From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineEuropean Steel Market Report: Positive Activity Shift Amidst Fluctuating Prices

European steel markets are witnessing a generally positive sentiment as recent activity levels at various plants show signs of recovery. In particular, the article “Thick-sheet steel prices in Europe are rising due to constant orders“ highlights a robust demand driving rising prices in thick steel sheets, which correlates with observed increases in plant activity.

On the other hand, the article “HRC prices in the EU remain mostly fluctuating as participants await clarity on guarantees“ indicates that hot-rolled coil (HRC) prices are stable yet uncertain due to anticipated regulatory changes impacting imports, suggesting a mixed buy-side sentiment that keeps some markets stagnant.

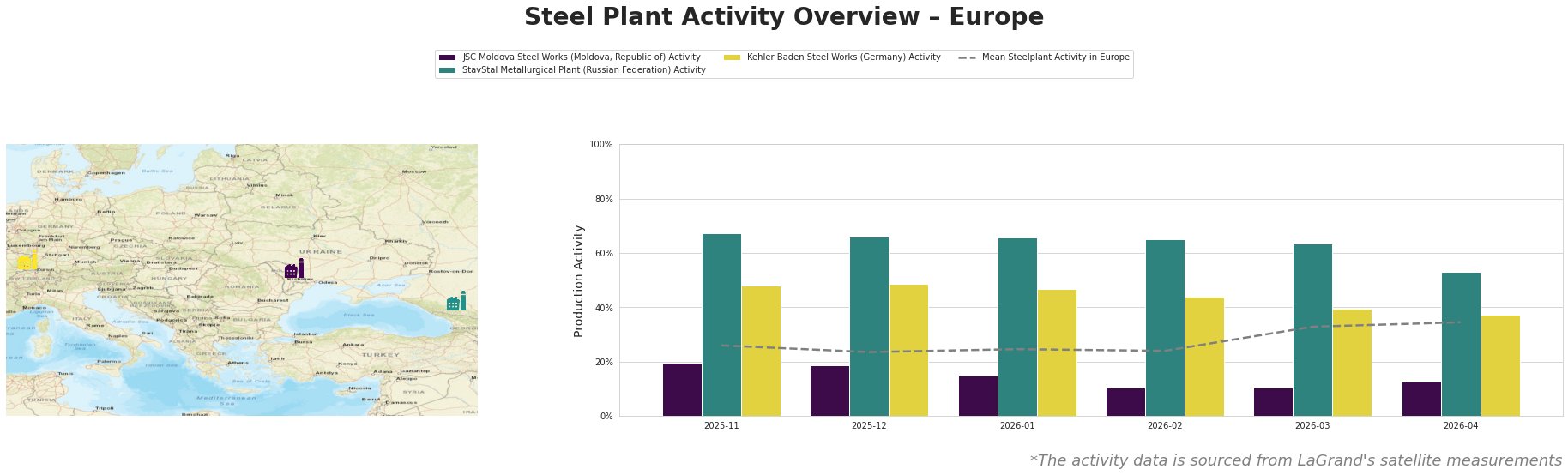

Measured Activity Overview

Recent data shows the mean activity level across Europe has increased dramatically from 24% in December 2025 to 35% in April 2026. Notably, JSC Moldova Steel Works experienced a marginal rise from 10% to 13%, although it remains significantly below the mean, indicating constrained production capacity linked to risks in the import market as noted in “HRC prices in the EU remain mostly fluctuating…”

Conversely, activity at the StavStal Metallurgical Plant remains robust compared to its peers, though it fell from 67% to 53%. Kehler Baden Steel Works exhibits a downward trajectory from 48% to 37%, aligning with thinning demand from rising prices of various products as pointed out in the “European rebar, wire rod prices continue climbing, acceptance limited“ article, where buyer hesitancy is evident.

JSC Moldova Steel Works

JSC Moldova Steel Works, utilizing Electric Arc Furnace (EAF) technology with a capacity of 1,000 tonnes, has seen activity levels stabilize at 13%. Despite a slight uptick, this level indicates a cautious approach likely influenced by the uncertainty highlighted in the aforementioned articles regarding market fluctuations and regulatory changes impacting material procurement.

StavStal Metallurgical Plant

The StavStal facility, with a capacity of 500 tonnes, reflects a strong EAF operation. The drop in activity from 67% to 53% may be tied to the cautious market sentiment surrounding pricing stability, as discussed in “European rebar, wire rod prices continue climbing…”, causing hesitation amongst buyers who anticipate declines.

Kehler Baden Steel Works

Kehler Baden Steel Works, capable of producing 2,500 tonnes via EAF, has seen a drop in activity to 37%. This decline highlights issuing demand directly attributable to consumer pricing concerns indicated in “HRC prices in the EU remain mostly fluctuating…” and the lower volume of customer purchases as pointed out in “European rebar, wire rod prices continue climbing…”.

Evaluated Market Implications

Potential supply disruptions could arise from the ongoing fluctuations in activity at JSC Moldova and Kehler Baden, both of which show less resilience compared to industry averages. Buyers should consider securing orders now from higher-activity plants like StavStal, which still maintain relatively stable production despite slight declines in activity, to mitigate risks associated with possible price increases following regulatory changes.

In addition, it is advisable for procurement teams to closely monitor the developments in EU market regulations around imports—as pointed out in multiple news sources—as these factors could lead to unexpected shifts in supply stability, suggesting proactive procurement strategies to secure necessary materials before further price inflation occurs.