From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Insights: Neutral Sentiment Amid Regulatory Changes and Plant Activity Variability

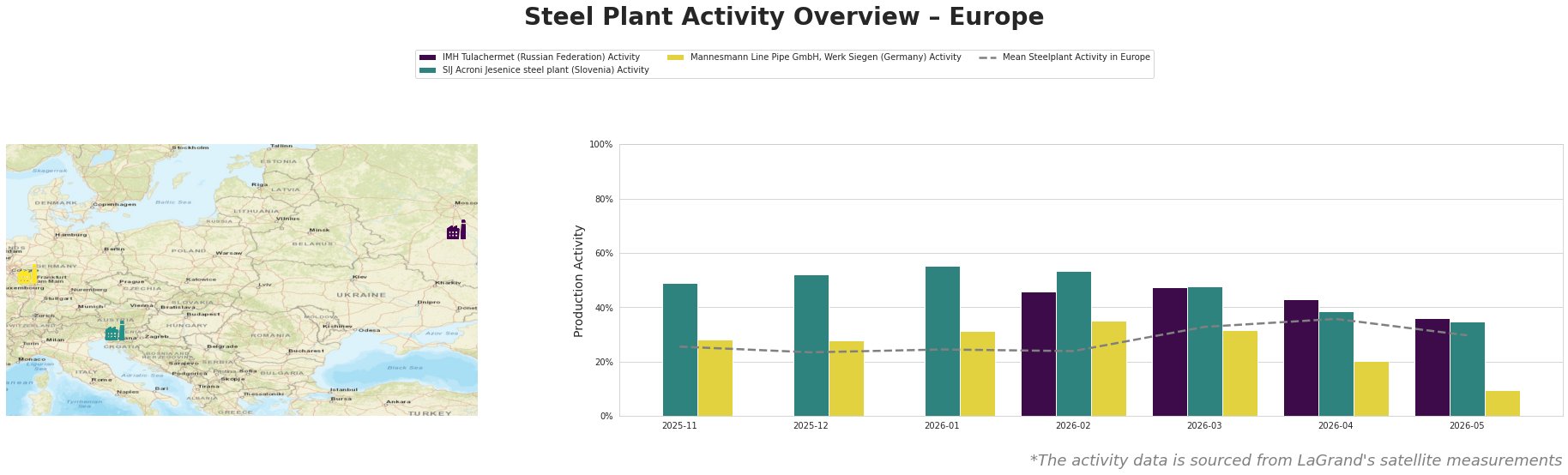

The European steel market is experiencing a neutral sentiment driven by regulatory changes and fluctuating plant activities. The WTO Committee reviews steel safeguards (April 30, 2026) and the EU’s 20th sanctions package further tightens restrictions on Russian steel-linked trade (April 29, 2026) provide context for ongoing shifts. Notably, these developments align with observed changes in plant activity levels, although direct relationships are not universally identifiable.

IMH Tulachermet recorded a notable decline, dropping from 48.0% in March to 43.0% in April, with no clear connection to recent news. In contrast, the SIJ Acroni Jesenice steel plant rose moderately until May, peaking at 55.0% in January but fell to 35.0% in May, which could reflect buyer hesitance amidst trade regulatory adjustments mentioned in the EU announces new steel import quota volumes and implementation changes (May 2, 2026). Mannesmann Line Pipe GmbH’s activity plunged from 32.0% in March to 20.0% in April, likely a reaction to the introduction of the UK’s protective trade measures for stainless steel highlighted in UK trade measures will lead to disruptions in the supply of stainless steel bars (April 30, 2026).

IMH Tulachermet focuses on integrated production yielding semi-finished and finished rolled products, highlighted by its 1800 kt crude steel capacity, whereas SIJ Acroni Jesenice, with 726 kt capacity, is driven by electric arc furnace (EAF) technology for flat rolled products vital for building and tools. Mannesmann, primarily producing pipes, displays a unique gap in producing crude steel but relies on sustained operation levels conditioned by other plant performances.

Specific potential supply disruptions may arise from the UK’s impending 60% reduction in stainless steel tariff quotas combined with the EU’s commitment to curb Russian steel imports significantly by 2028. Steel buyers should monitor SIJ Acroni for potential procurement, keeping in mind its current trajectory and regional competition dynamics. It may be prudent to reassess supply chain strategies involving import quotas and assign additional weight to local producers like IMH Tulachermet.

Furthermore, buyers should prepare for variability in pricing due to these regulatory frameworks and evaluate the feasibility of sourcing from plants with demonstrated activity stability amidst market uncertainties, especially within the context of sanctions impacting Russian supply routes.