From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EnginePositive Outlook for Europe’s Steel Market Despite Short-Term Challenges

Recent developments in the European steel market indicate a positive sentiment driven by sustained price levels and selective production adjustments. Specifically, the article Iberian HRC prices remain steady, demand volatile highlights that while hot rolled coil (HRC) prices have maintained stability around €730-740 per tonne in Spain amidst weak demand, producers are scaling back to manage price levels. Additionally, No rebound in sight for European HRC as deals dry up underscores the trading standstill affecting HRC prices in Germany and the Benelux region, further aligning with observed reductions in plant activity levels.

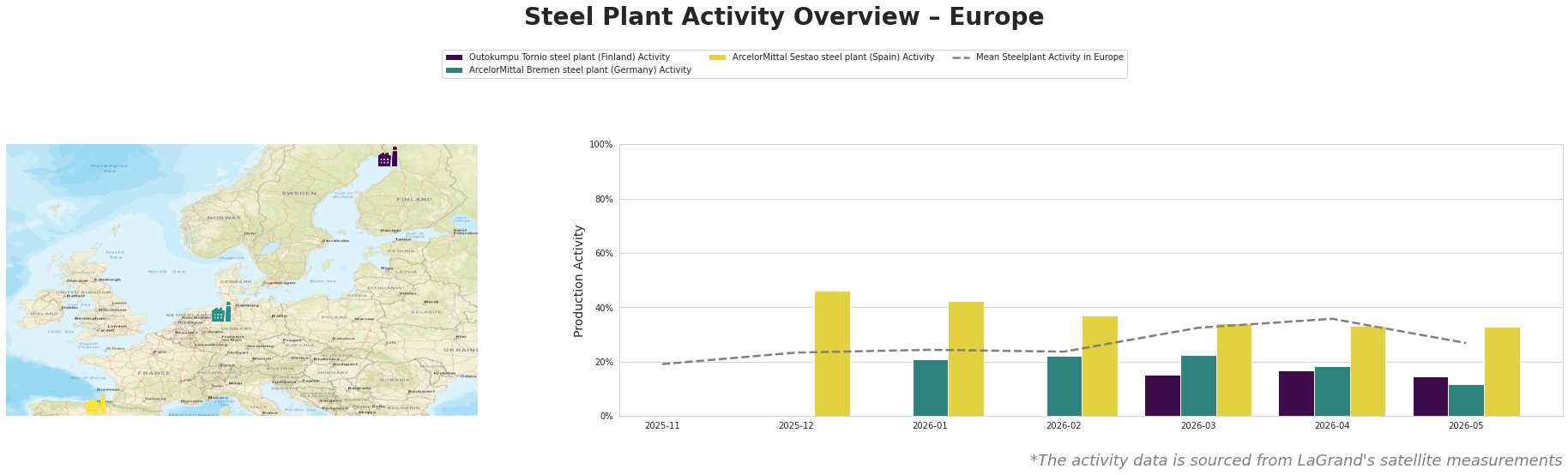

The overall activity in the European steel market averaged 27% in May, with notable variations among key plants. The Outokumpu Tornio steel plant reported a decrease to 15% activity, reflecting the industry’s caution amidst rising costs and geopolitical tensions as noted in Iberian HRC prices remain steady, demand volatile. In contrast, the ArcelorMittal Sestao saw consistent activity at 33%, maintaining its capacity for hot rolled coils.

The ArcelorMittal Bremen plant faced reduced activity at 12%, closely tied to a cautious approach to fill summer order books as per No rebound in sight for European HRC as deals dry up. This aligns with widespread hesitance in buyer engagement, leading to a standstill in new contracts and further emphasizing the market’s cautious mindset.

The European import flat steel market largely quiet awaiting clarity on safeguard article confirms limited activity driven by uncertainties regarding new safeguards affecting incoming steel prices. However, it also highlights Turkish HRC offers, providing essential context for procurement strategies amid shifting demand landscapes.

In terms of actionable insights for steel buyers, procuring from consistently active plants like ArcelorMittal Sestao may ensure stability, particularly for contracts valued around €665-680 for substantial orders, as larger procurements might yield better pricing. Conversely, reduced activity levels at Outokumpu Tornio and Bremen suggest potential supply disruptions, indicating a need for strategic foresight in sourcing, especially given the uncertainty highlighted around imports and regional price fluctuations.

In conclusion, while the European steel market currently exhibits a positive outlook driven by strategic production adjustments, stakeholders should remain vigilant regarding described market dynamics and consider procurement strategies that incorporate current plant activity trends and geopolitical influences.