From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineUkraine Steel Market Report: Navigating CBAM and Plant Activity Amid Ongoing Conflict

In Ukraine, the steel industry faces significant challenges stemming from the war and the evolving regulatory landscape, particularly regarding the Carbon Border Adjustment Mechanism (CBAM). Recent discussions highlighted in MEPs urge Commission to ‘reassess’ CBAM for Ukraine and The European Parliament has begun discussing a CBAM deferral for Ukraine reveal that lawmakers are advocating for a special treatment for Ukraine due to the war’s economic impacts, especially concerning steel exports. There is a notable 40% decline in steel production from pre-war levels alongside logistical challenges, as reported by the Business associations have called on the EC to adopt a special CBAM approach for Ukraine.

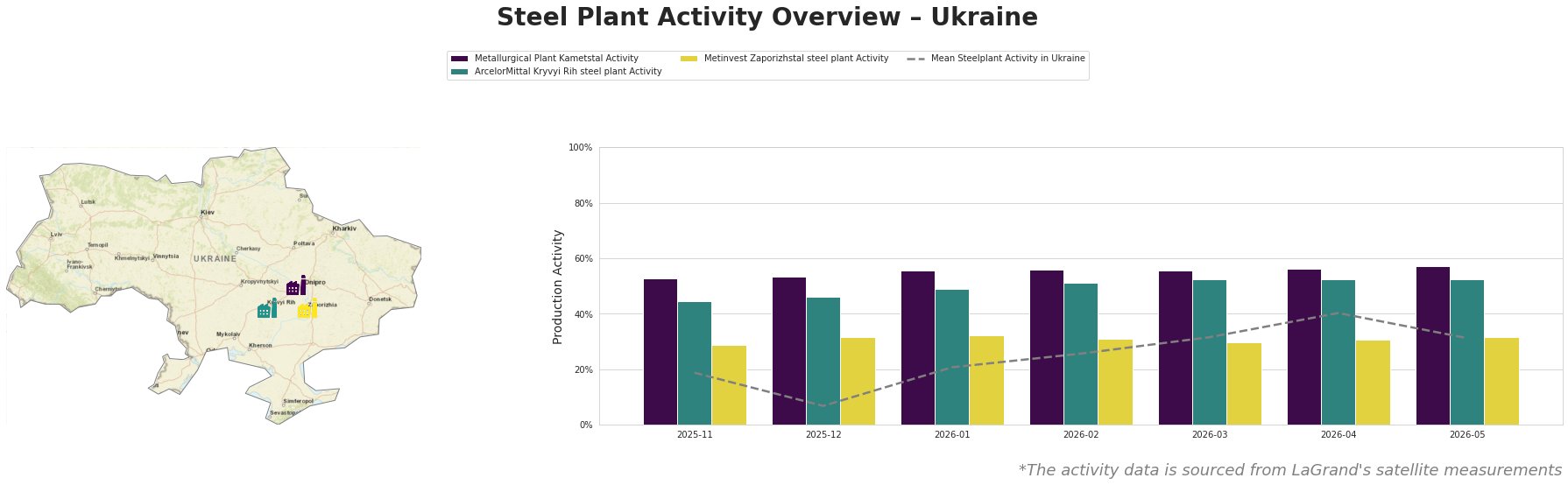

The satellite activity data reflects a significant drop in mean plant activity, especially noted in December 2025 with a low of just 7%. Specific plants such as ArcelorMittal Kryvyi Rih and Metinvest Zaporizhstal demonstrated slight resilience, operating at 46.0% and 32.0% in December 2025, respectively. Metallurgical Plant Kametstal has maintained a relatively steady operation, sustaining an activity level of 53.0% through this period. While Kametstal’s steady output may suggest an operational strategy to mitigate further declines, the overall downward trend is critical for market analysis.

At the Metallurgical Plant Kametstal, which produces semi-finished and finished rolled products employing integrated blast furnace (BF) technology, activity is currently around 57% as of May 2026. This is an essential indicator as it shows improvement and resilience compared to the lower December 2025 peak of 53%, demonstrating a potential response to the operational adjustments advocated in the recent discussions regarding CBAM. The connection to market demands amid ongoing war conditions is clear but remains precarious without specific exemptions.

ArcelorMittal Kryvyi Rih, producing a range of construction steel products, similarly shows a slight recovery, operating at 52% in May 2026 compared to its lower rates earlier in the year. While this indicates an effort to stabilize amid adverse conditions, the ongoing regulatory uncertainties underline vulnerability in future supply chains. Metinvest Zaporizhstal’s operations, affected by the overall drop in the industry, hovered around 30% during February, and only marginally improved to 32% in May, emphasizing the volatility of production capacity in the wake of war.

In conclusion, significant potential supply disruptions linger, particularly related to logistical challenges and CBAM regulations. Steel buyers are advised to anticipate delays and increased costs, especially if no exemptions from CBAM are granted. Proactive engagement with suppliers and careful inventory management are critical, particularly concerning sourcing from regions less affected by conflict or maintaining diversified supplier networks. It is imperative to keep abreast of further developments regarding policy changes related to Ukraine and the EU’s stance on CBAM.