From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Update: Stability Meets Caution Amid Rising Costs and Demand Challenges

Recent reports indicate a neutral sentiment prevailing in the European steel market, with noteworthy developments in plant activity levels. The article “Iberian HRC prices remain steady, demand volatile“ highlights the ongoing weak demand for hot rolled coil (HRC) in Spain, influenced by the US-Israel-Iran conflict, prompting steelmakers to scale back production amid cautious buyer behavior. This caution is further echoed by “No rebound in sight for European HRC as deals dry up,” illustrating stagnant prices and limited transactions suggesting a market unwilling to engage at elevated price points. Although no direct correlation can be drawn from these articles to specific plant activity fluctuations, they reflect broader trends influencing market behavior.

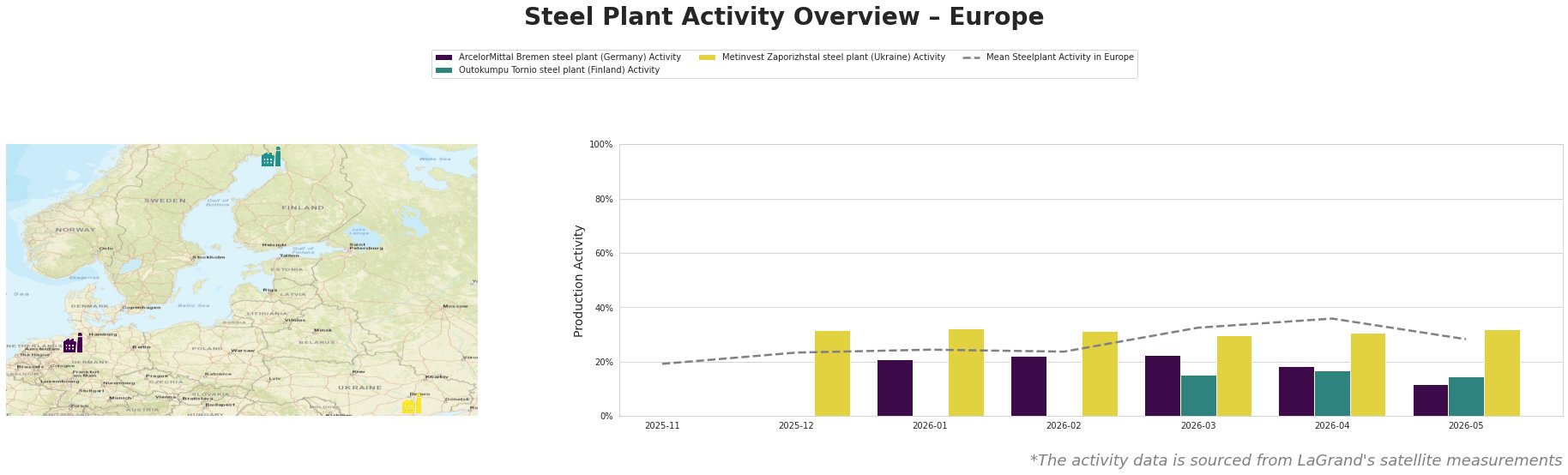

The ArcelorMittal Bremen steel plant has seen a noticeable decline, with activity dropping from 18.0% in April to 12.0% in May. This drop in activity aligns with the general market fatigue observed in the “No rebound in sight for European HRC as deals dry up,” reflecting a stagnant trade environment contributing to lower operation rates. The plant, focusing on integrated processes primarily for automotive and infrastructure sectors, has not escaped the cautious purchasing environment impacting overall demand.

Conversely, Outokumpu Tornio’s activity remained stable at around 15.0% in May, consistent with the sluggish demand for finished products noted in the “European stainless flats prices continue to rise,” which cites rising prices but weak market absorption. This indicates that while prices are climbing, end-users are hesitant to commit to large purchases, impacting turnover rates.

On a more positive note, Metinvest Zaporizhstal continues to operate relatively consistently at 32.0%, maintaining productivity levels despite geopolitical challenges as referenced in the broader market news. Its integrated production capabilities for finished rolled products reinforce its resilience amidst the shifting landscape described in the articles.

The market reflects an overall caution, with steel buyers advised to closely monitor Iberian HRC prices and supply chain disruptions, as heightened transport costs and emerging EU regulations could disrupt procurement processes. Given the declining activity at Bremen and the stable production at Zaporizhstal, buyers should foster flexible procurement strategies, prioritizing contracts with reliable producers while negotiating terms that mitigate risks associated with the current geopolitical landscape. Additionally, it is advisable for buyers in regions influenced by protective measures to remain vigilant regarding the import dynamics articulated in “European import flat steel market largely quiet awaiting clarity on safeguard,” as future regulations may alter available supply lines and pricing structures.