From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineNegative Steel Market Outlook for Oceania Driven by Diminished Activity Levels and European Trends

Oceania’s steel market sentiment is notably negative, influenced by weakened demand and declining activity levels across key steel plants. The article “Green flat steel demand near zero in Europe“ highlights a significant reluctance to invest in sustainable steel solutions, leading to stagnant pricing and minimal movement in the steel sector. Furthermore, “Trading activity in European steel HRC market remains slow on high stocks, uncertainty“ reflects similar trends impacting regional inventories and confidence, crucially linking reduced demand in Europe to the activity levels observed in Oceania.

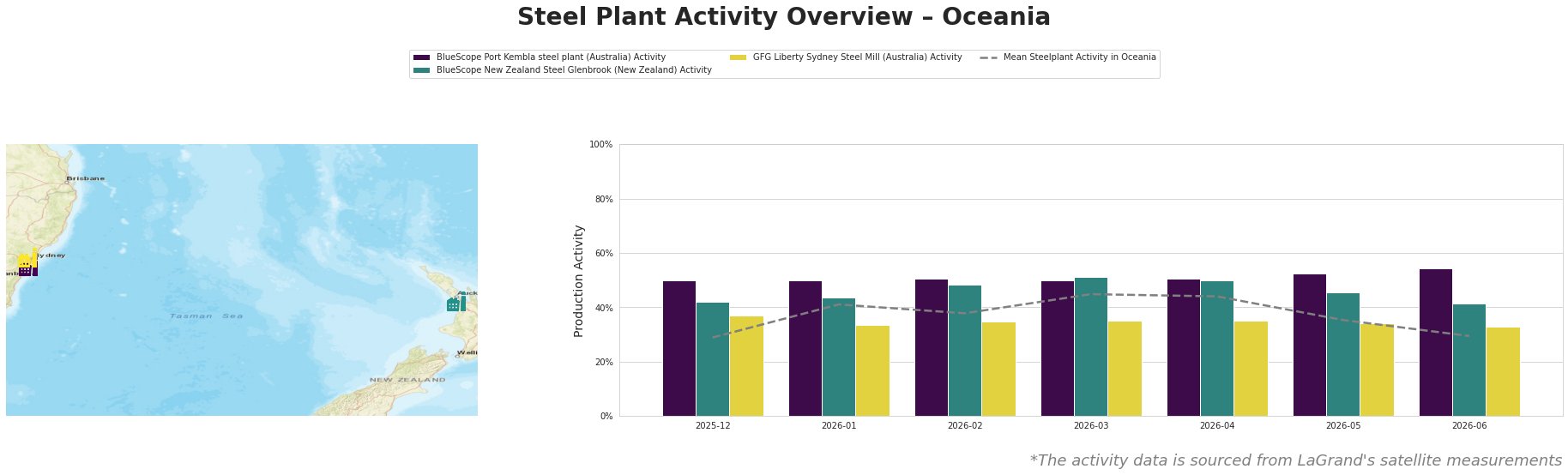

Recent activity at steel plants shows concerning declines, notably a drop to 29.0% mean activity in June, aligning with decreasing demand signals from Europe. The BlueScope Port Kembla plant has experienced a decline from 52.0% in May to 54.0%, indicating some production resilience but still falling short of sustainable operational levels. Meanwhile, BlueScope New Zealand Steel Glenbrook peaked at 51.0% in March but subsequently regressed, evidencing instability likely linked to uncertainties in both regional and international markets. The GFG Liberty Sydney Steel Mill remains sluggish, with activity levels stagnating around 33.0%, which could correlate with the apprehension reflected in the European trade articles.

These developments draw an explicit line to the broader European challenges, where stagnant demand and high inventories are projected to influence Oceania’s export potential as buyer sentiment remains tepid. The reluctance to shift towards greener steel solutions as seen in Europe suggests that similar trends could inhibit investment and innovation in Oceania.

Given the observed activity declines, steel buyers should prepare for potential supply disruptions, particularly from BlueScope and GFG Liberty, where sustained low activity could hamper timely delivery of products. A proactive procurement approach, focusing on securing long-term contracts now at traditional price levels, could mitigate risks associated with future price increases as regional demand thaws or pricing stabilizes post-summer holidays. With indications of hesitant buyer sentiment primarily linked to costs and uncertainties reflected in European markets, securing stocks in anticipation of upcoming shifts becomes a critical strategy.