From the Field to the Dashboard – Built by Experts, for Experts.

Discover What's Really Happening in the Steel Industry

Use the AI-powered search engine to analyze production activity, market trends, and news faster than ever before.

Try the Free AI Search EngineItaly’s Steel Market: Stabilizing Prices Amid Activity Fluctuations

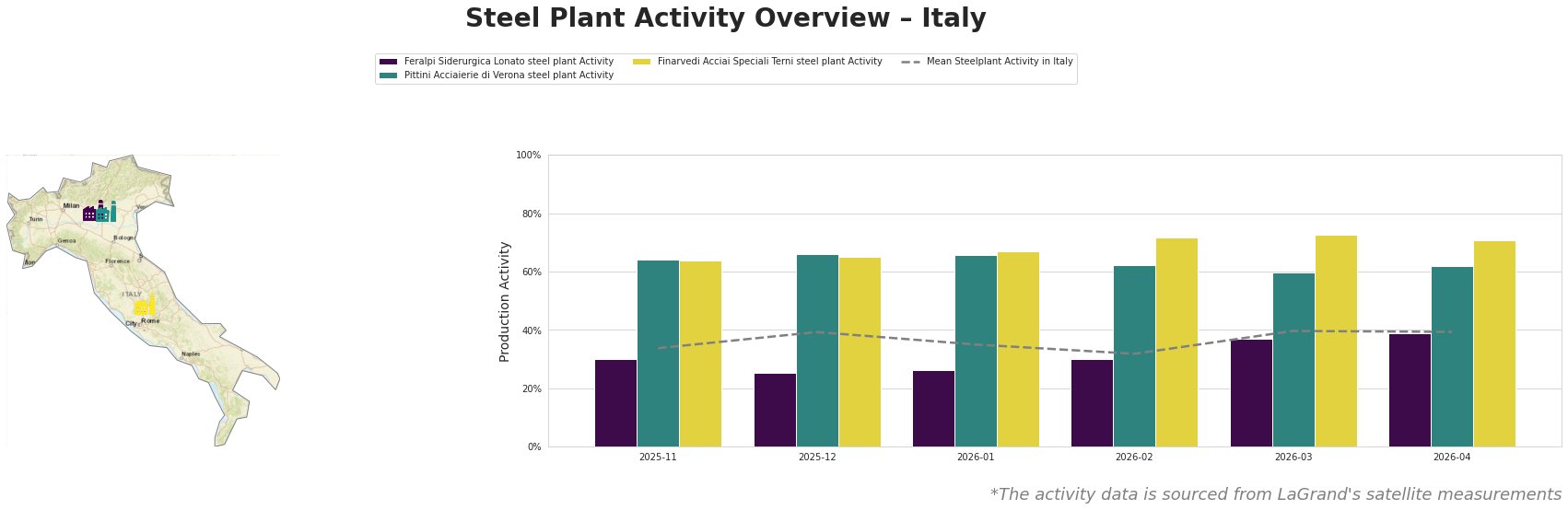

The Italian steel market faces mixed signals, as recent activity levels at key steel plants have stabilized while prices remain under pressure. The news articles “EU steel processors question sustainability of price hikes” and “EU HRC: Market sees dip as temporary” highlight the challenges stemming from rising coil prices and supply constraints. Satellite data indicates a slight recovery in activity, but significant concerns about demand persist.

Feralpi Siderurgica Lonato has experienced fluctuations, with activity dropping to 25% in December before recovering to 39% by April, aligning with concerns over price hikes highlighted in “EU steel processors question sustainability of price hikes.” Pittini Acciaierie di Verona showed stability with a peak activity of 66% before tapering, reflecting demand pressures discussed in the news. Finarvedi Acciai Speciali Terni exhibited consistent performance with 72% in February and 71% in April, providing essential products like hot-rolled and cold-rolled steels to sectors such as automotive and infrastructure, despite weak demand cited in multiple articles.

The market sentiment remains neutral, reflecting apprehensions about future price increases despite observed activity improvements. As noted in “EU HRC prices stay largely rangebound as participants await safeguard clarity,” mills have been unable to raise prices despite attempts, indicating a challenging environment for procurement. With domestic coil prices hovering around €700–720 per tonne, steel buyers are advised to monitor prices closely and consider securing inventories at current rates.

In conclusion, potential disruptions could arise from ongoing geopolitical tensions affecting imports, particularly as noted in “HRC EU: The market considers the fall as temporary.” Steel buyers should prioritize local suppliers to mitigate risks associated with potential regulatory changes affecting imported materials, especially when assessing their procurement strategies for Q2 2026. With limited import options and anticipated price volatility, focusing on established domestic relationships becomes imperative for ensuring supply continuity.