From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineAsia Steel Market Report: Neutral Sentiment Amid Variable Plant Activity – Insights and Buying Strategies

Recent developments in the Asian steel market reflect a neutral sentiment, primarily influenced by external factors such as changes in US export data and supply disruptions related to the US-Iran conflict. Key articles such as “US merchant bar exports down 17.8 percent in April 2026 from March“ and “India’s base oil imports fall in April on US-Iran war“ have highlighted significant shifts in trade dynamics, although these do not directly correlate with changes in local plant activities across Asia.

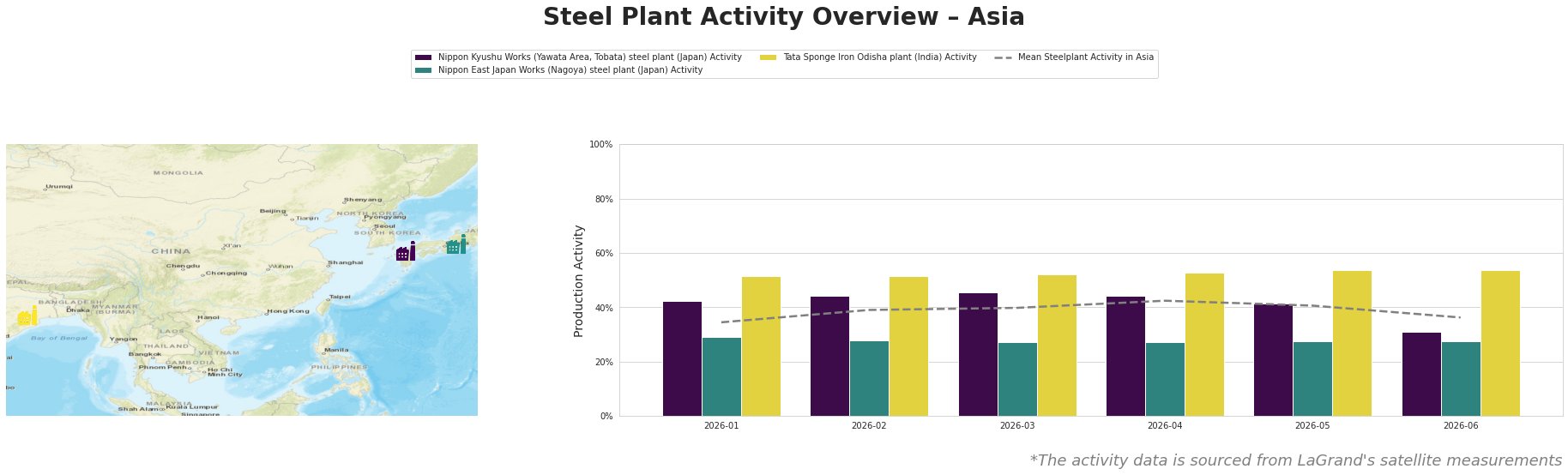

Measured Activity Overview

The overall mean activity in the Asian steel sector peaked at 42.0% in April 2026 but subsequently declined to 36.0% by June. Notably, the Nippon Kyushu Works saw a drop from 44.0% to 31.0% between April and June, contrasting the steady activity levels maintained by the Tata Sponge Iron Odisha plant, which remained at 54.0%.

The declining activity at the Nippon Kyushu Works could imply a diversification of supply chains, as indicated by the “US plates in coil imports decrease 50.3 percent in April 2026 from March“ report, revealing reductions in imports that may drive Asian producers to recalibrate their production strategies.

Plant Information

Nippon Kyushu Works (Yawata Area, Tobata), with a crude steel capacity of 3,727 metric tons, specializes in integrated processes, mainly producing semi-finished and finished steel products. Activity dropped from 44.0% in April to 31.0% in June, a 29.5% decrease, without a clear link to recent export trends. This decline aligns with broader regional trends but lacks direct causation with the highlighted news articles.

Conversely, Nippon East Japan Works (Nagoya), maintaining a steady 28% activity through June, operates a larger capacity at 6,000 metric tons. Its extensive focus on automotive and infrastructure products aligns with consistent demand, albeit without direct implications from recent US export declines.

Tata Sponge Iron Odisha, focusing on Direct Reduced Iron (DRI), observed stable activity at 54.0%, showing resilience amid regional disruptions. This could correlate indirectly with reduced Indian base oil imports, as highlighted in “India’s base oil imports fall in April on US-Iran war”, affecting raw material availability and influencing procurement strategies moving forward.

Evaluated Market Implications

The observed declines in activity at facilities like Nippon Kyushu may signal potential supply disruptions due to recalibrations in production cycles in response to external market pressures. For procurement professionals, a versatile supply strategy is essential:

- Explore diversified sourcing options from regions less impacted by the US-Iran conflicts that have shown increased shipment activities, like increased imports from Taiwan.

- Consider high-volume opportunities linked to stable producers such as Tata Sponge Iron, who have shown resilience in their throughput, potentially providing a stable product supply amidst fluctuating market conditions.

By closely monitoring these trends in tandem with geopolitical developments, steel buyers can refine their procurement strategies to navigate potential challenges effectively.