From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Momentum in European Steel Market: Strong Performance and Strategic Insights

In Europe, the steel market is witnessing a positive momentum driven by significant activity shifts in key production plants. Recent reports indicate that “Ukraine increased exports of pig iron by 11.2% y/y in January–April“ and while exports of flat steel also saw a growth, shipments of semi-finished products experienced a 15.7% m/m decline in April, showcasing mixed trends that influence the regional market dynamics.

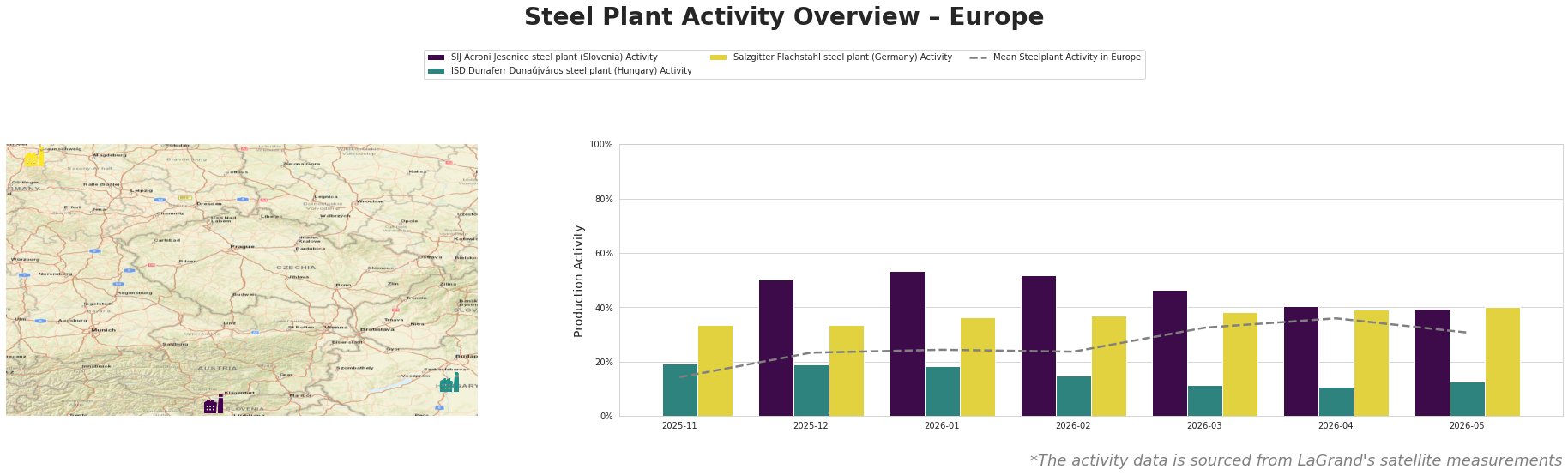

The SIJ Acroni Jesenice steel plant in Slovenia demonstrated a peak activity level of 54% in January 2026, yet faced a subsequent decline to 40% by April. This aligns with the reported decline in overall European export levels, specifically noted in the “Ukraine saw a 15.7% m/m decline in exports of semi-finished products in April“, indicating that reduced exports may have impacted plant operations. In contrast, Salzgitter Flachstahl in Germany displayed stable production with minor fluctuations, remaining relatively resilient amidst the broader Market fluctuations.

ISD Dunaferr’s activity fell sharply to 11% in March and April 2026, aligning with the broader challenges highlighted in “Ferroalloys exports from Ukraine fell to 3,900 tons in January–April“, where disruptions in supply chains have been significant. Meanwhile, Salzgitter’s capacity has allowed it to maintain activity around 40%, leveraging energy projects aimed at sustainable steel production.

Considering these developments, the following strategies are crucial for steel procurement professionals:

– Alternative Sourcing: The reductions in semi-finished product exports from Ukraine may necessitate identifying alternative sourcing options. Investigate domestic suppliers or alternative international markets for semi-finished steel components.

– General Monitoring of Plant Activity: Ongoing monitoring of the SIJ Acroni and ISD Dunaferr activity levels is advised, as strategic engagement or pre-ordering may be beneficial in times of fluctuating production capacity.

– Prioritize On-time Procurement: Engaging with Salzgitter and other facilities demonstrating stable output could ensure consistent supply amidst global uncertainty, especially given the potential for increased raw material costs or logistical interruptions.

In summary, the current positive sentiment underpinned by rising exports and recovery prospects stands alongside challenges that necessitate attentive procurement strategies tailored to the evolving landscape of the European steel market.