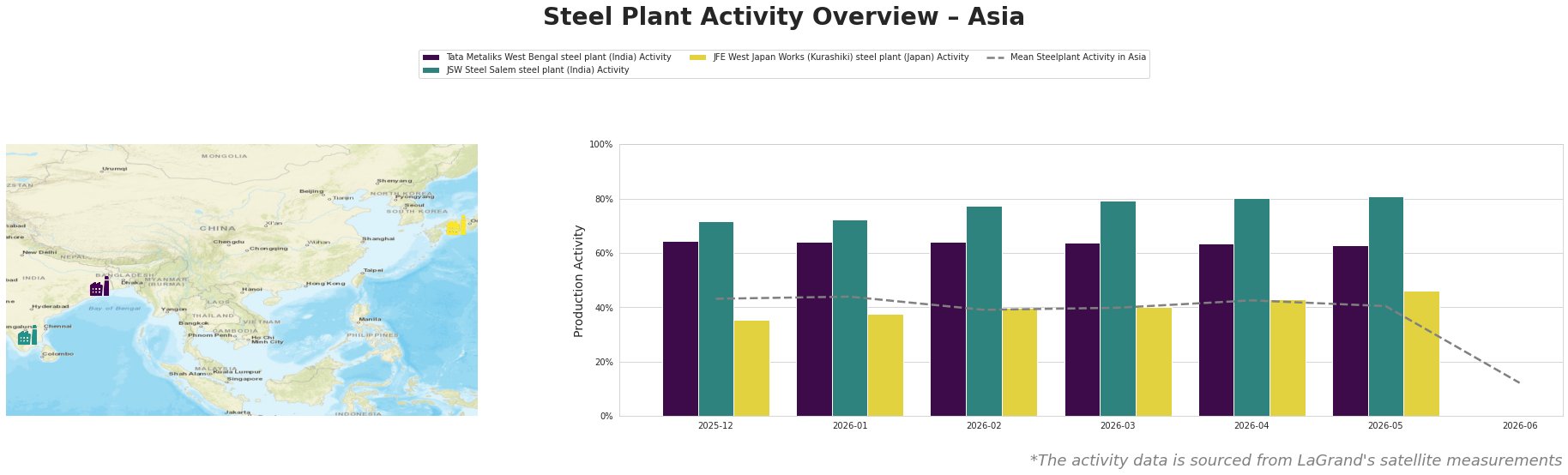

The Asian steel market is grappling with considerable challenges stemming from Global steel overcapacity deepens: OECD and the increasing use of anti-dumping measures as detailed in Anti-dumping measures on steel remained a common tool in 2025 – OECD. These insights correlate with recent satellite observations of steel plant activities, revealing a downward trend across various facilities.

Recent measurements show activity at the JFE West Japan Works dropped significantly, plunging to 12%, suggesting a severe contraction possibly tied to the projection of excess capacity, as outlined in the OECD: Global steel excess capacity set to reach 745 million mt by 2028. Other plants, like JSW Steel Salem and Tata Metaliks, maintained relatively stable activity around 72% and 64% respectively, indicating resilience amid fluctuating demand. However, the activities reflect contrast against declining mean activity, particularly with JFE’s drastic drop, illustrating a potential risk for supply chain turbulence in Japan.

The Tata Metaliks West Bengal steel plant exhibits consistent production levels throughout, remaining largely unaffected at 64%. This performance suggests that its status as a producer of pig iron and ductile pipes positions it favorably amidst regional demands. Consequently, ongoing operations can facilitate stable supply, demanding further attention from steel buyers targeting specific semi-finished products.

Conversely, the JSW Steel Salem plant showed an upward trend peaking at 81% activity in May. This growth may point to adaptability in meeting local requirements as noted against decreasing global demands; however, tailored procurement strategies should ensure that additional capacity does not lead to previous pitfalls highlighted in the OECD reports about global overcapacity.

Evaluating these aspects, potential supply disruptions especially from the JFE plant indicate a re-evaluation of procurement strategies, particularly from Japanese suppliers. Steel buyers should consider diversifying sources to mitigate risks associated with specific facility outages or performance volatility.

In conclusion, procurement actions should focus on solidifying relationships with operational facilities like Tata Metaliks and JSW Steel Salem, while being particularly cautious with JFE West Japan Works due to its notable decline in activity, as the market sentiment remains firmly neutral amidst these interconnected challenges.