From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineUkraine Steel Market Report: Activity Trends Amid EU Quota Changes and Domestic Price Surge

Ukraine’s steel industry faces critical challenges following the extension of anti-dumping measures on seamless pipes from China as outlined in “Ukraine has extended anti-dumping measures on imports of seamless pipes from China“ (2026-05-27). Concurrently, significant shifts in domestic market dynamics and the EU’s geopolitical posture influence operational activities within the sector.

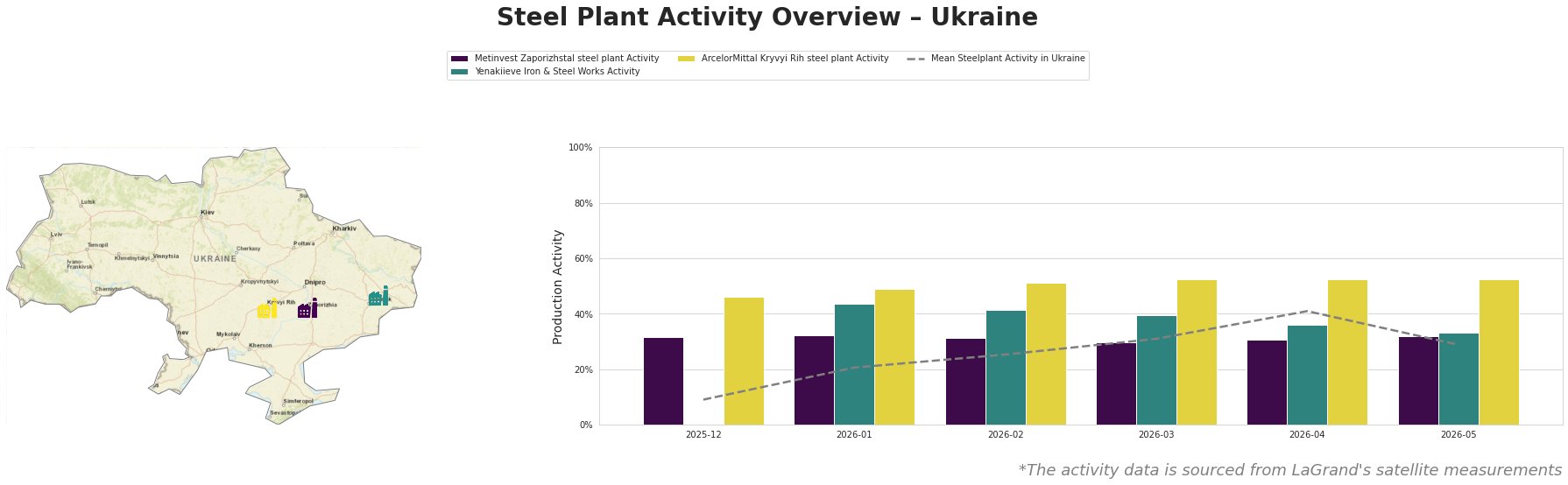

Recent observations from satellite data show that mean steel plant activity in Ukraine reached 29% in May 2026, a decrease from 41% in April. Specifically, Metinvest Zaporizhstal reported steady activity at 32%, while ArcelorMittal Kryvyi Rih maintained a stable 52% activity level. Yenakiieve Iron & Steel Works, however, saw a decline to 33%, aligning with disruptions likely tied to the overall market instability discussed in “The euroquote on steel will hit hard the Ukrainian metallurgists affected by the war, – CEO Interpipe” (2026-05-31), though no direct correlation to plant-specific changes was established.

Metinvest Zaporizhstal remains stable with a significant focus on finished rolled products including hot-rolled sheets and steel strips. The plant’s consistent operational level reflects a resilient adjustment despite external pressures from increased import tariffs highlighted in “Ukraine should be exempted from steel quotas under the EU’s new trade measure – Luca Zanotti“ (2026-05-28).

Yenakiieve Iron & Steel Works, on the other hand, has seen a drop to 33%. This aligns with continuous turmoil in the region, supporting the assertion made by Zanotti that ongoing geopolitical issues have drastically reduced Ukraine’s steel production capacity by 80% since 2022. This historical context underscores challenges faced by plants specialized in semi-finished and finished rolled categories, such as rebar and wire rods.

ArcelorMittal Kryvyi Rih’s operational status remains robust at 52%. The consistency of its output amidst fluctuating activity levels emphasizes the plant’s critical role in supplying semi-finished goods for construction and infrastructure, catering to steady domestic demand, especially amidst reported price increases of 9–10% for rolled steel products in May (see “Domestic prices for hot-rolled steel and pipes rose by 9–10% in May“, 2026-06-02).

In response to these market dynamics, steel buyers should prioritize establishing robust relationships with producers maintaining steady output, particularly ArcelorMittal and Metinvest, to ensure supply consistency. Monitoring further developments around EU trade policies and domestic price surges will be essential, as they may affect procurement strategies and costs going forward. Given the current market sentiment of neutrality, forward-looking assessments should also evaluate potential disruptions arising from ongoing geopolitical situations.