From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineOptimistic Outlook for European Steel Market Amid UK Tariff Changes: Key Plant Activities Observed

Recent developments in the European steel market highlight a positive trajectory, spurred by the UK government’s announcements regarding import tariffs. The articles titled “UK to cut steel import quotas by 60% to protect domestic steel industry“ and “The UK has announced new tariffs on steel imports for the transition period“ elucidate changes leading to increased domestic production focus, which aligns with rising activity levels at several key steel plants in Europe.

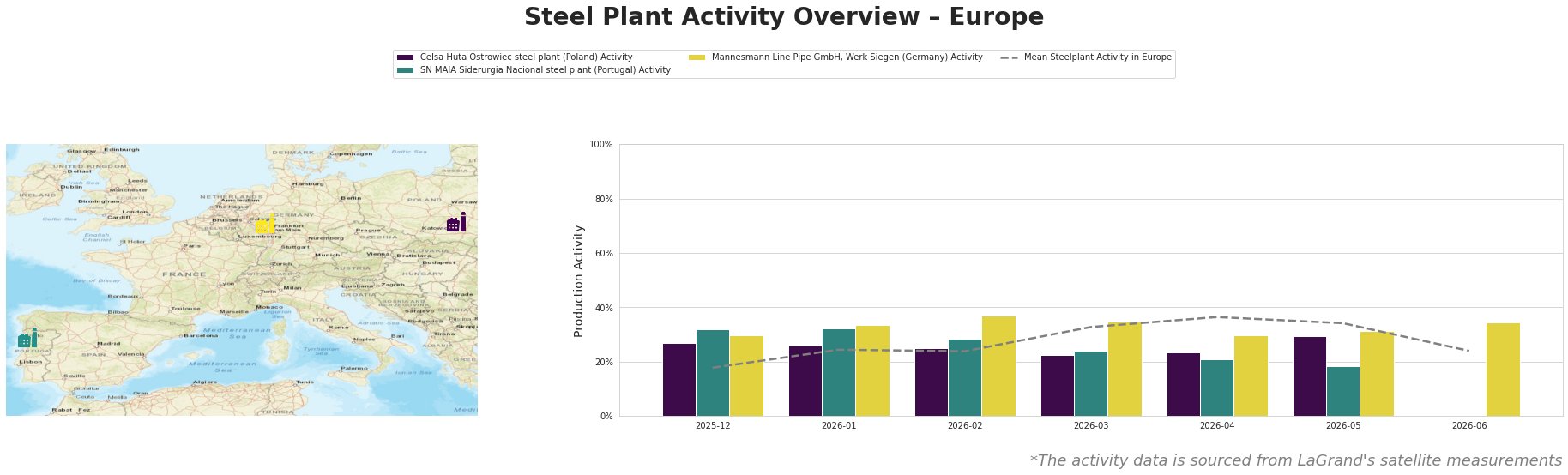

Celsa Huta Ostrowiec exhibited a marked decline from 29% in May 2026 to not reported in June 2026, with no discernible link to the recent UK tariff changes as indicated in “UK to cut steel import quotas by 60% to protect domestic steel industry”; however, its activities reflect broader market fluctuations. SN MAIA Siderurgia Nacional saw a drop to 18% in May but recovered by October, positioning it during this transitional tariff setup as crucial for fulfilling local demand possibly impacted by the UK transition strategy. Mannesmann Line Pipe GmbH maintained resilience with its activity rising to 35% in June 2026, potentially benefiting from flexible supply chains amid UK market adjustments.

Celsa Huta Ostrowiec, situated in Poland, links predominantly to construction with significant output in rebar and bars. The steel plant is entirely based on Electric Arc Furnace technology with a capacity to produce 900,000 tons of crude steel annually. The observed decrease in activity percentage may correlate indirectly with the changes in UK tariffs which pose significant implications on demand dynamics in regional markets.

SN MAIA Siderurgia Nacional, based in Portugal, is also structured around EAF technology, producing approximately 600,000 tons annually, primarily focusing on rebar for various sectors, although recent activity levels have not reflected a direct correlation with tariff impacts. The plant’s operational environment amid new UK regulations suggests potential for growth as local players seek to fulfill existing and new market requirements.

Mannesmann Line Pipe GmbH operates primarily in the production of pipes, exhibiting enhanced activity levels despite fluctuation, positioning themselves strategically to cater to increased demand in domestic supply chains likely affected by UK policy changes. Although no specific link can be drawn from recent UK news to its operations, the overall market sentiment remains positive for the plant given the expectations of heightened local demand.

The clearly defined potential supply disruptions arise primarily from Celsa Huta Ostrowiec’s current uncertain activity status and the potential struggles for SN MAIA Siderurgia Nacional. For procurement professionals, the recommendation is to closely monitor developments around the transitional tariffs instituted in the UK, as these will likely dictate strategic purchasing decisions going forward. Additional focus should be placed on establishing stronger supply relationships with Mannesmann, which is currently positioned advantageously in the evolving market landscape.