From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEurope Steel Market Outlook: Neutral Sentiment Amid UK Industry Concerns and Activity Fluctuations in Key Steel Plants

Recent developments in the European steel market reflect a neutral sentiment, influenced primarily by the UK’s protective steel quotas. The articles titled “Measures to protect the UK steel industry continue to provoke a negative reaction from the industry, despite the updates“ and “UK steel safeguards continue to face industry backlash despite updates“ highlight ongoing industry dissatisfaction and potential disruptions as companies brace for challenges in Q1 2027 tied to increased costs from new carbon controls. However, satellite activity data show no significant direct correlation between these developments and observed changes in activity levels of major steel plants.

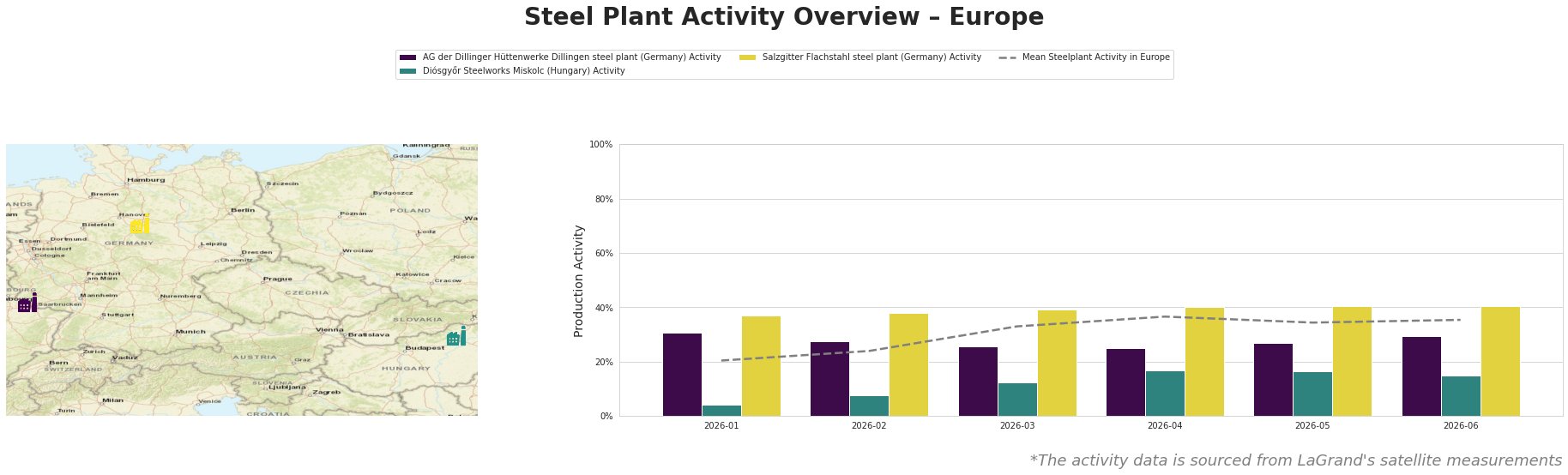

The AG der Dillinger Hüttenwerke Dillingen steel plant showed a steady decline in activity from 31% in January to 25% in April, before slightly recovering to 29% in June. This aligns with industry concerns from the aforementioned articles regarding domestic production challenges as new quotas threaten profitability.

Diósgyőr Steelworks Miskolc demonstrated minimal activity, with levels rising from 4% in January to only 17% by April, stabilizing at 15% by June. The activity levels do not directly link to the recent UK policy changes but reflect an ongoing struggle to meet market demands.

In contrast, the Salzgitter Flachstahl plant maintained a relatively high activity level, gradually increasing from 37% in January to 41% in June. This indicates resilient production capacity, yet how and if this can counterbalance the anticipated supply shortages in the UK remains uncertain.

As clarified in “British steelmakers are calling for an improvement in the terms of trade in steel with the EU,” rising tensions in trade negotiation may exacerbate existing supply issues, particularly as UK steelmakers depend heavily on EU markets. This backdrop suggests potential supply disruptions that European buyers should consider.

Procurement Recommendations:

– Buyers should strategically negotiate contracts well in advance, particularly for purchasing from the AG der Dillinger Hüttenwerke and Diósgyőr Steelworks, given rising concerns about product shortages and potential pricing pressures.

– With Salzgitter Flachstahl exhibiting stable activity, sourcing from this plant may offer a buffer against potential supply disruptions originating from the UK due to regulatory changes.

In summary, while the immediate sentiment remains neutral, critical factors—including the protective quotas in the UK, changing import laws, and varying activity levels across plants—prompt steel buyers to adopt proactive and targeted procurement strategies to mitigate risks.